Download

1 / 25

250 likes | 549 Views

Risk and Rates of Return. Besley: Chapter 5 Pages 179-198. Risk and Investing. The Rules: Investing is risky. Risk is manageable. Types of Risk: Diversifiable Risk – Can be eliminated through diversification. Nondiversifiable Risk. Defining and Measuring Risk.

E N D

Risk and Rates of Return Besley: Chapter 5 Pages 179-198

Risk and Investing The Rules: • Investing is risky. • Risk is manageable. Types of Risk: • Diversifiable Risk– Can be eliminated through diversification. • Nondiversifiable Risk

Defining and Measuring Risk • Risk is the chance that an outcome other than the expected outcome will occur. • A Probability Distribution lists allpossible outcomes and the probability of each outcome. The probabilities must sum to 1.0 (100%)

Defining and Measuring Risk Stand-Alone Riskis that risk which is associated with an investment that which is held on its own. Portfolio Riskis that risk which is associated with an investment that which is maintained in a portfolio of investments.

Flip a Coin: Outcome Probability Heads 50% Tails 50% 100% Chance of Snow: Outcome Probability Snow 50% Rain 30% No Snow 20% /Rain 100% Probability Distributions Probability Distribution: a listing of all possible outcomes with the likelihood of each possibility indicated.

Probability Distributions Martin Products and U. S. Electric

Expected Rate of Return • The rate of return expected to be realized from an investment • The mean value of the probability distribution of possible returns • The weighted average of the outcomes, where the weights are the probabilities

Martin Products U. S. Electric Probability of This State Return if This State Return if This State of the Product: Product: State Occurs (ki) Economy Occurring ( Pr ) Occurs (ki) (2) x (3) (2) x (5) i (1) (2) (3) = (4) (5) = (6) Boom 0.2 110% 22% 20% 4% Normal 0.5 22% 11% 16% 8% Recession 0.3 -60% -18% 10% 3% ^ ^ = = 1.0 k 15% k 15% m US Expected Rate of Return

Continuous versus Discrete Probability Distributions Discrete Probability Distribution:the number of possible outcomes is limited, or finite

a. Martin Products b. U. S. Electric Probability of Occurrence Probability of Occurrence 0.5 - 0.4 - 0.3 - 0.2 - 0.1 - 0.5 - 0.4 - 0.3 - 0.2 - 0.1 - Rate of Return (%) -60 -45 -30 -15 0 15 22 30 45 60 75 90 110 -10 -5 0 5 10 16 20 25 Rate of Return (%) Expected Rate of Return (15%) Expected Rate of Return (15%) Discrete Probability Distributions

Continuous versus Discrete Probability Distributions • Continuous Probability Distribution:the number of possible outcomes is unlimited, or infinite

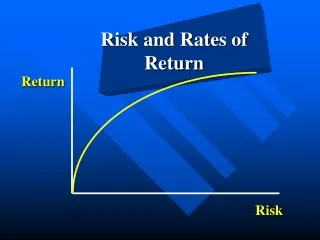

Continuous Probability Distributions Probability Density A tighter probability distribution is representative of lower risk. Martin Products -60 0 15 110 Rate of Return (%) Expected Rate of Return

^ ^ ^ ^ Measuring Risk: The Standard Deviation Calculating Martin Products’ Standard Deviation

Measuring Risk: The Standard Deviation s provides a definite value that represents the “tightness” of the probability distribution. A lower standard deviation indicates a tighter probability distribution, and the less risk associated with that particular stock.

s Risk = = = Coefficient of variation CV Return ˆ k Measuring Risk: Coefficient of Variation • Standardized measure of risk per unit of return • Calculated as the standard deviation divided by the expected return • Useful where investments differ in risk and expected returns

Risk Aversion • Risk-averse investors require higher rates of return to invest in higher-risk securities

Risk Aversion and Required Returns Risk Premium (RP) • The portion of the expected return that can be attributed to the additional risk of an investment • The difference between the expected rate of return on a given risky asset and that on a less risky asset

W1 is that stocks portion of the portfolio’s dollar value; therefore the sum of the W’s must equal 1. Portfolio Returns ^ • Expected return on a portfolio, kp The weighted average expected return on the stocks held in the portfolio

Portfolio Risk & Returns • Unlike returns, portfolio risk is not a weighted average of the standard deviations of the individual stocks (the portfolio’s risk is usually smaller). • Realized rate of return, k is the actual return earned, and usually differs from the expected return. _

Returns Distribution for Two Perfectly Negatively Correlated Stocks (r = -1.0) and for Portfolio WM: Stock W Stock M Portfolio WM 25 25 25 15 15 15 0 0 0 -10 -10 -10

Returns Distributions for Two Perfectly Positively Correlated Stocks (r = +1.0) and for Portfolio MM: Stock M Stock MM’ Stock M’ 25 25 25 15 15 15 0 0 0 -10 -10 -10

Portfolio Risk • Correlation Coefficient, r • A measure of the degree of relationship between two variables • Perfectly correlated stocks rates of return move together in the same direction (+1.0) • Negatively correlated stocks have rates of return that move in opposite directions (-1.0) • Uncorrelated stocks have rates of return which move independently on one another (0.0)

Portfolio Risk • Risk Reduction • Combining stocks that are not perfectly correlated will reduce the portfolio risk by diversification • The riskiness of a portfolio is reduced as the number of stocks in the portfolio increases • The smaller the positive correlation, the lower the risk