Download

1 / 16

160 likes | 305 Views

Identity Fraud Expense Coverage. Kimberley A. Ward KimW@AAISonline.com CAS Ratemaking Seminar, March 2004. Topics for Discussion. About AAIS Examples of Identity Theft Endorsement Coverages Pricing the Product Availability of Materials Your Questions. About AAIS.

E N D

Identity Fraud Expense Coverage Kimberley A. Ward KimW@AAISonline.com CAS Ratemaking Seminar, March 2004

Topics for Discussion • About AAIS • Examples of Identity Theft • Endorsement Coverages • Pricing the Product • Availability of Materials • Your Questions

About AAIS • Advisory Organization, formed in 1975 • 20 Lines of Business • Forms, Rules, and Rating Information • Statistical Reporting • Technical Support Services

What is Identity Fraud? • Use of another person’s personal identifying information without permission • Includes • Purchasing goods and/or services • Obtaining credit • Borrowing money • Obtaining employment • Committing crimes • Became a federal crime in 1998

How does it happen? • Loss or theft of identifying papers • Documents in the trash • Theft of mail • Employee dishonesty • Internet shopping or spam email (“Phishing”)

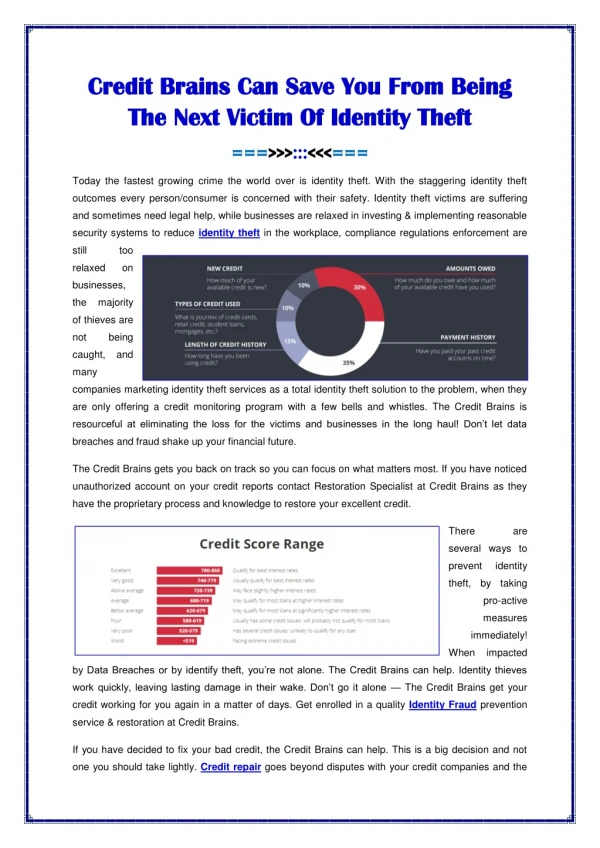

How widespread is it? • Reports to FTC Clearinghouse almost double every year since 1998. • FTC Identity Theft Survey released in September, 2003, found that 27.3 million victims over the last 5 years, 9.9 million in the last year alone. • These numbers include two types of losses • Account theft (17 million; 6.6 million) • ID theft (10 million; 3.3 million)

What does it cost consumers? • Damaged credit • Collection agencies • Criminal Record/Civil Suits • Insurance/Utilities/Employment • CASH $$$ • $5 billion in out of pocket expenses in the last year, according to FTC Survey • Victims of ID theft have more than 3 times the expenses of victims of account theft • $5 billion does not include time lost at work, etc.

Identity Fraud Expense Coverage • Endorsement and manual supplement for non-AAIS affiliates • Endorsement will require customization • Insured selects limit, shown on endorsement or declarations

New Definitions • “Identity Fraud” is the use of personal identifying information of an insured without permission, in a manner that violates federal, state, or local law • “Expenses” means • Costs to obtain, reproduce, or notarize required documents • Costs to send required documents • Costs for telephone calls • Research fees • Loss of earnings (no more than $250 per day per insured and total of $5,000 for all insureds.) • Loan application fees • Attorney fees with company’s prior consent

Coverage Period • Coverage provided for expenses incurred as a result of identity fraud: • Occurring any time prior to the policy period, and • Discovered during the policy period or up to one year after. • Coverage applies even if perpetrator(s) are not identified • No coverage for expenses • Business related • Insured committing fraud • Fraud discovered prior to policy • Fraud discovered after one year after end of policy

A few more things • Insured selects per occurrence limit • Deductible of $100 applies • Series of acts committed by one person is considered one occurrence • Limit does not accumulate from policy period to policy period • Coverage is excess over other insurance or types of redress • Policy conditions are modified to allow for “Discovery” basis • Supplement provides rating information for limits of $5,000, $10,000, $15,000, $20,000, $25,000, and $30,000, plus rating for each addl $5,000.

Pricing • Pricing based upon GAO 3/2002 report: Identity Theft: Prevalence and Cost Appear to be growing • Includes monetary loss information as reported to the FTC Clearinghouse • Early reporters may not know extent of monetary damages • Monetary damages include long distance calls, document copies, fees, postage, attorney fees

Pricing • Further…non-monetary damages are reported to the FTC Clearinghouse • include time lost from work, that is considered a monetary loss under the new endorsement • Price should reflect that coverage is provided on a discovery basis, which is broader coverage

Pricing - Adjustments to data • Trend and ALAE: to reflect that these costs are increasing over time and the cost of ALAE • adjustment is 20% • Development: since the majority of the reported incidents do not reflect the final cost to the victim • assumed 80% would be in the next cost range up, special treatment for “no cost” fraud claims • 80% of the reports to FTC indicating no monetary losses were distributed to the other categories proportionally

Pricing - Final Selections • Assumed frequency is 500,000 fraud reports per year from approximately 150 million adults (0.0033) • Projected severity for 15,000 limit is $5,857 per claim • Selected loss cost = $25 • Additional loss costs for other limits

Availability • AAIS will make endorsement and supplement available to non-affiliated companies • Contact Rick Anderer, at800-564-AAIS or RichardA@AAISonline.com • Additional questions can be answered by me at KimW@AAISonline.com.