Download

1 / 24

260 likes | 492 Views

INDIAN FINANCIAL SYSTEM AN OVERVIEW. Economic Development & Growth. An efficient, articulate and developed financial system is indispensable for rapid economic growth.

E N D

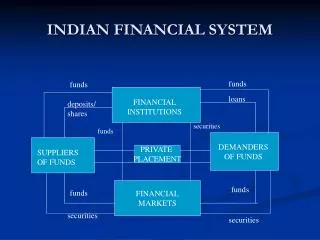

INDIAN FINANCIAL SYSTEM AN OVERVIEW

Economic Development & Growth • An efficient, articulate and developed financial system is indispensable for rapid economic growth. • The process of economic development is invariably accompanied by a corresponding and parallel growth of financial systems/organizations. However, their institutional structure, operational policies and regulatory framework differ widely and are largely influenced by the prevailing politico-economic environment. • Planned economic development in India had greatly influenced the course of financial development till the early nineties. In the post-1990s, the financial system has emerged in response to the imperatives of a liberalized/globalised/deregulated economic phase/era.

Pre-1951 The main features of the pre-1951 organization of the Indian financial system (IFS) • were: closed-circle character of industrial entrepreneurship. • A semi-organized and narrow industrial securities market devoid of issuing institutions: and the virtual absence of participation by intermediary financial institutions in the long-term finance of industry. Such a system was naturally not responsive to opportunities for industrial investment

Post-1951 The organization of the IFS during the post-1951 period evolved in response to the imperatives of planned economic development. • Planning signified the distribution of credit and finance in conformity with the planning priorities, which, in turn. implied Governmental control over the financial system. • The main elements of the IFS were: • Public/government ownership of financial institutions. • Fortification of the institutional structure, protection to investors; and participation of financial institutions (Fls) in corporate management.

Public Ownership Public ownership of Fls was brought about partly through nationalization of existing institutions • State Bank of India (1956) • LIC (1956) The setting up of the LIC, as a result of an amalgamation of 245 life insurance companies into a single monolithic state-owned institution, was a part of the deliberate and conscious attempt to mould the IFS according to the requirements of planned development. It not only transferred an important saving institution from private to public ownership, but also brought about a massive concentration of long-term funds in the hands of LIC, which emerged as the largest reservoir of long-term savings in the country

Commercial banks (1969) • GIC (1972) but mainly through the creation in the public sector, of new institutions, namely, special-purpose term-lending institutions/development banks and UTI. The setting up of the UTI was the culmination of a long overdue need of the IFS to encourage indirect holding of securities by the public.

Modification in structure & policies The fortification of the institutional structure of the IFS was partly the result of modification in the structure and policies of the existing Fls, but mainly due to the addition of new institutions. The banking policies and practices were moulded so as to be in tune with the planning practices. • Banks were encouraged to reorient their operational policies towards the financing of industry, as against commerce and trade. • They were also encouraged to enter into new forms of industrial financing, namely, underwriting and term-lending. • The banks also enlarged their functional coverage in terms of financing of small scale industries, exports and agriculture. To remedy the coverage and credit gaps to the priority sector, a scheme of social control was introduced, followed by a nationalization of the banks to control the heights of the economy and meet progressively and serve better the needs of development of the economy in conformity with national policies and objectives. • The post-nationalization period yielded significant changes in operational policies and practices of banks. This resulted in an acceleration of credit availability to the priority sector and a consequent decline in the share of large industry in the total bank credit, due to regulation and credit rationing.

Development Financial Institutions The backbone of the institutional structure of the IFS was the variegated structure of development banks, namely, IDBI. IFCI, ICICI, SFCs, SIDCs, Sites and so on. • They were conceived as instruments of the state policy of directing capital into a chosen area of industry, in conformity with the planning priorities, and of generally securing the development of private industry along the desired path, to facilitate effective public control of private enterprise. • They were also the agency through which specific socio-economic objectives of state policy, such as encouragement to new entrepreneurs and small enterprises and the development of backward regions in order to broad base the growth of industry, were being realized.

Regulatory Measures Along with the measures being taken to strengthen and diversify the institutional structure of the IFS, extensive legal reforms were carried out to provide protection to investors so as to restore their confidence in industrial securities. The main elements of the elaborate legislative code adopted by the Government were: • Companies Act • Capital Issues (Control) Act (now repealed and replaced by the SEBI Act) • Securities Contracts (Regulation) Act • MRTP Act (now replaced by Competition Act) • Foreign Exchange Regulation Act (now replaced by Foreign Exchange Management Act).

Regulatory Measures Conti…. A significant feature of the IFS was the participation by the Fls, in the management and control of companies to which finance was provided, in marked contrast to the time-honoured tradition of not getting involved in the control and management of assisted companies. This change in approach of the FIs could be ascribed to three factors: • Government policy • Structure of the industrial securities itself • The deep involvement of the Fls in the fortune of the companies through lending operations.

Emergence of Capital Market A serious lacuna in the organization of the IFS during the pre-1990 period, related to its institutional structure • Which was dominated by the development banks, which depended for resources on their sponsors (RBI, Government). • Which did not provide the ability to autonomously mobilize savings and had degenerated into a distributive mechanism. It had also resulted in a lop-sided capital structure of corporate with a heavy component of borrowed capital. The crying need of the IFS around the early nineties was the integration of the distributive mechanism with the savings pool of the community.

Emergence of Capital Market Conti.. In the post-1991 period, with a decline in the role of the Government in economic management and, as a logical corollary, in the distribution of finance and credit, the capital market has emerged as the main agency for the allocation of resources for all the sectors of the economy.

Transformation The IFS has naturally undergone major transformation. The notable developments contributing to this transformation are: • Privatization of Fls • Reorganization of the institutional structure • Introduction of an investor protection framework.

Transformation Conti… • Conversion of the IFCI into a company • The offer of equity shares to private investors by the IDBI • Steps were initiated to privatize important financial institutions. The private sector financial institutions that had come into being are the new generation of banks under the RBI guidelines; mutual funds under SEBI regulations, sponsored by Fls. FIIs, banks and insurance organizations; and insurance companies sponsored by both domestic and foreign promoters, under IRDA guidelines. Pension funds are poised to be opened for private entities with the setting up of the PRDA.

Transformation Conti… With the impending reorganization/liquidation of the IFCI Ltd. and the IIBI Ltd. and the conversion of the ICICI and the IDBI into banks, the development banks which constituted the backbone of the organization of the IFS, have virtually disappeared from the Indian financial scene, the only surviving institution being the SFCs.

Transformation Conti… The institutional structure of the IFS has undergone an outstanding transformation in its evolution to reflect its capital market-orientation. The components which witnessed the transformation are • Development banks/term-lending • Fls/public financial institutions • Commercial banks • Insurance companies, Mutual Funds, NBFCs and Securities/Capital market and Money Market.

Banking System Indian banking is characterized by prudential/viable banking. • By the early nineties, a geographically wide and functionally diverse banking system had emerged, as reflected in the phenomenal branch expansion, especially in the rural and semi-urban and unbanked areas. • The phenomenal growth in deposits and the increase in the share of priority sector in total bank lending. This impressive progress of Indian banking in achieving social goals had indeed been a major developmental input. • However, serious weaknesses developed in the form of decline in the efficiency of the banking system and consequently, a serious erosion of its profitability, with adverse implications for its vi-ability itself.

Banking Reforms The first generation of reforms, as a follow-up to the Narsimham Committee I recommendations, focused on: • Arresting the qualitative deterioration in the functioning of the banking system in terms of directed investments: directed credit programs; the interest rate structure: capital adequacy norms; income recognition, asset classification and provisioning norms and so on.

Banking Reforms Conti.. The second generation of reforms, as a follow-up to the Narsimham Committee II recommendations, addressed the issue of making the banking system internationally competitive. • The focus shifted to internal financial management of banks, in contrast to the regulatory compliances until then. The major components of internal financial management are: rigorous prudential norms relating to credit/investment portfolio and capital adequacy; debt recovery tribunals, corporate debt restructuring, and securitization, asset reconstruction and enforcement of security interest to en-sure speedy/effective NPA recovery/ management; asset-liability management; credit risk management: and operational risk management.

Impact of Reforms • With the entry of private insurance companies, the monopoly of the public sector LIC and GIC has been dismantled. • Mutual funds have emerged as the most preferred route of institutionalization of security investments for the relatively small investors. • NBFCs broaden the range of financial services, both fund-based and fee-based. They operate within the rigorous framework of RBI's directions relating to acceptance of public deposits, prudential norms and auditors, reports.

Impact of Reforms Continue.. The securities/capital market has witnessed the most profound transformation. From being a marginal institution in the mid-eighties, it has come to occupy the centre stage in the IFS. The structure of both the primary and the secondary market is characterized by significant changes. • The reforms of the intermediaries as well as the pre and post-issue procedure and activities, are indeed thorough going, as a consequence of which the primary market organization has assumed, highly developed character, capable of catering to the requirements of the sophisticated and articulate securities market. • The secondary market, which represented an institutional mechanism that was inadequate. non-transparent, hardly regulated and rarely geared to investor protection, has been truly trans-formed. The notable developments relate to intermediaries, reorganization of stock exchanges, trading and so on.

Impact of Reforms Continue.. The money market in India, had a narrow base and a limited number of participants: there were no participants who would alternate between lending and borrowing to develop an active market: there was a paucity of instruments in the market; and interest rates were regulated. A sophisticated and articulate money market has now emerged. Along with deregulation of interest rates and enlargement of participants, there are a number of inter-related sub-markets: call market. 1-bills market, commercial bills market, CPs market, CDs market, repo and so on. The money market intermediaries are PDs and MFs.

Focus Although a fairly comprehensive legislative code had been built up earlier, the focus was on control. The framework was fragmented. both in terms of the laws/acts under which the regulatory function fell and the agencies/government departments that administered them. The need for a focused/ integrated regulatory framework, administered by an independent/autonomous body, found expression in the establishment of the SEBI. Its main function is to protect the interest of the investors in securities and to promote the development and regulation of the securities market. The SEBI exercises power under the SEBI Act, SCRA, Depositories Act and delegated powers under the Companies Act. It regulates and supervises the securities market through a number of regulations/guide-lines and schemes