Download

1 / 10

100 likes | 418 Views

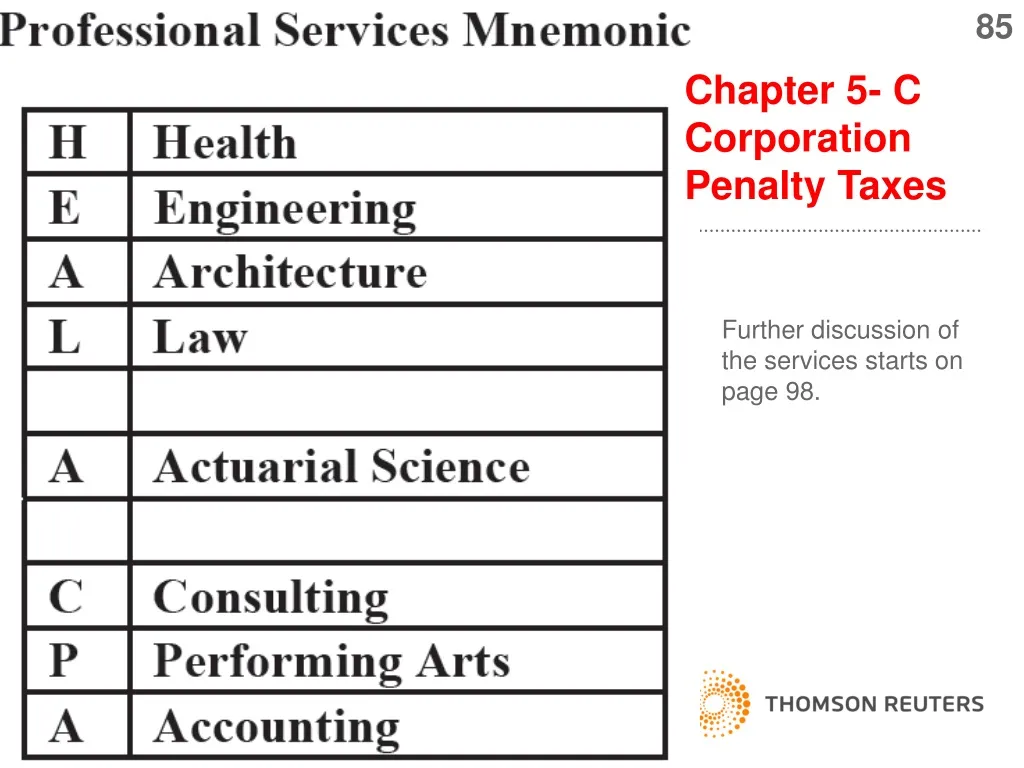

85. Chapter 5- C Corporation Penalty Taxes. Further discussion of the services starts on page 98. 86. Professional Service Corporations(PSC). A. Limitations. B. Meets all of the following:. C Corporation HEAL A CPA Activity More than 50% of Comp. attributed to PSC services.

E N D

85 Chapter 5- C Corporation Penalty Taxes Further discussion of the services starts on page 98.

86 Professional Service Corporations(PSC) A. Limitations B. Meets all of the following: C Corporation HEAL A CPA Activity More than 50% of Comp. attributed to PSC services. > 20% Comp for PSC services performed by owner employees. On last day of year, employee owners own more than 10% of stock. (IRC. 318) • Limited choice in year end. • 444 owner payment limitations. • PALs = No Offset against other income. • AET -$150,000

92 VI. Qualified Personal Service Corporations Issues • 35% Flat tax • Can use cash basis. Defined • Function test- 95% or more of employee time is HEAL A CPA • Ownership - 95% or more of stock at all times held by current or retired employees who perform services.

91 Beating the 35% Tax Rate • Have 6% of employee time doing something other than HEAL A CPA. • Get 6% stock out of the hands of current and former employees. • Bonuses can kick you in the face if not reasonable – See New Case page 91.

92 VII. QPSC Function Test Beating the Function Test- Employee time under 95%. • Get a Cat- DKD enterprises Inc, • Mix in other services- Ron Lykins Inc. • Challenge the definition- Kraatz & Craig Surveying Inc. (lost)

93 VIII. QPSC Ownership Test

94 Accumulated Earnings Test • 20 % tax on excess over • $250,000 Reg. C Corp • $150,000 PSC • Reasonable business needs

94 Accumulated Earnings Test

94 Bardahl -Cash Need for the Operating Cycle

94 Bardahl Created a formula to project the amount of working capital needed to fund business. It has to be modified for non-manufacturers In addition amounts that you can document enter in to the picture- Page 95- Item F.