Download

1 / 1

20 likes | 236 Views

Analysis of the Pharmaceutical Supply Chain in Jordan Simon Conesa 1 , Prashant Yadav 1 , Rania Bader 2 (2009) 1 MIT-Zaragoza International Logistics Program, Zaragoza Logistics Center, SPAIN , 2 Consultant, MeTA Jordan Poster prepared by Samia Saad, MeTA Jordan Int. Consultant

E N D

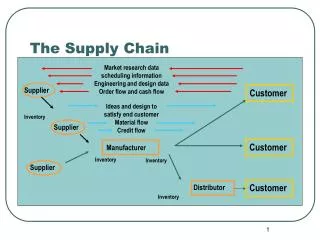

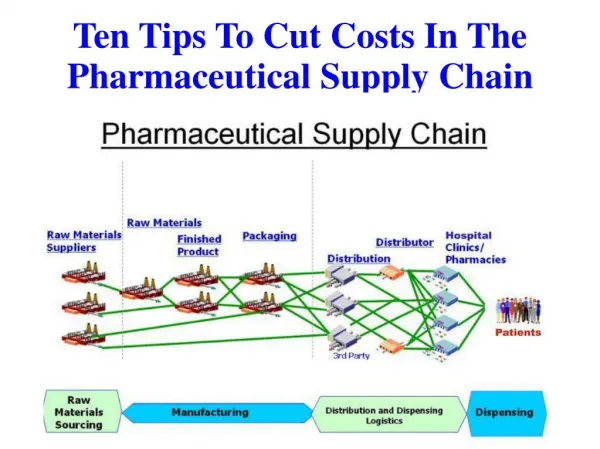

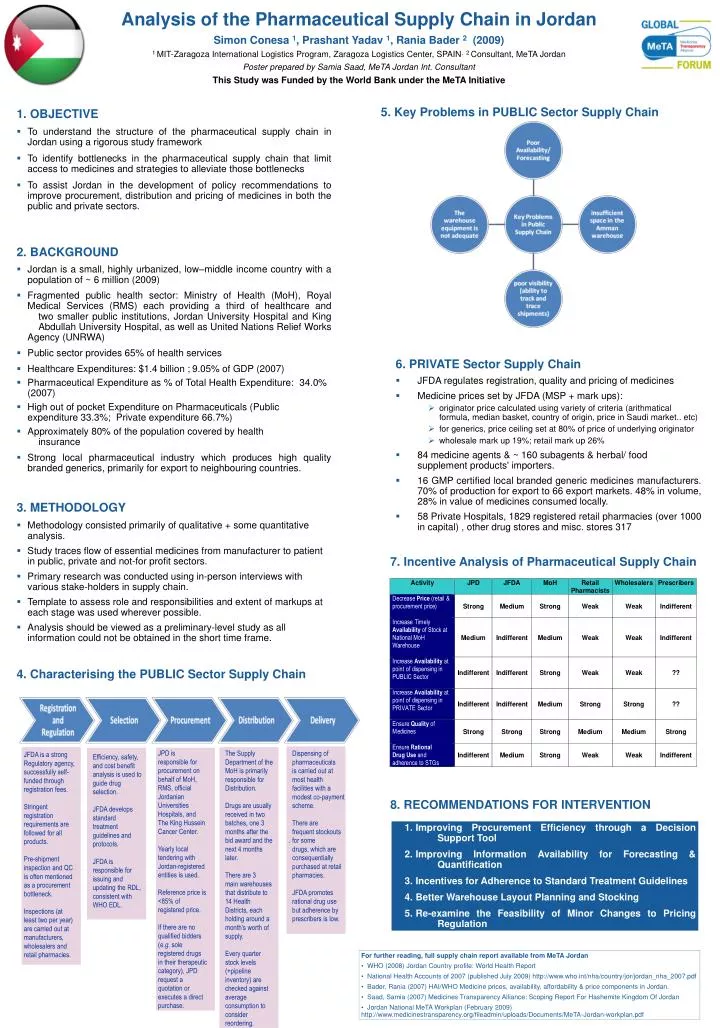

Analysis of the Pharmaceutical Supply Chain in Jordan Simon Conesa 1, Prashant Yadav 1, Rania Bader 2 (2009) 1 MIT-Zaragoza International Logistics Program, Zaragoza Logistics Center, SPAIN, 2 Consultant, MeTA Jordan Poster prepared by Samia Saad, MeTA Jordan Int. Consultant This Study was Funded by the World Bank under the MeTA Initiative 5. Key Problems in PUBLIC Sector Supply Chain 1. OBJECTIVE • To understand the structure of the pharmaceutical supply chain in Jordan using a rigorous study framework • To identify bottlenecks in the pharmaceutical supply chain that limit access to medicines and strategies to alleviate those bottlenecks • To assist Jordan in the development of policy recommendations to improve procurement, distribution and pricing of medicines in both the public and private sectors. 2. BACKGROUND • Jordan is a small, highly urbanized, low–middle income country with a population of ~ 6 million (2009) • Fragmented public health sector: Ministry of Health (MoH), Royal Medical Services (RMS) each providing a third of healthcare and two smaller public institutions, Jordan University Hospital and King Abdullah University Hospital, as well as United Nations Relief Works Agency (UNRWA) • Public sector provides 65% of health services • Healthcare Expenditures: $1.4 billion ;9.05% of GDP (2007) • Pharmaceutical Expenditure as % of Total Health Expenditure: 34.0% (2007) • High out of pocket Expenditure on Pharmaceuticals (Public expenditure 33.3%; Private expenditure 66.7%) • Approximately 80% of the population covered by health insurance • Strong local pharmaceutical industry which produces high quality branded generics, primarily for export to neighbouring countries. 3. METHODOLOGY • Methodology consisted primarily of qualitative + some quantitative analysis. • Study traces flow of essential medicines from manufacturer to patient in public, private and not-for profit sectors. • Primary research was conducted using in-person interviews with various stake-holders in supply chain. • Template to assess role and responsibilities and extent of markups at each stage was used wherever possible. • Analysis should be viewed as a preliminary-level study as all information could not be obtained in the short time frame. 4. Characterising the PUBLIC Sector Supply Chain • 6. PRIVATE Sector Supply Chain • JFDA regulates registration, quality and pricing of medicines • Medicine prices set by JFDA (MSP + mark ups): • originator price calculated using variety of criteria (arithmatical formula, median basket, country of origin, price in Saudi market.. etc) • for generics, price ceiling set at 80% of price of underlying originator • wholesale mark up 19%; retail mark up 26% • 84 medicine agents & ~ 160 subagents & herbal/ food supplement products' importers. • 16 GMP certified local branded generic medicines manufacturers. 70% of production for export to66 export markets. 48% in volume, 28% in value of medicines consumed locally. • 58 Private Hospitals, 1829 registered retail pharmacies (over 1000 in capital) , other drug stores and misc. stores 317 7. Incentive Analysis of Pharmaceutical Supply Chain . JPD is responsible for procurement on behalf of MoH, RMS, official Jordanian Universities Hospitals, and The King Hussein Cancer Center. Yearly local tendering with Jordan-registered entities is used. Reference price is <85% of registered price. If there are no qualified bidders (e.g. sole registered drugs in their therapeutic category), JPD request a quotation or executes a direct purchase. The Supply Department of the MoH is primarily responsible for Distribution. Drugs are usually received in two batches, one 3 months after the bid award and the next 4 months later. There are 3 main warehouses that distribute to 14 Health Districts, each holding around a month’s worth of supply. Every quarter stock levels (+pipeline inventory) are checked against average consumption to consider reordering. Dispensing of pharmaceuticals is carried out at most health facilities with a modest co-payment scheme. There are frequent stockouts for some drugs, which are consequentially purchased at retail pharmacies. JFDA promotes rational drug use but adherence by prescribers is low. JFDA is a strong Regulatory agency, successfully self-funded through registration fees. Stringent registration requirements are followed for all products. Pre-shipment inspection and QC is often mentioned as a procurement bottleneck. Inspections (at least two per year) are carried out at manufacturers, wholesalers and retail pharmacies. Efficiency, safety, and cost benefit analysis is used to guide drug selection. JFDA develops standard treatment guidelines and protocols. JFDA is responsible for issuing and updating the RDL, consistent with WHO EDL. 8. RECOMMENDATIONS FOR INTERVENTION • Improving Procurement Efficiency through a Decision Support Tool • Improving Information Availability for Forecasting & Quantification • Incentives for Adherence to Standard Treatment Guidelines • Better Warehouse Layout Planning and Stocking • Re-examine the Feasibility of Minor Changes to Pricing Regulation • For further reading, full supply chain report available from MeTA Jordan • WHO (2008) Jordan Country profile: World Health Report • National Health Accounts of 2007 (published July 2009) http://www.who.int/nha/country/jor/jordan_nha_2007.pdf • Bader, Rania (2007) HAI/WHO Medicine prices, availability, affordability & price components in Jordan. • Saad, Samia (2007) Medicines Transparency Alliance: Scoping Report For Hashemite Kingdom Of Jordan • Jordan National MeTA Workplan (February 2009) http://www.medicinestransparency.org/fileadmin/uploads/Documents/MeTA-Jordan-workplan.pdf