Download

1 / 12

E N D

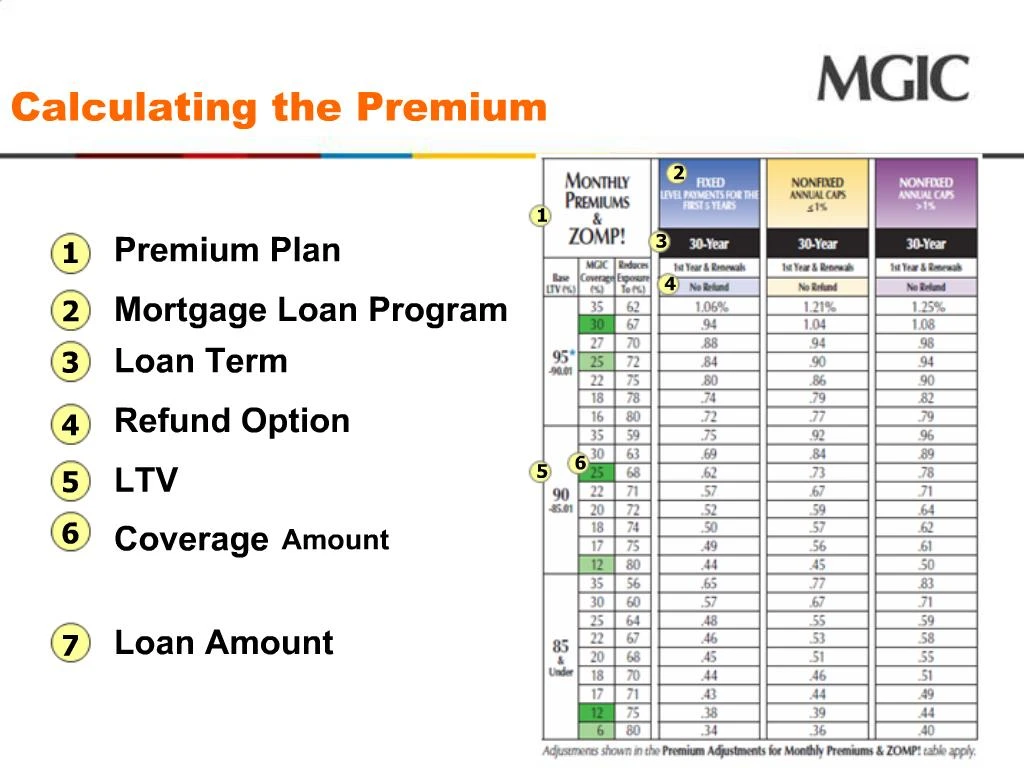

1. Calculating the Premium So how do you know what the MI premium is?

Let me cover quickly how you read an MGIC rate card.

There are seven items we need to know up front. The premium plan you want to use, of course. The mortgage loan program and term. Whether you are using a refund option or not. The LTV and the coverage amount required by your investor, and finally the loan amount.

So how do you know what the MI premium is?

Let me cover quickly how you read an MGIC rate card.

There are seven items we need to know up front. The premium plan you want to use, of course. The mortgage loan program and term. Whether you are using a refund option or not. The LTV and the coverage amount required by your investor, and finally the loan amount.

2. Calculating the Premium

3. Claim Payment Example <walk through example><walk through example>

4. Mortgage Insurance

5. 5 Mortgage Insurance Mortgage Insurance �

Required when:

LTV on a conventional loan that exceeds 80%

First lien mortgage loan exceeds 80% of the property value

Conventional loans sold in secondary market have an LTV exceeding 80%

Investors in the secondary market require insurance to ensure repayment

Insured loans are more attractive to investors because it limits or offsets potential risk

Protects lender against financial losses if the customer fails to repay the loan

There are two types of MI options:

Lender Paid MI (LPMI)

Borrower Paid MI (BPMI)

6. 6 Lender Paid Mortgage Insurance (LPMI)

Lender Paid Mortgage Insurance (LPMI)

Eliminates all mortgage insurance closing costs by incorporating the coverage into the overall price of the loan

Cost of the mortgage insurance is built into a slightly higher interest rate

In many cases the total monthly payment may be less than the total monthly payment with BPMI

The cost of LPMI may be tax deductible (depending on the customer�s situation) because it is included in the interest rate

Customers cannot be canceled or terminated unless the loan is refinanced

Accounts for about 10% of Mortgage Insurance placed for WFHM

7. 7 Borrower Paid Mortgage Insurance (BPMI) Borrower Paid Mortgage Insurance (BPMI)

Cost of mortgage insurance is a separate premium that is added to the customer�s monthly mortgage principal and interest payment

Amount of premium varies with the degree of risk

Several options available for the payment such as monthly, yearly or a one-time payment

BPMI may be tax deductible for certain income limits

Two types of cancelation procedures for BPMI �

Customer cancellation � Customer can request cancellation at 80% LTV (based on amortization for actual payments) if requirements are met

Automatic termination � Lender is required to terminated BPMI at 78% LTV (based solely on initial amortization schedule) if the loan is current

8. 8 FHA and VA Mortgage Insurance FHA and VA loans require their own types of mortgage insurance

The payments of mortgage insurance on government loans are know as:

FHA Mortgage Insurance Premium (MIP)

VA Funding Fee (VAFF)

9. 9 Impacts to Servicing The existence of Mortgage Insurance is not included in loss mitigation waterfall solutions. Better indicators are:

Income

Loan to value, combined loan to value

Debt to Income

Economic benefit of keeping the customer in the home versus foreclosing and selling the property (NPV)

In most cases, lenders are given delegated authority by the investor and the mortgage insurance company to negotiate payment arrangements, short sales, or other loss mitigation efforts on their behalf. In some cases, we are required to obtain approval from both before agreeing to terms

Critical message is encouraging customers to be in contact with their Mortgage Servicer

10. Counseling Saver Genworth Mortgage Insurance

IHOEP Spring Conference

April 2009

11. 11 Counseling Saver

12. 12 Counseling Saver

13. 13 Counseling Saver