Download

1 / 38

390 likes | 595 Views

Post-Keynesian monetary theory and policy in an open economy. Marc Lavoie. My interpretation of PK theory based on….

E N D

Post-Keynesian monetary theory and policy in an open economy Marc Lavoie

My interpretation of PK theory based on… • Two papers that I wrote in the JPKE (2000, 2002-3), about forward exchange markets, based on the so-called cambist approach, developed in the 1970s by French practioners and scholars, one of which was my teacher in 1976-77. • A book chapter that I wrote in 2001 about the sterilization of foreign exchange reserves, based on the ideas developed by the same practioners (the Banque de France view), also found in my 1992 book. • My understanding of the clearing and settlement process in Canada, as expressed by the practioners at the Bank of Canada who developed this system. • My collaboration with the late Wynne Godley, in particular three papers that we wrote on stock-flow consistent two- or three-country models, which reinforced my convictions about the validity of the PK monetary theory in an open economy Jornadas de Economia Politica, UNQ, Argentina, 2012

Outline • Forward exchange markets and covered interest parity • The impossible trinity and the Rules of the Game • The compensation thesis or endogenous sterilization • Historical examples • Modern examples • The eurozone in an SFC model Jornadas de Economia Politica, UNQ, Argentina, 2012

The interest parity theorem: a rejection • The neoclassical interest parity theorem comprises two relations: covered interest parity (CIP) and uncovered interest parity (UIP). • UIP: nominal interest rates (in a riskless environment with perfect asset substitutability and perfect capital mobility) are equal to world interest rates plus the expected change in the exchange rate: R = R* + (se – s) • CIP: interest rate differentials must be equal to the forward exchange premium (or discount) relative to the spot exchange rate: (R – R*) = f– s • Therefore, UIP and CIP implies that the forward exchange rate and the expected future spot exchange must be equal: f = se. • Therefore, if markets have correct expectations on average, the forward exchange rate should be a good predictor of realized future spot exchange rates: f = s(+1). Jornadas de Economia Politica, UNQ, Argentina, 2012

The forward exchange rate is not a predictor of future spot rates • CIP is always observed, provided we note, in the case of capital controls, that the forward rate paid by a national resident may be different from that paid by a foreign customer, as euro-markets will be partly disconnected from the domestic money markets. • The current spot rate, not the current forward rate, is the best predictor of future spot rates. Changes in the forward rate are useless to predict future changes in the spot rate. • The spot rate exchange rate is related to the contemporaneous, rather than the lagged, forward exchange rate (Moosa 2004). • It implies the failure of the so-called unbiased efficiency hypothesis. Jornadas de Economia Politica, UNQ, Argentina, 2012

A reinterpretation of CIP • The forward exchange rate is not an expectational variable. • It is the result of a simple arithmetic operation, conducted by cambists. • Banks hedge their forward exchange market operations, they do not arbitrage as such. • When a customer wishes to purchase dollars forward, banks cover themselves by borrowing pesos at the rate R and buying dollars spot, and placing these dollars at the rate R*. • Banks set the forward rate by adding a simple mark-up (or mark-down) to the spot rate, determined by the differential in interest rates on interbank markets : f= s + (R – R*) Jornadas de Economia Politica, UNQ, Argentina, 2012

Implications of the cambist view • An obvious implication is that covered interest arbitrage has no impact whatsoever on spot rates or foreign reserves when exchange rates are fixed. • Only uncovered forward exchange operations induce inflows or outflows, and these can be countered by forward exchange market operations by the central bank. • Monetary authorities can renew these operations as long as they have the nerves to face the possibility of losing their foreign reserves in the future. • Monetary authorities do have some leeway in setting domestic interest rates, including real rates, both in a flexible and a fixed exchange rate regime. • With fixed exchange rates, the interest rate differential is limited by the width of the intervention band (4% differentials for 3-month T-bills are permitted by 1% spot rate differentials) Jornadas de Economia Politica, UNQ, Argentina, 2012

The fixed exchange rate case • This goes against the usually asserted claim, associated with the mainstream Mundell-Fleming model, that there is no such choice in a fixed exchange rate regime. • Its main assertion is that an economy operating with fixed exchange rates would lose control of the money supply, and hence that monetary policy is ineffective (in contrast to the situation with flexible exchange rates). • The mainstream claim is that a central bank gaining (losing) reserves would see its monetary base grow (diminish) and hence interest rates would drop (rise). • The money supply here is endogenous, but supply-led. • (in the PK view the money supply is endogenous, but demand-led). Jornadas de Economia Politica, UNQ, Argentina, 2012

The impossible trinity – the trilemma • The Mundell-Fleming model has given rise to the claim of the impossible trinity. As is well-known in Latin America, mainstream authors claim that one cannot have together: • Fixed exchange rates; • Capital mobility; • An independent monetary policy (Home-made interest rates set by the central bank). • Such a claim relies: • on the mistaken belief in the relevance of the unbiased efficiency hypothesis, • on the confusion between perfect capital mobility and perfect asset substitutability, • on the ignorance of the compensation principle, • and on the inability to distinguish between countries in BOP deficit and surplus positions. • . Jornadas de Economia Politica, UNQ, Argentina, 2012

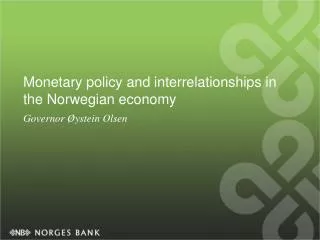

The standard view of the impact of a balance of payment surplus on the balance sheet of the central bank Jornadas de Economia Politica, UNQ, Argentina, 2012

The (neoclassical) rules of the Game • “In order to maintain a fixed exchange rate, a central bank must engage in foreign exchange transactions that prevent it from managing the monetary base so as to achieve other macroeconomic objectives. If monetary policy is dedicated to pegging the exchange rate, it is then unavailable (except on a highly temporary basis) for application to other goals.” (McCallum, 1996, pp. 139-140). • “The Rules of the Game must be such that a balance of payments deficit should be fully reflected in a reduction in the supply of money, and a surplus should be fully reflected in an increased money supply” (Ethier 1988: 341). Jornadas de Economia Politica, UNQ, Argentina, 2012

The rules of the game are not automatic • Mundell (1961), whose other works are often invoked to justify the relevance of the rules of the game in textbooks and the IS/LM/BP model, was himself aware that the automaticity of the rules of the game relied on a particular behaviour of the central bank. • Indeed he lamented over the fact that modern central banks were following the banking principle instead of the bullionist principle, and hence adjusting ‘the domestic supply of notes to accord with the needs of trade’ (1961, p. 153), which is another way to say that the money supply was endogenous and that central banks were concerned with maintaining the targeted interest rates. Jornadas de Economia Politica, UNQ, Argentina, 2012

Sterilization in the neoclassical view Jornadas de Economia Politica, UNQ, Argentina, 2012

What about sterilization ? • The effect on the stock of base money of a purchase of foreign currency can be undone by the sale of government securities by the central bank. This is sterilization. • It is usually argued that sterilization cannot be pursued for very long or is ineffective. • For Claassen (1996) [and also McCallum (1996)], ‘in the context of “perfect capital mobility” ... sterilized intervention policies are doomed to be ineffective’. • In our opinion, such statements confuse perfect capital mobility with perfect asset substitutability. • They also do not distinguish between countries that are in a current account deficit situation and losing reserves, and those that are in a surplus situation and gaining reserves (say China). Jornadas de Economia Politica, UNQ, Argentina, 2012

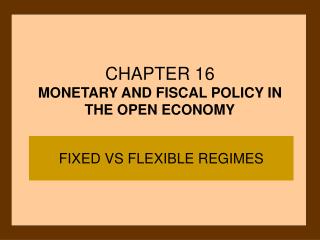

Another, new, argument against sterilization, or on the limits of sterilization • In the context of Latin American countries, Frenkel (2006, p. 587) writes that sterilization operations: “consist in the selling of public-sector or central bank papers with the objective of money absorption. They imply a financial cost to the treasury or the central bank, proportional to the difference between the interest rate of those papers and the interest rate earned by the central bank’s international reserves”. Jornadas de Economia Politica, UNQ, Argentina, 2012

The opportunity cost of sterilization if interest rates are high in the domestic economy (the case of a surplus economy) Jornadas de Economia Politica, UNQ, Argentina, 2012

An answer to this new argument • It is true that the costs of sterilization could be such that the central bank would make zero profits or even operating losses. • This would reduce to zero the profits that the central bank usually distributes to the government, thus reducing the government budget balance. • If the losses of the central bank are so large that it becomes technically insolvent, the government would then need to sell newly-issued securities, that would be purchased by the central bank, with the proceeds being invested into the central bank, so as to raise the own funds of the central bank. Jornadas de Economia Politica, UNQ, Argentina, 2012

The compensation thesis • The essential features of the Post Keynesian approach to monetary economics are that credit and money are demand-led endogenous variables, and that central banks can control interest rates, within large bounds. • Through the reflux principle, balance of payments disequilibria have no effect on the overall monetary base or money supply, even with fixed exchange rates. Money aggregates are still determined by demand-led factors. The only difference is that these foreign-induced disequilibria will change the composition of the balance sheet of the central bank. • As Arestis and Eichner (1988: 1018) say, “government deficits and a favorable balance of payments have no direct effect on the creation of money, for any money thus created is completely compensated by an equivalent reduction in credit money”. Jornadas de Economia Politica, UNQ, Argentina, 2012

A PK, more realistic, balance sheet of central banks, with compensation Jornadas de Economia Politica, UNQ, Argentina, 2012

History shows that the rules of the game never held, even during the gold exchange regime • Bloomfield (1959, p. 49) shows that when looking at year-to-year changes in the period before the First World War – the heyday of the gold standard – the foreign assets and the domestic assets of central banks moved in opposite directions 60% of the time. Foreign assets and domestic assets moved in the same direction only 34% of the time for the eleven central banks under consideration. • The prevalence of a negative correlation thus shows that the so-called Rules of the Game were violated more often than not, even during the heyday of the gold standard. Indeed, ‘in the case of every central bank the year-to-year changes in international and domestic assets were more often in the opposite than in the same direction’ (Bloomfield, 1959, pp. 49-50). Jornadas de Economia Politica, UNQ, Argentina, 2012

Further results • Almost identical results were obtained in the case of the 1922-1938 period. • Ragnar Nurkse (1944, p. 69) shows that the foreign assets and the domestic assets of twenty-six central banks moved in opposite direction in 60% of the years under consideration, and that they moved in the same direction only 32% of the time. • Studying the various episodes of inflows or outflows of gold and exchange reserves, Nurkse (1944, p. 88) concludes that ‘neutralization was the rule rather than the exception’. Without saying so, Nurkse adopts the compensation principle as the phenomenon ruling central banks in an open economy. The rules of the game as they were to be endorsed in the modern IS/LM/BP models of Mundell are an erroneous depiction of reality. Jornadas de Economia Politica, UNQ, Argentina, 2012

The compensation thesis • Bloomfield and Nurkse have uncovered what was later to be called the compensation thesis. • The compensation thesis is sometimes called the Banque de France view, because in its modern incarnation it was endorsed by Pierre Berger, who was the general director of research at the Banque de France. • Berger (1972a, 1972b) points out that the compensation phenomenon that can be observed in modern economies could already be observed in the 19th century. • Berger argues that when France had large external surpluses, and hence was accumulating gold reserves, the peaks in the gold reserves of the Banque de France were accompanied by throughs in credits to the domestic economy. • As a result, despite the wide fluctuations in gold reserves, the variations in the monetary base and the money supply were quite limited. Jornadas de Economia Politica, UNQ, Argentina, 2012

Nurkse and the compensation thesis • “There is nothing automatic about the mechanism envisaged in the “rules of the game”. We have seen that automatic forces, on the contrary, may make for neutralization. Accordingly, if central banks were to intensify the effect of changes in their international assets instead of offsetting them or allowing them to be offset by inverse changes in their domestic assets, this would require not only deliberate management but possibly even management in opposition to automatic tendencies.” • (Nurkse, 1944, p. 88) Jornadas de Economia Politica, UNQ, Argentina, 2012

Active sterilization or passive compensation? • Nurkse’s rejects the standard interpretation in terms of a ‘sterilization’ operation initiated by the central bank. • Nurkse considers that it would be ‘quite wrong to interpret [the inverse correlation] as a deliberate act of neutralization’ on the part of the central bank. • On the opposite, Nurkse considers that the neutralization of shifts in foreign reserves is caused by ‘normal’ or ‘automatic’ factors, and that the compensation principle operates both in overdraft financial systems and in the asset-based ones. • In the overdraft system, Nurkse (1944, p. 70) notes that ‘an inflow of gold, for instance, tends to result in increased liquidity on the domestic money market, which in turn may naturally lead the market to repay some of its indebtedness to the central bank’. Jornadas de Economia Politica, UNQ, Argentina, 2012

Active sterilization or passive compensation? (2) • But Nurkse also observed compensating phenomena that were consistent with the operation of an asset-based financial system. • In the case of an inflow of gold and foreign exchange, foreign investors (or the banks where their deposits would be held) would purchase new government securities. • This would allow Government to reduce its debt to the central bank, as would be the case in an open-market operation. • However, as Nurkse (1944, p. 77) points out, in contrast to the usual open-market operation, the manoeuvre ‘did not come about at the Bank’s initiative’. • Alternatively, Nurkse (1944, p. 76) points out, gold inflows could also be neutralized by an increase in government deposits held at the central bank, as the Bank of Canada used to do. Jornadas de Economia Politica, UNQ, Argentina, 2012

Even Keynes recognized the compensation principle • Keynes (1930, ch. 32) was also keenly aware of the compensation phenomenon. • He points out that year after year the Bank of England would gain £10,000,000 of gold in the spring and lose a similar amount in the autumn. This should have caused concern to all, but it did not, because these inflows and outflows were compensated by corresponding seasonal outflows and inflows arising from the Treasury. • In the spring, with the receipts of income tax, the Treasury would buy back its securities from the public and from the Bank of England, thus reducing the domestic credit entry in the balance sheet of the Bank of England. Jornadas de Economia Politica, UNQ, Argentina, 2012

A PK, more realistic, balance sheet of central banks Jornadas de Economia Politica, UNQ, Argentina, 2012

An obvious case of endogenous sterilization: Germany Jornadas de Economia Politica, UNQ, Argentina, 2012

The Canadian case, before giving up exchange rate interventions in 1997 Jornadas de Economia Politica, UNQ, Argentina, 2012

The case of Argentina (Frenkel and Rapetti 2008) Jornadas de Economia Politica, UNQ, Argentina, 2012

Central banks always pursue sterilization and say so • In a background paper, the Bank of Canada (2003) explains that when it conducts exchange rate operations, moderating a decline in the Canadian dollar for instance, it must sterilize its purchases of Canadian dollars by ‘redepositing the same amount of Canadian-dollar balances in the financial system’, in order ‘to make sure that the Bank’s purchases do not take money out of circulation and create a shortage of Canadian dollars, which could put upward pressures on Canadian interest rates’. • Similarly, when the Bank wishes to slow down the appreciation of the dollar and sells Canadian dollars on the exchange markets, thus acquiring foreign currency, ‘to prevent downward pressure on Canadian interest rates ... the same amount of Canadian-dollar balances are withdrawn from the financial system.’. • Thus sterilization is not a matter of choice, it is a necessity as long as the central bank wants to keep the interest rate at its target level. Jornadas de Economia Politica, UNQ, Argentina, 2012

The current Eurozone case • What happens if depositors move their money away from PIIGS banks or if the PIIGS run a current account deficit? • Normally such imbalances are absorbed by counteracting movements in the overnight or wholesale funds markets. • However, Northern banks are now declining to provide loans to Southern banks. • Assume Italy has a current account deficit, importing too many goods, while Germany has a current account surplus. • The TARGET2 system will absorb all this smoothly. • Compensation phenomena will also arise. Jornadas de Economia Politica, UNQ, Argentina, 2012

Sterilization at the Bundesbank Target2 balances Claims on banks Jornadas de Economia Politica, UNQ, Argentina, 2012

There is no need for sterilization (in a BOP surplus position) when there is a floor system (Switzerland July-September 2011, with target rate at 0 to 0.25% !) Interest rate S July S’ Sept ceiling Lending rate Demand for reserves Target rate and Deposit rate 0.25% floor Reserves Jornadas de Economia Politica, UNQ, Argentina, 2012

Godley stock-flow consistent (SFC) models and the compensation thesis • It can be shown that interest rates can be kept constant in a open economy SFC model with a fixed exchange rate and a surplus or deficit BOP. • Compensation will occur automatically in such a model. 2012 Jornadas de Economia Politica, UNQ, Argentina, 2012

The eurozone: Effect on various balances of an increase in the propensity of the ‘& Greece’ country to import products from the ‘$’ country (flexible euro/$ rate) Germany Greece Jornadas de Economia Politica, UNQ, Argentina, 2012

Evolution of the assets and liabilities of the European Central Bank following an increase in the propensity of the ‘& Greece’ country to import products from the ‘$ USA’ country, so as to keep interest rates equal in both countries. But the ECB, up until May 2010, refused to hold government securities! Greek T-bills German T-bills Jornadas de Economia Politica, UNQ, Argentina, 2012