Download

1 / 19

190 likes | 339 Views

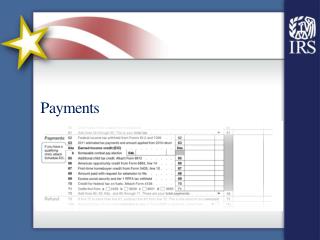

Payments. Pub 4491 – Page 275 Form 1040 – Lines 62-72. Intake/Interview. Also ask if taxpayer filed application for automatic extension of time to file this year’s tax return. Types of Payments. 1040 page 2. Federal income tax withheld Estimated payments Amounts applied from prior year

E N D

Payments Pub 4491 – Page 275Form 1040 – Lines 62-72 NTTC Training – 2013

Intake/Interview • Also ask if taxpayer filed application for automatic extension of time to file this year’s tax return NTTC Training – 2013

Types of Payments 1040 page 2 • Federal income tax withheld • Estimated payments • Amounts applied from prior year • Earned income credit • Additional child tax credit (Form 8812) • American opportunity credit (Form 8863) • Payments made with request for extension • Excess social security or tier 1 RRTA tax withheld NTTC Training – 2013

Form 1040, Page 2 NTTC Training – 2013

Withholding Sources • Employment • Social Security • Pensions, IRA distributions • Capital gains, interest, dividends • Unemployment compensation • Gambling winnings • W-2 • SSA 1099, RRB 1099 • 1099-R, RRB 1099-R • Broker Statement • 1099-INT, 1099-DIV • 1099-G • W-2G NTTC Training – 2013

Estimated Payments • Typically made if: • Self-employed • Investment income • Projected balance due >$1,000 (to avoid penalty) • Payments made periodically by taxpayer • No form – ask taxpayer if payments made • “When” and “How Much” for each • Check last year’s Form 1040-ES NTTC Training – 2013

Overpayment – Previous Year • Ask taxpayer if overpayment applied from last year to this year’s taxes • Review 2012 tax returns • TaxWise will bring forward via carryforward if applicable NTTC Training – 2013

Reporting • In TaxWise, link to F/S Tax Pd Worksheet from 1040, line 63 • Enter refunds applied from prior year (if any) • Enter Estimated Payments • Federal • State, if applicable(but not Local) NTTC Training – 2013

Estimated/Prior Year Tax Payments Ignore – automatically calculated by TaxWise if penalty due NTTC Training – 2013

TaxWise will carry payment to Sch A itemized deductions if marked as paid in 2013 TaxWise populates states based on Main Info sheet state return entries

Bottom of F/S Tax Pd Worksheet TaxWise populates states based on Main Info sheet state return entries NTTC Training – 2013

Amount Paid with Extension • If taxpayer filed Form 4868 for filing extension, enter amounts paid by: • Check • Electronic Fund Withdrawal • Credit card • Do not include any fees charged NTTC Training – 2013

Refundable Credits Automatically entered by TaxWise • Additional Child Tax Credit • Earned Income Credit • American Opportunity Credit • Excess Social Security paid NTTC Training – 2013

Refundable Credits Quiz #1 Which of the following are automatically calculated in TaxWise: • Federal Income Tax Withholding • Estimated taxes • Earned Income Credit • Additional Child Tax Credit • Refundable American Opportunity Credit NTTC Training – 2013

Refundable Credits #1 Answer • Federal Income Tax Withholding • Earned Income Credit • Additional Child Tax Credit • Refundable American Opportunity Credit Estimated taxes are not automatically calculated by TaxWise; must be input by counselor NTTC Training – 2013

Quality Review – Payments • Are estimated payments for 2013 included? • Are credits from the prior year entered? • State, too, if applicable • Confirm all taxes that were withheld are reflected as payments NTTC Training – 2013

Summary with Taxpayer • Review estimated tax and other payments NTTC Training – 2013

Payments Questions? Comments… NTTC Training – 2013

More Practice • Open Kent return and add Estimated Tax Payments from Pub 4491W, page 69 NTTC Training – 2013