Download

1 / 6

80 likes | 217 Views

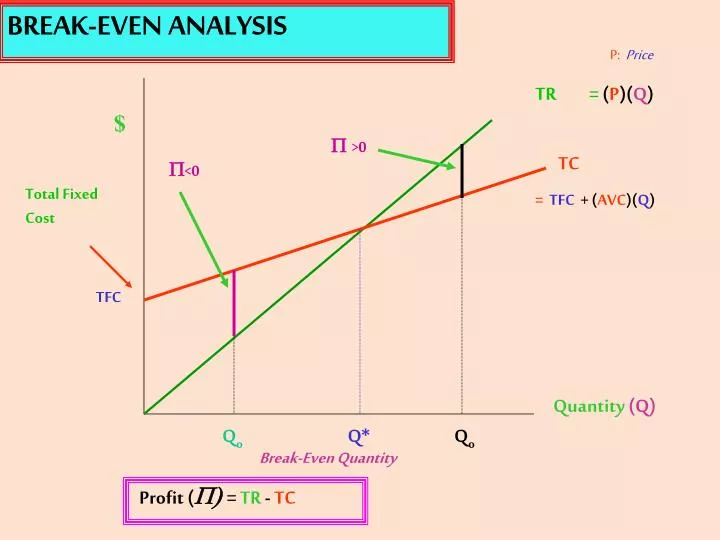

BREAK-EVEN ANALYSIS. BREAK-EVEN ANALYSIS. P: Price. TR. = ( P )( Q ). $. P >0. TC. P <0. Total Fixed Cost. = TFC + ( AVC )( Q ). TFC. Quantity (Q). Q o. Q*. Q o. Break-Even Quantity. Profit ( P) = TR - TC. P: Price TFC: Total Fixed Cost. Example:. TFC. TFC = $10.000.

E N D

BREAK-EVEN ANALYSIS BREAK-EVEN ANALYSIS P:Price TR = (P)(Q) $ P >0 TC P<0 Total Fixed Cost =TFC + (AVC)(Q) TFC Quantity (Q) Qo Q* Qo Break-Even Quantity Profit (P)= TR - TC

P:Price TFC:Total Fixed Cost Example: TFC TFC = $10.000 P = $20 Q* = AVC = $15/unit (P - AVC) 10.000 Q* = = 2.000 units (20 - 15) BREAK-EVEN ANALYSIS Profit (P)= TR - TC Critical Quantity: P = 0 TR = TC PQ* = TFC + (AVC)Q* PQ* - (AVC)Q* = TF (P - AVC)Q* = TFC P - AVC: gross margin

SPC 2,000 S* = = $8.000/wk S* = [(P-AVC)/P] [(20 - 15)/20] PROFIT-CONTRIBUTION & BREAK-EVEN Profit Volume = PV= (P)Q - (AVC)Q = (P – AVC)Q Sales = S = (P)Q Q = S/P PV = [(P – AVC)]S P Profit Contribution = Profit Volume – Specific ProgramCosts Pc = PV– SPC • Suppose P = $20/kg AVC = $15/kg SPC = $2,000 • Then: • PC = [(P-AVC)/P] S – SPC • = [(20 – 15)/20]S – 2,000 • = [.25]S – 2,000

PROFIT-CONTRIBUTION & BREAK-EVEN =[.25]14,000 – 2,000 = $1,500 PC 1,500 S* Profit Contribution ($) 0 14,000 8,000 Sales Volume/week ($) -2,000 PC = [.25]S – 2,000 S* = [2.000]/.25 = $8,000

PROFIT-CONTRIBUTION & BREAK-EVEN =[.33]14,000 – 2,000 = $2,620 PC’ 2,620 PC 1,500 S*’ S* Profit Contribution ($) 0 8,000 14.000 14,000 Sales Volume/week ($) -2,000 PC = [.33]S – 2,000 S*’ = [2,000]/.33 = $6,061