Download

1 / 39

390 likes | 744 Views

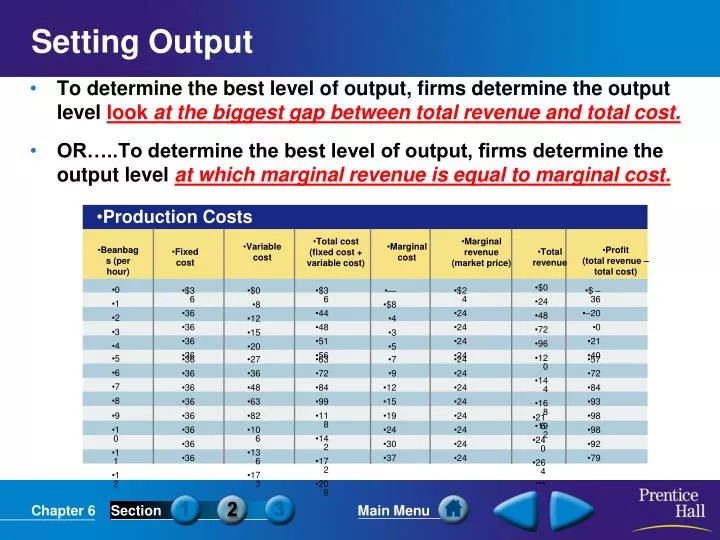

Production Costs. Total cost (fixed cost + variable cost). Marginal revenue (market price). Variable cost. Marginal cost. Beanbags (per hour). Profit (total revenue – total cost). Fixed cost. Total revenue. $0 24 48 72 96. 0 1 2 3 4. $36 36 36 36 36. $0 8 12 15 20.

E N D

Production Costs • Total cost (fixed cost + variable cost) • Marginal revenue (market price) • Variable cost • Marginal cost • Beanbags (per hour) • Profit(total revenue – total cost) • Fixed cost • Total revenue • $0 • 24 • 48 • 72 • 96 • 0 • 1 • 2 • 3 • 4 • $36 • 36 • 36 • 36 • 36 • $0 • 8 • 12 • 15 • 20 • $36 • 44 • 48 • 51 • 56 • — • $8 • 4 • 3 • 5 • $24 • 24 • 24 • 24 • 24 • $ –36 • –20 • 0 • 21 • 40 • 120 • 144 • 168 • 192 • 5 • 6 • 7 • 8 • 36 • 36 • 36 • 36 • 27 • 36 • 48 • 63 • 63 • 72 • 84 • 99 • 7 • 9 • 12 • 15 • 24 • 24 • 24 • 24 • 57 • 72 • 84 • 93 • 9 • 10 • 11 • 12 • 36 • 36 • 36 • 36 • 82 • 106 • 136 • 173 • 118 • 142 • 172 • 209 • 19 • 24 • 30 • 37 • 24 • 24 • 24 • 24 • 98 • 98 • 92 • 79 • 216 • 240 • 264 • 288 Setting Output • To determine the best level of output, firms determine the output level look at the biggest gap between total revenue and total cost. • OR…..To determine the best level of output, firms determine the output level at which marginal revenue is equal to marginal cost.

Combining Supply and Demand • How do supply and demand create balance in the marketplace? • What are differences between a market in equilibrium and a market in disequilibrium? • What are the effects of price ceilings and price floors?

Combining Supply and Demand • In the ‘Case of the Pizzerias in the book’, Ch6, section 1: • 1. The market equilibrium price is ($): • 2. The market supply level (qty): • 3. The market demand level(qty): • In Any Market Environment • 4. How equilibrium is shown on a supply and demand graph: • 5. Two possible outcomes of disequilibrium: • 6. Supplier price response to excess demand: • 7. Condition under which market forces will push market toward the equilibrium: • In the Case of Government Intervention • 8. Purpose(s) of rent control: • 9. Negative results of ending rent control: • 10. Effect on labor when minimum wage exceeds equilibrium:

The point at which quantity demanded and quantity supplied come together is known as equilibrium. Finding Equilibrium Equilibrium Point Combined Supply and Demand Schedule $3.50 $3.00 $2.50 $2.00 $1.50 $1.00 $.50 Price of a slice of pizza Quantity demanded Quantity supplied Result $ .50 300 100 Shortage from excess demand Price per slice a Equilibrium Price $1.00 250 150 $1.50 200 200 Equilibrium Equilibrium Quantity $2.00 150 250 Supply Demand Surplus from excess supply $2.50 100 300 0 50 100 150 200 250 300 350 350 $3.00 50 Slices of pizza per day Balancing the Market

Excess Demand: Excess demand occurs when quantity demanded is more than quantity supplied. Market Disequilibrium If the market price or quantity supplied is anywhere but at the equilibrium price, the market is in a state called disequilibrium. There are two causes for disequilibrium:

Excess Supply Excess supply occurs when quantity supplied exceeds quantity demanded. Market Disequilibrium If the market price or quantity supplied is anywhere but at the equilibrium price, the market is in a state called disequilibrium. There are two causes for disequilibrium: Interactions between buyers and sellers will always push the market back towards equilibrium.

Price Ceilings • A price ceiling is a maximum price that can be legally charged for a good. • An example of a price ceiling is rent control, a situation where a government sets a maximum amount that can be charged for rent in an area. In some cases the government steps in to control prices. These interventions appear as price ceilings and price floors.

Remember: A price ceiling is a maximum price that can be legally charged for a good. Price Ceiling (continued)

One well-known price floor is the minimum wage, which sets a minimum price that an employer can pay a worker for an hour of labor. Price Floors A price floor is a minimum price, set by the government, that must be paid for a good or service.

Combining Supply and Demand Problem Hy Feshn owns and operates a necktie boutique in one of New York City’s trendy neighborhoods. The spring weather is mild, his clientele is loyal, and overall, his business prospers. A friend in the garment district tells him, however, that the coming fall’s new fad will be the starched turtleneck shirt worn without a tie. Hy knows that fads fade quickly, but he still worries about keeping his business going during the down season sure to come. Hy Feshn Neckties Hy’s first line of defense is to cut expenses. He calls Cap Hill, his congressional representative, to see if he is eligible for any government help. Cap says no, but his mother would let him have her nearby rent-controlled apartment for a fee of $500 in addition to the usual rent. Hy decides to pay the $500 and convert the cheaper second-story quarters into a boutique. Hy takes inventory before he moves and finds he has no more $30 Speckle ties but nearly his full shipment of $50 Spott ties in stock. He plans to make some adjustments after he moves. 1. In what way does Hy benefit from government price ceilings? 2. How does Hy’s experience illustrate some of the problems connected with government price intervention? 3. What part of Hy’s inventory illustrates excess supply?

Section 1 Assessment 1. Equilibrium in a market means which of the following? (a) the point at which quantity supplied and quantity demanded are the same (b) the point at which unsold goods begin to pile up (c) the point at which suppliers begin to reduce prices (d) the point at which prices fall below the cost of production 2. The government’s price floor on low wages is called the (a) market equilibrium (b) base wage rate (c) minimum wage (d) employment guarantee Want to connect to the PHSchool.com link for this section? Click Here!

Section 1 Assessment 1. Equilibrium in a market means which of the following? (a) the point at which quantity supplied and quantity demanded are the same (b) the point at which unsold goods begin to pile up (c) the point at which suppliers begin to reduce prices (d) the point at which prices fall below the cost of production 2. The government’s price floor on low wages is called the (a) market equilibrium (b) base wage rate (c) minimum wage (d) employment guarantee Want to connect to the PHSchool.com link for this section? Click Here!

Combining Supply and Demand • How do supply and demand create balance in the marketplace? • What are differences between a market in equilibrium and a market in disequilibrium? • What are the effects of price ceilings and price floors?

Changes in Market Equilibrium • How do shifts in supply affect market equilibrium? • How do shifts in demand affect market equilibrium? • How can we use supply and demand curves to analyze changes in market equilibrium?

Shifts in Supply • Understanding a Shift • Since markets tend toward equilibrium, a change in supply will set market forces in motion that lead the market to a new equilibrium price and quantity sold. • Excess Supply • A surplus is a situation in which quantity supplied is greater than quantity demanded. If a surplus occurs, producers reduce prices to sell their products. This creates a new market equilibrium. • A Fall in Supply • The exact opposite will occur when supply is decreased. As supply decreases, producers will raise prices and demand will decrease.

Shifts in Demand • Excess Demand • A shortage is a situation in which quantity demanded is greater than quantity supplied. • A Fall in Demand • When demand falls, suppliers respond by cutting prices, and a new market equilibrium is found. • Spillover costs: cost of production that affect people who have no control over how much of a good is produced (water pollution)

Search Costs • Search costs are the financial and opportunity costs that consumers pay when searching for a good/service. • Example: if a person compares prices for goods that come in different varieties, such as sweaters, depending on the type of material its made of determines the price. Searching for the lowest price for a sweater, is an example of a search cost.

Graph A shows how the market finds a new equilibrium when there is an increase in supply. Graph A: A Change in Supply Graph B: A Change in Demand $800 $600 $400 $200 0 $60 $50 $40 $30 $20 $10 Supply a b Original supply c c Price Price a b New demand New supply Demand Original demand 0 1 2 3 4 5 100 200 300 400 500 600 700 800 900 Output (in millions) Output (in thousands) Analyzing Shifts in Supply and Demand • Graph B shows how the market finds a new equilibrium when there is an increase in demand.

Section 2 Assessment 1. When a new equilibrium is reached after a fall in demand, the new equilibrium has a (a) lower market price and a higher quantity sold. (b) higher market price and a higher quantity sold. (c) lower market price and a lower quantity sold. (d) higher market price and a lower quantity sold. 2. What happens when any market is in disequilibrium and prices are flexible? (a) market forces push toward equilibrium (b) sellers waste their resources (c) excess demand is created (d) unsold perishable goods are thrown out Want to connect to the PHSchool.com link for this section? Click Here!

Section 2 Assessment 1. When a new equilibrium is reached after a fall in demand, the new equilibrium has a (a) lower market price and a higher quantity sold. (b) higher market price and a higher quantity sold. (c) lower market price and a lower quantity sold. (d) higher market price and a lower quantity sold. 2. What happens when any market is in disequilibrium and prices are flexible? (a) market forces push toward equilibrium (b) sellers waste their resources (c) excess demand is created (d) unsold perishable goods are thrown out Want to connect to the PHSchool.com link for this section? Click Here!

Combining Supply and Demand Problem Hy Feshn owns and operates a necktie boutique in one of New York City’s trendy neighborhoods. The spring weather is mild, his clientele is loyal, and overall, his business prospers. A friend in the garment district tells him, however, that the coming fall’s new fad will be the starched turtleneck shirt worn without a tie. Hy knows that fads fade quickly, but he still worries about keeping his business going during the down season sure to come. Settled in his new location, Hy stocks a new shipment of Speckle ties and raises the price to $32.50. At the same time, he lowers the price of the Spott ties to $45. The Speckle ties continue to sell so well that Hy runs out of them before his next shipment arrives. This time he raises their price to $37 and does not run out until another shipment comes in. The Spott ties still sit on the shelf, however. Hy puts them on sale for $39, at which price he just meets demand and is able to sell them steadily until he runs out of stock. He does not reorder, however, because he learns that waste dyes used in their manufacture are discoloring the waters of his favorite lake. 1. (a) What problem of excess demand does Hy face? (b) How does he remedy it? 2. In what way is Hy’s market for Spott ties in disequilibrium? 3. (a) What is the equilibrium price for Hy’s Speckle ties? (b) For his Spott ties? 4. To what spillover cost does Hy object?

Combining Supply and Demand Review • How do supply and demand create balance in the marketplace? • What are differences between a market in equilibrium and a market in disequilibrium? • What are the effects of price ceilings and price floors? • How do shifts in supply affect market equilibrium? • How do shifts in demand affect market equilibrium? • How can we use supply and demand curves to analyze changes in market equilibrium?

The Role of Prices • What role do prices play in a free market system? • What advantages do prices offer? • How do prices allow for efficient resource allocation?

Intro • Prices are the key element of equilibrium • Move markets toward equilibrium • Solves excess supply and demand • Free Market: • Prices are highly efficient in allocating or distributing resources • Centrally based economy is less efficient

The Role of Prices 1. What overall, vital role do prices play in the free market? 2. What standard do prices set? 3. What signals do high prices send to producers and consumers? 4. Why do suppliers use price rather than production to resolve the problem of excess demand? 5. What drives the distribution system in the free market? 6. How does a price-driven economy allow for a wide diversity of goods? 7. What was the goal of the Soviet planned economy? 8. How did the Soviet economic system affect consumer goods? 9. How does the free market ensure an efficient allocation of resources? 10. What motivates suppliers to increase production in the face of high demand and high prices? 11. What three problems in the free market work against the efficient allocation of resources?

The Role of Prices in a Free Market • Prices serve a vital role in a free market economy. • Prices help move land, labor, and capital into the hands of producers, and finished goods in to the hands of buyers. • Prices create efficient resource allocation for producers and a language that both consumers and producers can use.

Advantages of Prices • Prices set a standard measure of value for goods • Suppliers would have no consistent or accurate way to measure demand

Price as Incentive • Buyers and sellers look at prices to find information on a good’s supply and demand • Prices are a signal that tell consumers how much to buy & firms how much to produce • Tells consumers to think carefully before buying • More new firms will enter the market

Role of Prices • Prices can be used as signals to producers and consumers • Prices are more flexible than output levels but changing production can be costly and time consuming. • Prices can be increased to solve a problem of excess demand and decreased to eliminate the problem of excess supply • A supply shock is a sudden shortage of a good that creates excess demand • What are the options? Increasing supply is too time consuming. • Rationing or dividing goods based on something other than price is expensive and takes too long. • Rising prices is the quickest way to resolve excess demand, causing a new equilibrium.

Price System is “Free” Prices help goods flow through the economy without a central plan and is essentially costs nothing to administer. Free market pricing distributes goods through millions of decisions daily by consumers and suppliers.

A Wide Choice of Goods • A benefit of a market-based economy is the diversity of goods & services. • Price give suppliers a way to allow consumers to choose among similar prices, like a cotton sweater at $40 or a cashmere sweater at $75. • Factors such as prices, income and taste provide an easy way for consumers to narrow the choices down. • Prices allow producers to target the audience they want for a specific product. • In the USSR, one organization decides what goods are produced & how much stores will charge. To limit costs, central planners restrict production of goods to create a society in which everyone is equal. • Therefore people living in places like the Soviet Union have fewer choices than we do.

Rationing & Shortages • Rationing occurred during WWII • Food, metal & rubber created shortages at home because the soldiers had a greater need for them • The government intervened and began controlling the distribution of foods and consumer goods. • It guaranteed every civilian a minimum standard of living in wartime. • Black Market: allows consumers to buy good when unavailable

Efficient Resource Allocation • Efficient resource allocation: economic resources will be used for their most valuable purpose • Price-based systems ensures: • Resources go to the uses that consumers value most • Resource use will adjust to changing demand • Changes take place without government control

Prices and the Profit Incentive • Profit incentive motivates suppliers to increase production in the face of high demand and high prices. • For example: workers will move towards the high-paying jobs & invest in firms that pay the highest returns • Wealth of Nation • A famous book The Wealth of Nations published in 1776 by Adam Smith. Explains how businesses prosper by finding out what the population wants and then providing it. This method has been proved to be a very efficient system • Market Problems • Some exceptions in the market that do not lead to an efficient allocation of resources: • Imperfect competition: not enough of firms sell or producing that product • Spillover costs: cost of production that affect people who have no control over how much of a good is produced (water pollution) • Imperfect information: doesn’t have enough information about the product

Section 3 Assessment 1. What prompts efficient resource allocation in a well-functioning market system? (a) businesses working to earn a profit (b) government regulation (c) the need for fair allocation of resources (d) the need to buy goods regardless of price 2. How do price changes affect equilibrium? (a) Price changes assist the centrally planned economy. (b) Price changes serve as a tool for distributing goods and services. (c) Price changes limit all markets to people who have the most money. (d) Price changes prevent inflation or deflation from affecting the supply of goods. Want to connect to the PHSchool.com link for this section? Click Here!

Section 3 Assessment 1. What prompts efficient resource allocation in a well-functioning market system? (a) businesses working to earn a profit (b) government regulation (c) the need for fair allocation of resources (d) the need to buy goods regardless of price 2. How do price changes affect equilibrium? (a) Price changes assist the centrally planned economy. (b) Price changes serve as a tool for distributing goods and services. (c) Price changes limit all markets to people who have the most money. (d) Price changes prevent inflation or deflation from affecting the supply of goods. Want to connect to the PHSchool.com link for this section? Click Here!

Combining Supply and Demand Problem Hy Feshn owns and operates a necktie boutique in one of New York City’s trendy neighborhoods. The spring weather is mild, his clientele is loyal, and overall, his business prospers. A friend in the garment district tells him, however, that the coming fall’s new fad will be the starched turtleneck shirt worn without a tie. Hy knows that fads fade quickly, but he still worries about keeping his business going during the down season sure to come. Hy Feshn Neckties Hy’s first line of defense is to cut expenses. He calls Cap Hill, his congressional representative, to see if he is eligible for any government help. Cap says no, but his mother would let him have her nearby rent-controlled apartment for a fee of $500 in addition to the usual rent. Hy decides to pay the $500 and convert the cheaper second-story quarters into a boutique. Hy takes inventory before he moves and finds he has no more $30 Speckle ties but nearly his full shipment of $50 Spott ties in stock. He plans to make some adjustments after he moves. 1. In what way does Hy benefit from government price ceilings? 2. How does Hy’s experience illustrate some of the problems connected with government price intervention? 3. What part of Hy’s inventory illustrates excess supply?

Combining Supply and Demand Problem Hy Feshn owns and operates a necktie boutique in one of New York City’s trendy neighborhoods. The spring weather is mild, his clientele is loyal, and overall, his business prospers. A friend in the garment district tells him, however, that the coming fall’s new fad will be the starched turtleneck shirt worn without a tie. Hy knows that fads fade quickly, but he still worries about keeping his business going during the down season sure to come. Settled in his new location, Hy stocks a new shipment of Speckle ties and raises the price to $32.50. At the same time, he lowers the price of the Spott ties to $45. The Speckle ties continue to sell so well that Hy runs out of them before his next shipment arrives. This time he raises their price to $37 and does not run out until another shipment comes in. The Spott ties still sit on the shelf, however. Hy puts them on sale for $39, at which price he just meets demand and is able to sell them steadily until he runs out of stock. He does not reorder, however, because he learns that waste dyes used in their manufacture are discoloring the waters of his favorite lake. 1. (a) What problem of excess demand does Hy face? (b) How does he remedy it? 2. In what way is Hy’s market for Spott ties in disequilibrium? 3. (a) What is the equilibrium price for Hy’s Speckle ties? (b) For his Spott ties? 4. To what spillover cost does Hy object?

Combining Supply and Demand Problem Hy Feshn owns and operates a necktie boutique in one of New York City’s trendy neighborhoods. The spring weather is mild, his clientele is loyal, and overall, his business prospers. A friend in the garment district tells him, however, that the coming fall’s new fad will be the starched turtleneck shirt worn without a tie. Hy knows that fads fade quickly, but he still worries about keeping his business going during the down season sure to come. As the dreaded fall season approaches, a new designer offers Hy an innovative “Soopt” tie suitable for the turtleneck collar. Hy orders 500 Soopt ties, which he prices at $75. The Soopt ties sell out in less than a week, with customers asking for more. Seeing the success of her ties, the designer offers her employees more than minimum wage to attract more workers. Before long her output rises, but she still cannot keep up with orders. Her problem eases when she starts charging Hy more for his orders, but Hy does not mind. His customers will pay up to $100 for a Soopt tie, even though other designers and stores have also started offering them. 1. What price floor appears in the Soopt tie story? 2. How does price flexibility serve the market for Soopt ties? 3. What role do profit incentives play in the success of Soopt ties?