Download

1 / 6

0 likes | 12 Views

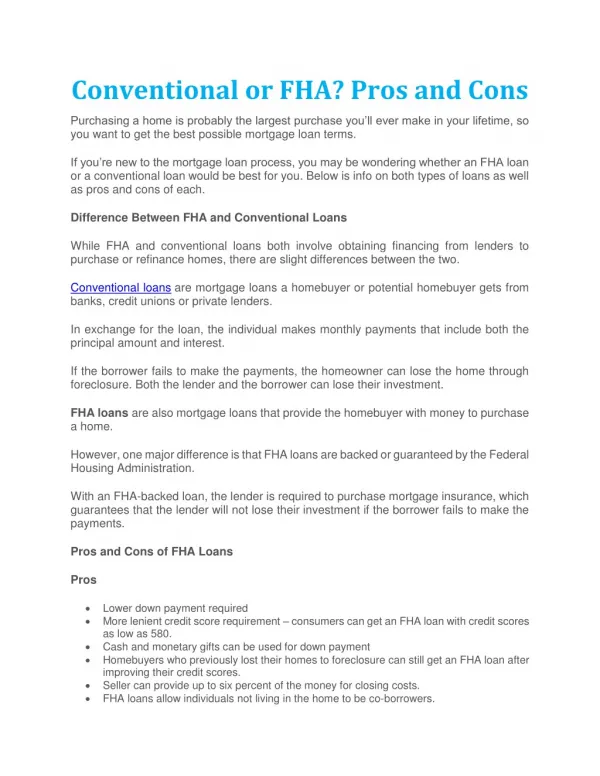

Regarding financing a home, various options are available to prospective buyers. Two popular choices often emerge in the discussion are FHA (Federal Housing Administration) and conventional loans. Understanding the differences between these two loan types is crucial for anyone purchasing a property.<br>

E N D

FHA vs. Conventional Loans: Understanding the Definition and Differences Introduction: An Overview of FHA and Conventional Loans Regarding financing a home, various options are available to prospective buyers. Two popular choices often emerge in the discussion are FHA (Federal Housing Administration) and conventional loans. Understanding the differences between these two loan types is crucial for anyone purchasing a property. This article will provide an overview of FHA and conventional loans, defining each type and highlighting their key distinctions. Whether you're a first-time homebuyer or someone considering refinancing options, gaining insights into these loan types will empower you to make informed decisions about your home financing journey.

So, let's delve into FHA and conventional loans, exploring their features, eligibility criteria, benefits, and considerations. By the end of this article, you'll have a comprehensive understanding of these loan options and be better equipped to choose the one that aligns with your specific needs and financial goals. Definition of FHA Loans Federal Housing Administration (FHA) loans are government-backed mortgages that offer a cost-effective choice to prospective homeowners. These loans aim to enable middle-class individuals and families to fulfill their dream of becoming homeowners. The low down payment requirement of FHA loans is their main advantage. FHA loans appeal to those with limited savings or equity because they can be qualified with as little as 3.5% down. Furthermore, regarding qualifying requirements, FHA loans are more accommodating than conventional mortgages. These loans are insured by the Federal Housing Administration, which lowers the risk for lenders and enables them to provide better terms to borrowers with lower credit scores or higher debt-to-income ratios. The Federal Housing Administration plays a vital role in guaranteeing these loans. Because the FHA protects lenders from potential losses, it encourages them to offer financing options that might otherwise be deemed too hazardous. Thanks to this government support, more people and families will have access to affordable housing options. In conclusion, FHA loans are government-insured mortgages with flexible qualifying standards and minimal down payment requirements. The Federal Housing Administration guarantees these loans and helps more borrowers achieve homeownership. Definition of Conventional Loans Conventional or traditional mortgage loans are non-government-backed loans widely used in the real estate industry. Unlike government-insured loans such as FHA or VA loans, conventional loans are not guaranteed or insured by any governmental entity. The defining characteristic of conventional loans is that the government needs to back them. This means lenders take on more risk when offering these types of loans. To mitigate this risk, lenders often require borrowers to pay at least 20% of the home's purchase price down. This helps establish property equity and reduces the lender's exposure. One key distinction between conventional and FHA loans is that conventional loans typically require a higher down payment. While FHA loans often have down payment requirements as low as 3.5%, traditional loan borrowers may be required to put down 5% or more. Another essential aspect to consider when discussing conventional loans is private mortgage insurance (PMI). PMI is typically required for borrowers who make a down payment of less than 20%. This insurance protects the lender in case the borrower defaults on the loan. Borrowers need to understand that PMI adds cost to their monthly mortgage payments. Eligibility criteria for conventional loan applicants can vary depending on the lender's requirements. Generally, lenders look at factors such as credit score, debt-to-income ratio, employment history, and financial stability when evaluating applicants for conventional loans.

In summary, conventional loans give borrowers flexibility and options in the mortgage lending market. Private lenders are crucial in providing these types of mortgages without government backing. Understanding private mortgage insurance and meeting eligibility criteria are essential aspects for those considering applying for a conventional loan. Main Differences between FHA and Conventional Loans: Pros and Cons Comparison When choosing between FHA and conventional loans, it's essential to understand the key differences and weigh the pros and cons of each option. FHA and conventional loans have their own advantages and disadvantages, making it crucial for borrowers to make an informed decision based on their specific needs and circumstances. FHA loans, backed by the Federal Housing Administration, are known for their more lenient qualification requirements. They typically allow for lower credit scores and require a smaller down payment than conventional loans. This makes them a popular choice for first-time homebuyers or those with limited financial resources. Additionally, FHA loans offer fixed interest rates, making budgeting more accessible for borrowers. On the other hand, conventional loans are not insured or guaranteed by any government agency. They often require higher credit scores and a larger down payment but can offer more flexibility regarding loan options and repayment terms. Conventional loans also don't require mortgage insurance once the borrower's equity reaches a certain threshold. One advantage of FHA loans is that they allow borrowers with lower credit scores or limited funds to become homeowners. However, one drawback is that FHA loans typically come with mortgage insurance premiums that can increase monthly payments over time. FHA Loans: ● Down Payment: Exploring borrowers' lower down payment requirements opens up new possibilities for aspiring homeowners. Traditionally, the down payment has been a significant hurdle for many individuals and families looking to purchase a property. However, with changing times and evolving lending practices, lenders are now offering more flexible options to accommodate a broader range of borrowers. ● Credit Score: When obtaining an FHA loan, understanding the credit score requirements is essential. The Federal Housing Administration (FHA) provides loans backed by the government, making them accessible to individuals with lower credit scores than traditional loans. Applicants must meet specific credit score requirements to be eligible for an FHA loan. Generally, a minimum credit score 580 is required to qualify for a 3.5% down payment option. However, borrowers with credit scores between 500 and 579 may still be eligible for an FHA loan with a higher % down payment requirement of 10%.

It's important to note that while the FHA has set these minimum requirements, individual lenders may have their criteria and consider additional factors such as income and employment history. ● Interest Rates: Analyzing the interest rates associated with FHA loans is crucial for potential homebuyers and real estate investors. The Federal Housing Administration (FHA) offers loans backed by the government, providing borrowers with more accessible financing options. When considering FHA loans, understanding the interest rates is essential as it directly impacts the overall cost of borrowing. These rates can vary depending on credit score, loan amount, and market conditions. ● Mortgage Insurance: Mortgage insurance protects lenders if borrowers default on their loans. Lenders can provide financing options with lower down payments and more flexible credit requirements. With FHA loans, borrowers are required to pay an upfront premium at closing and an annual premium divided into monthly payments. The upfront premium is typically 1.75% of the loan amount and can be financed into the loan itself. This means borrowers don't have to pay it out-of-pocket at closing but should be aware that it increases the loan amount and subsequent interest charges. Conventional Loans: ● Down Payment: Conventional mortgages are one of the most common types of home loans, and they often have specific down payment requirements. While these requirements can vary depending on factors such as credit score and loan amount, there are some general guidelines to remember. Conventional US Mortgage Loan Processing Support Services USA typically requires a down payment ranging from 5% to 20% of the purchase price. For example, if you purchase a $300,000 home, your down payment could range from $15,000 to $60,000. The percentage required will depend on factors such as your creditworthiness and financial situation. It's important to note that putting more money towards your down payment can have its benefits. A larger down payment can result in lower monthly mortgage payments and help you secure a better interest rate on your loan. ● .Credit Score: Conventional loans typically have higher credit score requirements compared to other types of loans. This is because the government does not insure or guarantee them, meaning lenders bear more risk. The credit score requirement may vary depending on the lender and other factors such as down payment amount and debt-to-income ratio. By comparing different lenders' credit score requirements, borrowers can identify potential options that align with their current financial situation. It's important to note that while a higher credit score generally improves one's chances of getting approved for a conventional loan, other factors, such as income stability and employment history, also play a role in the decision-making process. ● Interest Rates:

The interest rate on a conventional mortgage refers to the percentage of the loan amount that borrowers will pay annually as interest. This rate can vary depending on various factors, including market conditions, borrower's creditworthiness, loan term, and down payment amount. Understanding and comparing the interest rates different lenders offer is vital in making informed decisions about financing options. By examining these rates, borrowers can assess their affordability and choose a mortgage that aligns with their financial goals. ● Mortgage Insurance: Private mortgage insurance (PMI) plays a crucial role in conventional loans. Understanding its implications and how it affects borrowers and lenders alike is essential. Private mortgage insurance is typically required for conventional loans with a down payment of less than 20%. It acts as a safeguard for lenders in case the borrower defaults on their loan payments. While PMI protects the lender, it does come with specific implications for the borrower. One of the main implications of PMI is that it adds cost to the monthly mortgage payment. This can impact a borrower's budget and affordability. However, it is worth noting that PMI can be removed once the borrower reaches a certain level of equity in their home. Another implication is that PMI may limit borrowing options for some borrowers. Lenders often have specific requirements for private mortgage insurance, which could affect loan approval or interest rates. Finding the Right Loan Option: Factors to Consider When it comes to finding the right loan option, there are several factors that you need to consider. Two standard loan options that borrowers often compare are FHA and conventional loans. Understanding the eligibility requirements for each can help you make an informed decision based on your financial situation. One of the first steps in evaluating your financial situation is to assess your credit history. Lenders will review your credit score and payment history to determine your eligibility for a loan. This information will also impact the interest rates and terms you may qualify for. Another crucial factor to consider is the impact of down payment requirements on your budget. FHA loans typically have lower down payment requirements compared to conventional loans, which may be beneficial if you have limited funds available upfront. However, thinking about your long-term homeownership goals and potential resale plan is essential. Conventional loans may offer more flexibility regarding refinancing or selling the property in the future, while FHA loans have specific guidelines that can affect future transactions. By carefully evaluating these factors - eligibility requirements, financial situation, long-term goals, and potential resale plans - you can decide which loan option is best suited for your needs. Conclusion: Making an Informed Decision between FHA and Conventional Loans FHA US Mortgage Loan Processing Services USA may be a viable choice for those with lower credit scores or limited funds for a down payment. The lower credit score requirements and lower down

payment options offered by the Federal Housing Administration can make homeownership more accessible for individuals who may not qualify for conventional loans. On the other hand, if you have a higher credit score and can afford a larger down payment, a conventional loan might be the better option. Conventional loans offer more flexibility in loan terms and interest rates, allowing borrowers to save money over the long term. When deciding between FHA and conventional loans, it is essential to carefully evaluate your financial situation and consider factors such as future plans, income stability, and overall affordability. Consulting with a mortgage professional can provide valuable guidance in navigating this decision-making process. Ultimately, selecting the right loan option will depend on your unique circumstances. By weighing the pros and cons of each type of loan and considering your personal financial goals, you can confidently choose the financing solution that best suits your needs.