Download

1 / 3

60 likes | 290 Views

Break-Even Analysis. Company "A" Plans to Sale Units for $100 Variable Cost : Employee Wages $8 per Hour (4 hours per unit) Supplies $1 per Unit Other Variable C ost $2 per Unit Total - $35 Fixed Cost : Depreciation $3,000 Factory Lease $7,000 Advertising Cost $6,000

E N D

Break-Even Analysis Company "A" Plans to Sale Units for $100 Variable Cost: Employee Wages $8 per Hour (4 hours per unit) Supplies $1 per Unit Other Variable Cost $2 per Unit Total - $35 Fixed Cost: Depreciation $3,000 Factory Lease $7,000 Advertising Cost $6,000 Other Fixed Cost $4,100 Total - $20,100 • Employee wages $32 (5 hours* $8/hour), supplies $1, Other variable $2

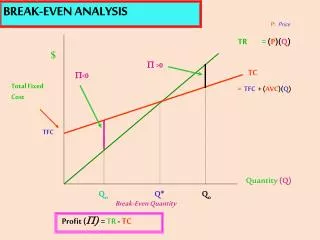

Break-Even in Sales • Units Price – Variable Cost = Contribution per Unit • $100 - $35*= $67 Contribution per Unit Sold • Fixed Cost / Contribution per Unit Sold = Break-even in Units Sold • $20,100 / $67 = 300 Units to Break-even

To Earn a Profit of $21,000 • (Fixed Cost + Target Profit) / Contribution = Units Sells Required to Reach Target Profit • ($20,100 + $21,000) / $67 = 600 Units Sold to Earn $21,000 Profit