Download

1 / 10

100 likes | 266 Views

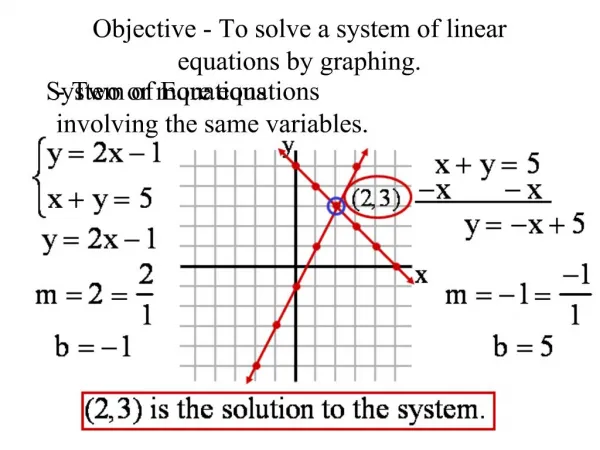

Solve a System of Two Linear Equations. Jee Hoon Choi & Chul Ou Lee. Equilibrium. Definition: a state of balance in which supply and demand meets at a point, and as a result, prices become stable Very important in economics

E N D

Solve a System of Two Linear Equations JeeHoon Choi & Chul Ou Lee

Equilibrium • Definition: a state of balance in which supply and demand meets at a point, and as a result, prices become stable • Very important in economics • When supply and demand isn’t at equilibrium, there is deadweight loss (=costs to society created by market inefficiency)

Demand • Definition: the quantity of a good or service that consumers are willing and able to purchase at a given price in a given time period • The law of demand states that “as price of product falls, quantity demanded of the product will increase”, as illustrated by the downward sloping demand curve.

Linear Demand Functions • Simple demand function: • QD = a – bP • Where QD is quantity demanded, P is price, ‘a’ is quantity demanded if the price were zero, ‘b’ is the slope of the curve • It is VERY VERY important not to confuse this linear graph with the mathematical slope-intercept form of a straight line. • The mathematical slope-intercept form: • y = mx + b • Where ‘y’ is the y-axis label, ‘x’ is the x-axis label, ‘b’ is the y-value when x is zero, and ‘m’ is the slope of the line • The math slope-intercept form isolates the y-axis label on one side, whereas the demand function isolates the x-axis label (quantity). Therefore, compared to the slope-intercept form, the demand function has switched axis.

Supply • Definition: the willingness and ability of producers to produce a quantity of good or service at a given price in a given time period • The law of supply states that “as price of a product rises, the quantity supplied of the product will also increase”, as illustrated by the upward sloping supply curve.

Linear Supply Functions • Simple supply function: • Qs = c + dP • Where, Qs is quantity supplied, P is price, ‘c’ is quantity supplied if price were zero, and ‘d’ is the slope of the curve • Same with the linear demand function, it is VERY VERY important not to confuse this function with the mathematical slope-intercept form of a straight line, as the isolated variables (y or Qs) doesn’t represent the same side of the axis

Solving Linear Functions • Solving linear functions involve finding the point where the two functions meet • Through finding this point, we’re able to find the X and the Y values, or the Equilibrium Quantity and Price. • This point is where the market is in equilibrium and will not move unless an external factor influences the market.

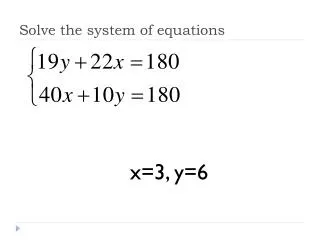

Example • QD = 2000 – 200P • Qs = -400 + 400P • Equilibrium quantity demanded and supplied: 1200 • Equilibrium price: $4 Wheat Market

Since equilibrium is found where demand equals supply, we simply need to set our two functions equal to each other. • At equilibrium, QD=Qs, so in order to find the equilibrium price: • 2000 – 200P = -400 + 400P • 2000=-400+600P • 2400=600P • P=$4

Finding Equilibrium Quantity: • QD = 2000 – 200 (4) • QD = 1200