Download

1 / 24

240 likes | 249 Views

FCS is a system that brings together findings with the same content but different titles, enabling the production of statistics. It helps the Turkish Court of Accounts in auditing public entities and identifying findings. The system aims to overcome the time-consuming structure of preparing general reports and provides opportunities for effective follow-up mechanisms.

E N D

FINDING CLASSIFICATION SYSTEM Turkish Court of Accounts - TCA

What Is FCS? This is a systemthat enables to produce statistics as bringing the findings together that have thesame content but different finding titles. As Turkish Court of Accounts, weaudit; • Nearly 400 publicentities. • Nearly 7000 findingsareidentifiedyearly.

What Is FCS? Same Content DifferentTitlesReportedByTheDifferentAuditors. QuiteDifficultToProduceStatistics

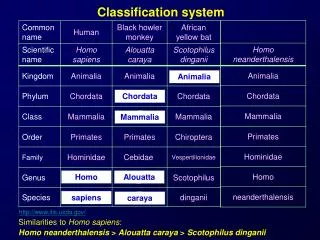

What Is FCS? Thesearefourpublicentities’ findings. Althoughthefindingtitlesaredifferentfromeachother, all of thefindingsareaboutlack of accountingrecordregarding bank accounts. Sowebroughtallthesefindingstogetherundertheuniquesubject of ‘The Existence Of Bank Accounts Not Recorded In The Financial Statements.’

TheScope of theSystem Thereare 3 types of findings in Regularityaudit: • Findings Effecting Financial Reports And Statements, • Findings Related To Compliance, • The Assessments Regarding Financial Management And Internal Control Thesystem is based on theclassification of onlyFindings Effecting Financial Reports And Statementsfornow. Theprocess of theclassification of othertypes of findings is in progress.

Why Do We NEED IT? Main Motive ToOvercomeThe Time ConsumingStructure Of Preparing General Reports CreatesMuchMoreOppotunities

Why Do We NEED IT? • The main idea behindsettingupsuch a system is desinging a sytemtoprepareTheExternalAudit General Report effectively. • TheExternalAudit General Report is one of the general reportthatwesubmittothe Grand National Assembly. • Thisreportincludestheissuesthataregenerallyfoundin theauditreports of theseveralpublicentities. Inordertodeterminethoseissuesweexaminedallauditreportsonebyone. Since thisduty is quiteheavyand time consuming, an effectivesystem is needed. • Evenifthis is our main aimtodesignthesystem, werealizedthat it wouldprovidemuchmoreopportunities.

ExpectedOutcomes of theSystem • Tomeasuretheaddedvalue of audit • To form effectivefollow-upmechanism • Toproducestastisticsaboutfindings • To form an auditdatabaseforauditors

Tomeasuretheaddedvalue of audIt • Thesystem is expectedtomonitorthefrequency of identification of spesificissuesbyyears. • Whenwecomparethenumber of findingsregardingthespesifictopicsbyyears, thedeclinemightimplythecontribution of theaudits.

To form effectIvefollow-upmechanIsm • Thesystem is expectedtoensuretomonitorwhethertherecommendations of auditfindingshavebeenfulfilled on thebasis of publicentitiesbyyears.

ToproducestastIstIcsaboutfIndIngs • It is possible to produce different types of statistics through this system. • Thesestatisticsarewidelyusedby TCA in the framework of accountability and fiscal transparency in the public sector. • Withthehelp of thissystem, TCA willprovidestatisticstoThe Grand National Assembly andpublicentitiesandwillinformthe publiccorrectly.

To form an audItdatabaseforaudItors • Thereareapproximately 900 specificsubjects in thesystemandtheyarevisibletoauditors in SayCap . • Inthecourse of audit, auditorsmaybenefitfromthesesubjectsandthisdatabasemaypromptthemtoexaminethesubjectstheydeemappropriate

How DoesTheSystemWork? • Thesystem is integratedto SAYCAP (Audit Management System). • When an auditoridentify a finding effectingfinancialreportsandstatements, he insertsthetitletotitlebox at the top leftcorner. • Then, he has tochoosetheaffectedaccountgroup, andthesubject of thefindingfromthecomboboxlocated at theleftside of thescreen. • Inthiscomboboxthereare 70 accountgroupsandnearly 900 uniquesubjectsassociatedwithaccountgroups.

How DoesTheSystem Report? • Afterall of the data entriescompleted, system can producereportsincludingthetitlesshown here. • Bymeans of thesetitles it is possibletoproducemanytypes of statisticsneeded. • Thesestatisticsmight be; 1- How manyfindingidentified on thebasis of thebudgettype in a specificyear? 2- How manyfindingidentified on thebasis of publicentityovertheyears? 3- What is themostidentifiedfinding in Auditreports? Andso on.

FIrstOutcomes (BASED ON mostlyIdentIfIedfIndIngs IN 2017 ) • Whenweneedtoanalyzethefirstoutcomes of thesystem, thesearethe 10 mostlyidentifiedfindingstakingplace in auditreports in 2017. • You can see here thenumber of publicentitiescorrespondingtosubjectsidentified. We can see how widely is a subjectidentified.

FIrstOutcomes(BASED ON TheChanges IN THE NUMBer OF FINDINGs BY YEARS)

FIrstOutcomes(BASED ON TheChanges IN THE NUMBer OF FINDINGs BY YEARS) • Thankstothesystem, it is alsopossibletoobtainstatisticsbased on thechanges in thenumber of findingsbyyears. • thenumber of identificationforsomefindingsdecreased in 2017 whilethere is an increaseforsomeothers . • Theresult is goingtoshow us whichareashouldwefocuswhiledetectingtheriskyareasorcarryingouttheaudit.

FIrstOutcomes(BASEd On Changes IN THE NUMBerOF SpecIFICFINDING BY YEARS AND BY ENTITY)

FIrstOutcomes(BASEd On Changes IN THE NUMBerOF SpecIFICFINDING BY YEARS AND BY ENTITY) • Anotherstatisticwe can obtain form thesystem is thechange of thenumbers on thebasis of spesificfindingbyyearsandpublicentity. • Thiswillprovide us an opportunitytosupportthefollowupprocess of previousyears’ audits.

Thank you for your attention… Turkish Court of Accounts - TCA