Download

1 / 0

0 likes | 176 Views

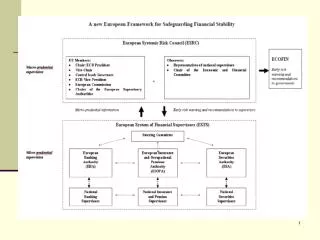

Developing Macro-stress tests: how to identify systemic risk. Session 10 Mindaugas Leika. Macroprudential policy framework. I. Macroprudential policy definition, targets, policy transmission channels and relationships with other policies (Monday) II. Institutional structure (Tuesday)

E N D