Download

1 / 5

50 likes | 1.01k Views

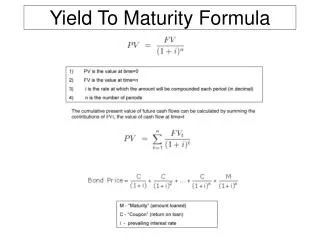

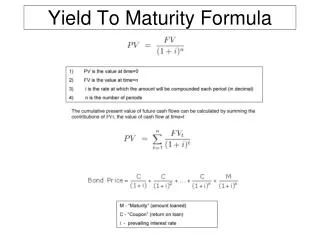

The Approximation Formula. F = Face Value = Par Value = $1,000P = Bond PriceC = the semi annual coupon interestN = number of semi-annual periods left to maturity. Example. Find the yield-to-maturity of a 5 year 6% coupon bond that is currently priced at $850. (Always assume the coupon interest is paid semi-annually.)Therefore there is coupon interest of $30 paid semi-annuallyThere are 10 semi-annual periods left until maturity .

E N D

1. Yield to Maturity The Approximation Approach Business 2039

3. Example Find the yield-to-maturity of a 5 year 6% coupon bond that is currently priced at $850. (Always assume the coupon interest is paid semi-annually.)

Therefore there is coupon interest of $30 paid semi-annually

There are 10 semi-annual periods left until maturity

4. Example � with solution Find the yield-to-maturity of a 5 year 6% coupon bond that is currently priced at $850. (Always assume the coupon interest is paid semi-annually.)

5. The logic of the equation The numerator simply represents the average semi-annual returns on the investment�it is made up of two components:

The first component is the average capital gain (if it is a discount bond) or capital loss (if it is a premium priced bond) per semi-annual period.

The second component is the semi-annual coupon interest received.

The denominator represents the average price of the bond.

Therefore the formula is basically, average semi-annual return on average investment.

Of course, we annualize the semi-annual return so that we can compare this return to other returns on other investments for comparison purposes.