Download

1 / 11

110 likes | 521 Views

Yield to maturity and holding period return. Marc Prud’Homme University of Ottawa. About this brief presentation. This presentation is based on the PDF file available on the website at http://www.veblen.ca/2012/MB_Fall2012/Readings/ ytmvshpr.pdf

E N D

Yield to maturity and holding period return Marc Prud’Homme University of Ottawa

About this brief presentation • This presentation is based on the PDF file available on the website at • http://www.veblen.ca/2012/MB_Fall2012/Readings/ytmvshpr.pdf • It deals with the “Yield to Maturity versus Holding Period Returns” • I picked it up on the Internet a while ago. I cannot take credit for it. I cannot also credit anyone with it since there is no name attached. • This topic is also covered in the book in Chapter 6 on pages 110 to 113.

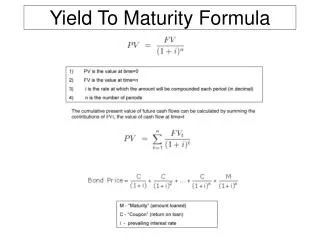

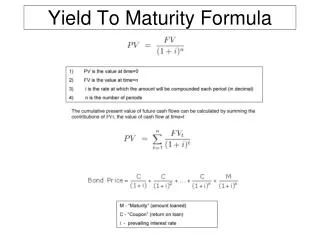

Yield to maturity • The Yield to maturity (YTM) of a bond or other fixed-interest security, is the internal rate of return (IRR, overall interest rate) earned by an investor who buys the bond today at the market price, assuming that the bond will be held until maturity, and that all coupon and principal payments will be made on schedule. • Contrary to popular belief, including concepts often cited in advanced financial literature, Yield to maturity does NOT depend upon a reinvestment of dividends. • Yield to maturity, rather, is simply the discount rate at which the sum of all future cash flows from the bond (coupons and principal) are equal to the price of the bond.

Example • A 30-year bond paying an annual coupon of $80 and selling at face value of $1,000. • What is the bonds YTM? • Recall equation 9 on page 72 in chapter 4. • Solve for i. This is your IRR and the YTM.

Example • Let go to Excel… • When the YTM is unchanged from its initial value, the rate of return on the bond will equal that yield. • Coupon rate = YTM • This is because the current price equals the face value.

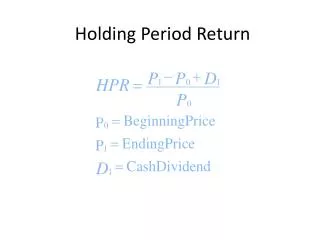

Holding period return (HPR) • The holding period return (HPR) is the total return on an asset (e.g., bond) over the period during which it was held. • It is one of the simplest measures of investment performance. • HPR is the percentage by which the value of an asset has grown for a particular period. • It is the sum of income and capital gains divided by the initial period value (asset value at the beginning of the period).

Example • A 30-year bond paying an annual coupon of $80 and selling at face value of $1,000. • What is the bonds HPR? • The HPR in this case is the same as the YTM.

Example • Now suppose that the bonds yield (or market interest rates) fall and the price of the bond increases to $1050. • What is the bonds HPR? • The HPR in this case is different than the YTM.

Example • Now suppose that the bonds yield (or market interest rates) increases and the price of the bond falls to $900. • What is the bonds HPR? • The HPR is negative and different from the YTM.

Explaining the difference between YTM and HPR • The YTM depends only 3 things: the current price, the bond’s coupon payment, and its face value. All of these values are observable today. • The HPR is a rate of return over a particular investment period, and depends on the market price of the bond at the end of the holding period. Of course, looking forward, this price is not known today. • Thus, the YTM today can be interpreted as the expected (or average) rate of return if the bond is held until maturity. Since bond prices over the holding period will respond to unanticipated changes in interest rates, holding period returns can be at most forecasted.