Download

1 / 63

650 likes | 904 Views

Engineering Economics. Fundamentals: EIT Review. Hugh Miller Colorado School of Mines Mining Engineering Department Fall 2008. Basics. Notation Never use scientific notation Significant Digits

E N D

Engineering Economics Fundamentals: EIT Review Hugh Miller Colorado School of Mines Mining Engineering Department Fall 2008

Basics • Notation • Never use scientific notation • Significant Digits • Maximum of 4 significant figures unless the first digit is a “1”, in which case a maximum of 5 sig figs can be used • In general, omit cents (fractions of a dollar) • Year-End Convention • Unless otherwise indicated, it is assumed that all receipts and disbursements take place at the end of the year in which they occur. • Numerous Methodologies for Solving Problems • Use the method most easy for you (visualize problem setup)

Concept of Interest If you won the lotto, would you rather get $1 Million now or $50,000 for 25 years? What about automobile and home financing? What type of financing makes more economic sense? Interest: Money paid for the use of borrowed money. • Put simply, interest is the rental charge for using an asset over some period of time and then, returning the asset in the same conditions as we received it. → In project financing, the asset is usually money

Why Interest exist? Taking the lender’s view of point: • Risk: Possibility that the borrower will be unable to pay • Inflation: Money repaid in the future will “value” less • Transaction Cost: Expenses incurred in preparing the loan agreement • Opportunity Cost: Committing limited funds, a lender will be unable to take advantage of other opportunities. • Postponement of Use: Lending money, postpones the ability of the lender to use or purchase goods. From the borrowers perspective …. Interest represents a cost !

Simple Interest Simple Interest is also known as the Nominal Rate of Interest • Annualized percentage of the amount borrowed (principal) which is paid for the use of the money for some period of time. Suppose you invested $1,000 for one year at 6% simple rate; at the end of one year the investment would yield: $1,000 + $1,000(0.06) = $1,060 This means that each year interest gives $60 How much will you earn (including principal) after 3 years? $1,000 + $1,000(0.06) + $1,000(0.06) + $1,000(0.06) = $1,180 Note that for each year, the interest earned is only calculated over $1,000. Does this mean that you could draw the $60 earned at the end of each year?

Terms In most situations, the percentage is not paid at the end of the period, where the interest earned is instead added to the original amount (principal). In this case, interest earned from previous periods is part of the basis for calculating the new interest payment. This “adding up” defines the concept of Compounded Interest Now assume you invested $1,000 for two years at 6% compounded annually; At the end of one year the investment would yield: $1,000 + $1,000 ( 0.06 ) = $1,060 or $1,000 ( 1 + 0.06 ) Since interest is compounded annually, at the end of the second year the investment would be worth: [ $1,000 ( 1 + 0.06 ) ] + [ $1,000 ( 1 + 0.06 ) ( 0.06 ) ] = $1,124 Principal and Interest for First Year Interest for Second Year Factorizing: $1,000 ( 1 + 0.06 ) ( 1 + 0.06 ) = $1,000 ( 1 + 0.06 )2 = $1,124 How much this investment would yield at the end of year 3?

Solving Interest Problems Step #1: Abstracting the Problem • Interest problems based upon 5 variables: P, F, A, i, and n • Determine which are given (normally three) and what needs to be solved

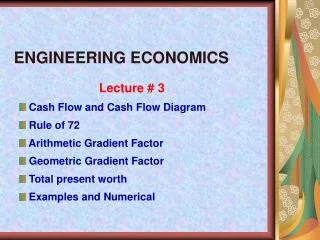

F A1 A2 A3 A4 A6 A5 Cash Flow - + Time P Solving Interest Problems Step #2: Draw a Cash Flow Diagram Receipts Disbursements

Interest Formulas The compound interest relationship may generally be expressed as: F = P (1+r)n(1) Where F = Future sum of money P = Present sum of money r = Nominal rate of interest n = Number of interest periods Other variables to be introduced later: A = Series of n equal payments made at the end of each period i = Effective interest rate per period Notation: (F/P,i,n) means “Find F, given P, at a rate i for n periods” This notation is often shortened to F/P

Interest Formulas r = Nominal rate of interest i = Effective interest rate per period • Nominal Interest is the periodic interest rate times the number of periods per year: Nominal annual interest rate of 12% based upon monthly compounding means 1% interest rate per month compounded • When the compounding frequency is annually: r = i • When compounding is performed more than once per year, the effective rate (true annual rate) always exceeds the nominal annual rate: i > r

Future Value Example: Find the amount which will accrue at the end of Year 6 if $1,500 is invested now at 6% compounded annually. Method #1: Direct Calculation (F/P,i,n) F = P (1+r)n Given Find F n = P = i =

Future Value Example: Find the amount which will accrue at the end of Year 6 if $1,500 is invested now at 6% compounded annually. Method #1: Direct Calculation (F/P,i,n) F = P (1+r)n Given Find F n = 6 years F = (1,500)(1+0.06)6 P = $ 1,500 F = $ 2,128 r = 6.0 %

Future Value Example: Find the amount which will accrue at the end of Year 6 if $1,500 is invested now at 6% compounded annually. Method #2: Tables The value of (1+i)n = (F/P,i,n) has been tabulated for various i and n. From the handout, use the table with interest rate of 6% to find the appropriate factor. The first step is to layout the problem as follows: F = P (F/P,i,n) F = 1500 (F/P, 6%, 6) F = 1500 ( ) =

Future Value Example: Find the amount which will accrue at the end of Year 6 if $1,500 is invested now at 6% compounded annually. Method #2: Tables The value of (1+i)n = (F/P,i,n) has been tabulated for various i and n. Obtain the F/P Factor, then calculate F: F = P (F/P,i,n) F = 1500 (F/P, 6%, 6) F = 1500 (1.4185) = $2,128

Present Value If you want to find the amount needed at present in order to accrue a certain amount in the future, we just solve Equation 1 for P and get: P = F / (1+r)n(2) Example: If you will need $25,000 to buy a new truck in 3 years, how much should you invest now at an interest rate of 10% compounded annually? (P/F,i,n) Given Find P F = n = i =

Present Value If you want to find the amount needed at present in order to accrue a certain amount in the future, we just solve Equation 1 for P and get: P = F / (1+r)n(2) Example: If you will need $25,000 to buy a new truck in 3 years, how much should you invest now at an interest rate of 10% compounded annually? Given Find P F = $25,000 P = F / (1+r)n n = 3 years P = (25,000) /(1 + 0.10)3 i = 10.0% = $18,783

Present Value If you want to find the amount needed at present in order to accrue a certain amount in the future, we just solve Equation 1 for P and get: P = F / (1+r)n(2) Example: If you will need $25,000 to buy a new truck in 3 years, how much should you invest now at an interest rate of 10% compounded annually? What is the factor to be used? ____________ Solve:

Present Value If you want to find the amount needed at present in order to accrue a certain amount in the future, we just solve Equation 1 for P and get: P = F / (1+r)n(2) Example: If you will need $25,000 to buy a new truck in 3 years, how much should you invest now at an interest rate of 10% compounded annually? What is the factor to be used? 0.7513 P = F(P/F,i,n) = (25,000)(0.7513) = $ 18,782

Present Value Example: If you will need $25,000 to buy a new truck in 3 years, how much should you invest now at an interest rate of 9.5%compounded annually? Method #1: Direct Calculation: Straight forward -Plug and Crank Method #2: Tables: Interpolation Which table in the appendix will be used? Tables i = 9% & 10% What is the factor to be used? A13 (9%): 0.7722 A14 (10%): 0.7513 Assume 9.5%: 0.7618 P = F(P/F,i,n) = (25,000)(0.7618) = $ 19,044

Engineering EconomicsEIT ReviewUniform Series & Effective Interest

F A1 A2 A3 A4 A6 A5 Cash Flow - + Time P Annuities • Uniform series are known as the equal annual payments made to an interest bearing account for a specified number of periods to obtain a future amount.

Annuities Formula • The future value (F) of a series of payments (A) made during (n) periods to an account that yields (i) interest: F = A [ (1+i)n – 1 ] (5) i Where F = Future sum of money n = number of interest periods A = Series of n equal payments made at the end of each period i = Effective interest rate per period • Derivation of this formula can be found in most engineering economics texts & study guides Notation: (F/A,i,n) or if using tables F = A (F/A,i,n)

Example: What is the future value of a series payments of $10,000 each, for 5 years, if deposited into a savings account yielding 6% nominal interest compounded yearly? Draw the cash flow diagram. F = A [ (1+i)n – 1 ] = i Check with Factor Values: F = A (F/A,i,n)

Example: What is the future value of a series payments of $10,000 each, for 5 years, if deposited in a savings account yielding 6% nominal interest compounded yearly? Draw the cash flow diagram. F = A [ (1+i)n – 1 ] = 10,000 [ (1+0.06)5 – 1 ] = 10,000 [ 1.3382 – 1 ] i 0.06 0.06 = $ 56,370 Checking with Factor Values: F = A (F/A,i,n) = 10,000 (F/A, 6%, 5) = 10,000 ( 5.6371 ) = $ 56,370

Sinking Fund • We can also get the corresponding value of an annuity (A) during (n) periods to an account that yields (i) interest to be able to get the future value (F) : Solving for A: A = i F / [ (1+i)n – 1 ](6) Notation:A = F (A/F,i,n) Example: How much money would you have to save annually in order to buy a car in 4 years which has a projected value of $18,000? The savings account offers 4.0% yearly interest.

Sinking Fund Example: How much money do we have to save annually to buy a car 4 years from now that has an estimated cost of $18,000? The savings account offers 4.0 % yearly interest. A = i F / [ (1+i)n – 1 ] A = (0.04 x 18,000) / [ (1.04)4 -1 ] = 720 / 0.170 = $4,239 A = F (A/F,i,n) A = (18,000)(A/F,4.0,4) = (18,000)(0.2355) = $4,239

Present Worth of an Uniform Series • Sometimes it is required to estimate the present value (P) of a series of equal payments (A) during (n) periods considering an interest rate (i) From Eq. 1 and 5 P = A [ (1+i)n – 1 ] (7) i (1+i)n Notation:P = A (P/A,i,n) Example: What is the present value of a series of royalty payments of $50,000 each for 8 years if nominal interest is 8%? P =

Present Worth of an Uniform Series Example: What is the present value of a series of royalty payments of $50,000 each for 8 years if nominal interest is 8%? P = A [ (1+i)n – 1 ] = 50,000 [ (1+0.08)8 – 1 ] = 50,000 [ 1.8509 – 1 ] i (1+i)n 0.08 (1.08)8 0.1481 = $ 287,300 P = A (P/A,i,n) = (50,000)(P/A,8,8) = (50,000)(5.7466) = $ 287,300

Uniform Series Capital Recovery • This is the corresponding scenario where it is required to estimate the value of a series of equal payments (A) that will be received in the future during (n) periods considering an interest rate (i) and are equivalent to the present value of an investment (P) Solving Eq. 7 for A A = i P (1+i)n(8) (1+i)n -1 Notation:A = P (A/P,i,n) Example: If an investment opportunity is offered today for $5 Million, how much must it yield at the end of every year for 10 years to justify the investment if we want to get a 12% interest? A =

Uniform Series Capital Recovery Example: If an investment opportunity is offered today for $5 Million, how much must it yield at the end of every year for 10 years to justify the investment if we want to get a 12% interest? A = i P (1+i)n= 0.12 x 5 (1+0.12)10 = 0.6 [ 3.1058 ] (1+i)n -1 (1.12)10 - 1 2.1058 = 0.8849 Million $ 884,900 per year

Engineering EconomicsEIT ReviewVarying Compounding PeriodsEffective Interest

Solving Interest Problems Example: An investment opportunity is available which will yield $1000 per year for the next three years and $600 per year for the following two years. If the interest is 12% and the investment has no terminal salvage value, what is the present value of the investment? What is Step #1?

Solving Interest Problems Example: An investment opportunity is available which will yield $1000 per year for the next three years and $600 per year for the following two years. If the interest is 12% and the investment has no terminal salvage value, what is the present value of the investment? Step #1 What are we trying to solve? P What are the known variables?A, i, n

Solving Interest Problems Step #2: Draw a Cash Flow Diagram PV (?) Receipts A1 A2 A3 A4 A5 Time A1 + A2 + A3 = $1000 A4 + A5 = $600

Solving Interest Problems Step #2: Draw a Cash Flow Diagram – Method #1 P = A1 (P/A1, i, n1) + A2 (P/A2, i, n2) = ($600)(P/A1, 12, 5) + ($400)(P/A2, 12, 3) = $3,124 A1 A2 A3 A4 A5 A1 A2 A3 + Time Time A1 = A2 = A3 = A4 = A5 = $600 A1 = A2 = A3 = $400

Solving Interest Problems Step #2: Draw a Cash Flow Diagram – Method #2 P = A1 (P/A1, i, n1) + A2 (P/A2, i, n2)(P/F, i, n3) = ($1000)(P/A1, 12, 3) + ($600)(P/A2, 12, 2)(P/F, 12, 3) = $3,124 A1 A2 A3 P A4 A5 + Time Time A1 = A2 = A3 = $1000 A4 = A5 = $600

Varying Payment and Compounding Intervals • Thus far, problems involving time value of money have assumed annual payments and interest compounding periods • In most financial transactions and investments, interest compounding and/or revenue/costs occur at frequencies other than once a year (annually) • An infinite spectrum of possibilities • Sometimes called discrete, periodic compounding • In reality, the economics of project feasibility are simply complex annuity problems with multiple receipts & disbursements

Compounding Frequency • Compounding can be performed at any interval (common: quarterly, monthly, daily) • When this occurs, there is a difference between nominal and effective annual interest rates • This is determined by: i = (1 + r/x)x – 1 where: i = effective annual interest rate r = nominal annual interest rate x = number of compounding periods per year

Compounding Frequency Example: If a student borrows $1,000 from a finance company which charges interest at a compound rate of 2% per month: • What is the nominal interest rate: r = (2%/month) x (12 months) = 24% annually • What is the effective annual interest rate: i = (1 + r/x)x – 1 i = (1 + .24/12)12 – 1 = 0.268 (26.8%)

Nominal and EffectiveAnnual Rates of Interest • The effective interest rate is the rate compounded once a year which is equivalent to the nominal interest rate compounded x times a year • The effective interest rate is always greater than or equal to the nominal interest rate • The greater the frequency of compounding the greater the difference between effective and nominal rates. But it has a limit Continuous Compounding. Frequency Periods/year Nominal Rate Effective Rate Annual 1 12% 12.00% Semiannual 2 12% 12.36% Quarterly 4 12% 12.55% Monthly 12 12% 12.68% Weekly 52 12% 12.73% Daily 365 12% 12.75% Continuously ∞ 12% 12.75%

Compounding Frequency • It is also important to be able to calculate the effective interest rate (i) for the actual interest periods to be used. • The effective interest rate can be obtained by dividing the nominal interest rate by the number of interest payments per year (m) i = (r/m) where: i = effective interest rate for the period r = nominal annual interest rate

When Interest Periods Coincide with Payment Periods • When this occurs, it is possible to directly use the equations and tables from previous discussions (annual compounding) Provided that: (1) the interest rate (i) is the effective rate for the period (2) the number of years (n) must be replaced by the total number of interest periods (mn), where m equals the number of interest periods per year

When Interest Periods Coincide with Payment Periods Example: An engineer plans to borrow $3,000 from his company credit union, to be repaid in 24 equal monthly installments. The credit union charges interest at the rate of 1% per month on the unpaid balance. How much money must the engineer repay each month? A = P (A/P, i, mn) = i P (1+i)n (1+i)n -1 A = ($3000) (A/P, 1%, 24) = $141.20

When Interest Periods Coincide with Payment Periods Example: An engineer wishes to purchase an $80,000 lakeside lot (real estate) by making a down payment of $20,000 and borrowing the remaining $60,000, which he will repay on a monthly basis over the next 30 years. If the bank charges interest at the rate of 9½% per year, compounded monthly, how much money must the engineer repay each month? i = (r/m) = (0.095/12) = 0.00792 (0.79%) A = P (A/P, i, mn) = i P (1+i)n (1+i)n -1 A = ($60000) (A/P, 0.79%, 360) = $504.50 Total amount repaid to the bank?

When Interest Periods are Smaller than Payment Periods • When this occurs, the interest may be compounded several times between payments. • One widely used approach to this type of problem is to determine the effective interest rate for the given interest period, and then treat each payment separately.

When Interest Periods are Smaller than Payment Periods • Example: Approach #1 An engineer deposits $1,000 in a savings account at the end of each year. If the bank pays interest at the rate of 6% per year, compounded quarterly, how much money will have accumulated in the account after 5 years? Effective Interest Rate: i = (6%/4) = 1.5% per quarter F = P (F/P,i,mn) F = $1000(F/P,1.5%,16) + $1000(F/P,1.5%,12) + $1000(F/P,1.5%,8) +$1000(F/P,1.5%,4) +$1000(F/P,1.5%,0) Using formulas or tables: F = $5,652

When Interest Periods are Smaller than Payment Periods • Another approach, often more convenient, is to calculate an effective interest rate for the given payment period, and then proceed as though the interest periods and the payment periods coincide. i = (1 + r/x)x – 1

When Interest Periods are Smaller than Payment Periods • Example: Approach #2 An engineer deposits $1,000 in a savings account at the end of each year. If the bank pays interest at the rate of 6% per year, compounded quarterly, how much money will have accumulated in the account after 5 years? i = (1 + r/x)x – 1 = (1 + 0.06/4)4 – 1 = 0.06136 (6.136%) F = $1,000 (F/A,6.136%,5) Using formula: F = $5,652

When Interest Periods are Larger than Payment Periods • When this occurs, some payments may not have been deposited for an entire interest period. Such payments do not earn any interest during that period. • Interest is only earned by those payments that have been deposited or invested for the entire interest period. • Situations of this type can be treated in the following manner: • Consider all deposits that were made during the interest period to have been made at the end of the interest period (i.e., no interest earned during the period) • Consider all withdrawals that were made during the interest period to have been made at the beginning of the interest period (i.e., earning no interest) • Then proceed as though the interest periods and the payment periods coincide.

When Interest Periods are Larger than Payment Periods Example: A person has $4,000 in a savings account at the beginning of a calendar year; the bank pays interest at 6% per year, compounded quarterly. Given the transactions presented in the following table (next slide), find the account balance at the end of the calendar year. Effective Interest Rate (i) = 6%/4 = 1.5% per quarter