Download

1 / 3

30 likes | 42 Views

With the rise in the Covid-19 pandemic, a dramatic impact has been observed on the global economy and financial markets. To keep running the financial system, several central banks around the globe have dropped the interest rates to nearly zero. The interest rate in the US is in the range of 0% to 0.25%, in the UK it is 0.1%, in India itu2019s 4% while Japan which already adopted a negative rate of 0.1% in 2016 yet remains unchanged. To support the economy and the industry, various governments have eased their fiscal policies and even initiated quick measures to provide the much-required financial support which amounts to about $9 trillion according to IMF as of April 2020. This article tries to highlight some of the key recent developments in the Indian debt market and tries to identify current and potential risks.<br>

E N D

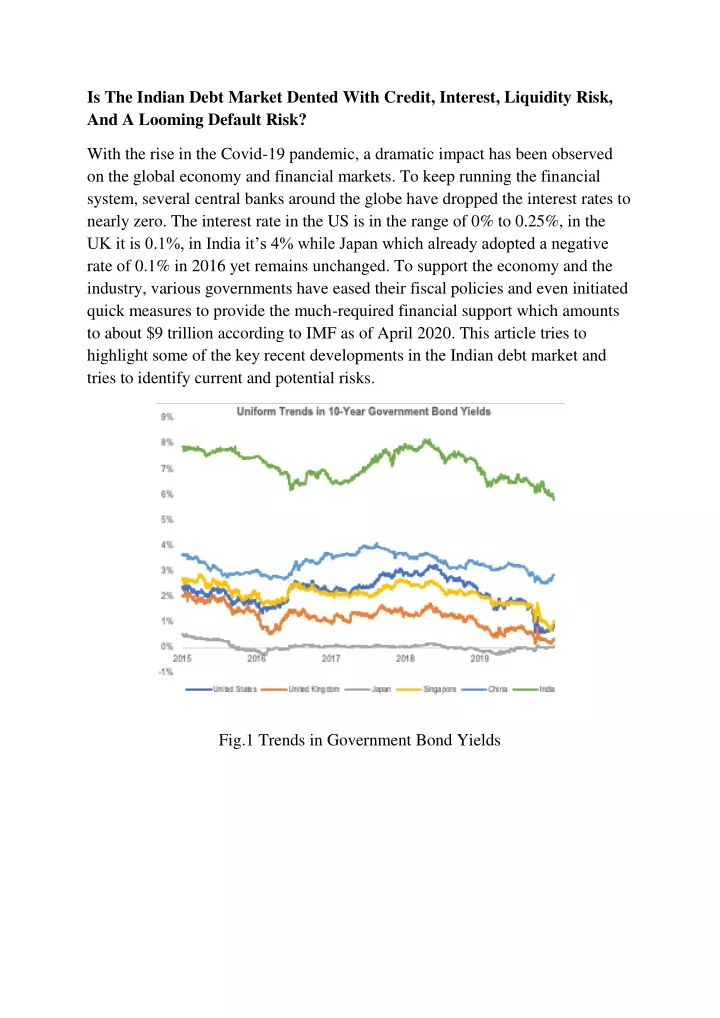

Is The Indian Debt Market Dented With Credit, Interest, Liquidity Risk, And A Looming Default Risk? With the rise in the Covid-19 pandemic, a dramatic impact has been observed on the global economy and financial markets. To keep running the financial system, several central banks around the globe have dropped the interest rates to nearly zero. The interest rate in the US is in the range of 0% to 0.25%, in the UK it is 0.1%, in India it’s 4% while Japan which already adopted a negative rate of 0.1% in 2016 yet remains unchanged. To support the economy and the industry, various governments have eased their fiscal policies and even initiated quick measures to provide the much-required financial support which amounts to about $9 trillion according to IMF as of April 2020. This article tries to highlight some of the key recent developments in the Indian debt market and tries to identify current and potential risks. Fig.1 Trends in Government Bond Yields

Fig.2 Trends in Indian Corporate Bond Market The benchmark Indian 10-year government bond dropped to around 6% in the first week of March and stands at 5.87% on 10 June 2020, lowest in the last five years. This drop was triggered due to the global sell-off in emerging markets and the concerns of widening fiscal deficit in India. The AAA-rated PSU as well as Private Sector Bonds observed a huge sell-off resulting in the yields to rise by about 100 to 150 basis points. The number of trades in corporate bonds have more than doubled in the span of the last ten years from INR 397 bn (3,165 trades) in April 2011 to INR 2,145 bn (8,926 trades) in April 2020. The debt market in India yet remains underdeveloped with government debt at ~68.62% of GDP. The government debt to GDP ratio for the US, UK, and Japan is 107%, 80.7%, and 238%, respectively. The value of sovereign securities held by global funds have dropped to INR 767 billion due to the steep hedging costs for foreign currency risk incurred which has led to a deterioration in returns. Recent Highlights Of The Indian Debt Market Liquidity in the debt market forces Franklin Templeton to freeze its six debt schemes, triggering the liquidity crisis in the debt market The three-pronged strategy (OMO, rate cuts, and economic relief package) is expected to pump the necessary liquidity in the financial market

Amendments to the Insolvency and Bankruptcy Code (IBC) offer a good window for genuine distressed assets, however, leaves the creditors with a long impending uncertainty Launch of the Request for Quote (RFQ) platform is expected to bring depth, liquidity as well as transparency in the bond markets Liquidity Risks In The Debt Market Forces Franklin Templeton To Freeze Six Of Its Debt Schemes Fear of poor liquidity flew through the corporate debt market when Franklin Templeton informed its investors of winding up its six debt schemes. According to a press release by Franklin Templeton, the combined assets under management (AUM) of these six debt fund schemes stood at about INR 25,648 crores as on 23 April 2020. These schemes represent less than 1.4% of the Indian Mutual Fund Industry AUM as on 31 March 2020. The decision to wind up was taken to protect the interest of investors through a managed sale of the portfolio and was limited to funds that had direct exposure to higher-yielding, lower-rated credit securities in India which had been most impacted by the ongoing liquidity crisis in the market. The extreme drop in liquidity in debt markets along with large redemptions due to the Covid-19 outbreak compelled the fund house to take such a drastic measure. This announcement led to a spike in yields on bonds rated AA and below. Vedanta Ltd, Uttar Pradesh Power Corporation’s Bond, and Shriram Finance Corporation were among the top holdings of these schemes. Franklin Templeton was the sole lender to about one-third of the bonds, the issue of credit and liquidity risk does not just pertain to this fund portfolio alone, however, it is a result of the market-wide fear and slowdown. More Details: valueadd-research.com/blog/is-the-indian-debt-market-dented- with-credit-interest-liquidity-risk-and-a-looming-default-risk/