Download

1 / 16

160 likes | 353 Views

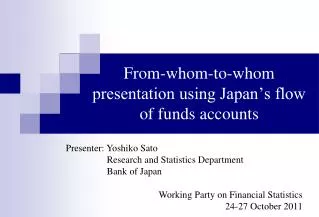

Measuring Securitization in the Flow of Funds Accounts in Japan. Yoshiko Sato Financial Statistics Section Research and Statistics Department Bank of Japan. Working Party on Financial Statistics, OECD Paris, 2-4 November 2009. 1 /16. Motivation.

E N D

Measuring Securitization in the Flow of Funds Accounts in Japan Yoshiko SatoFinancial Statistics SectionResearch and Statistics DepartmentBank of Japan Working Party on Financial Statistics, OECD Paris, 2-4 November 2009 1/16

Motivation • Recent financial turmoil has led an increasing number of people to look into Flow of Funds Accounts (FFA) statistics. • The statistics is primarily designed to describe a country’s financial structure in rather a long-term perspective. But recent financial events set it to another task of providing information to narrow “data gaps” or to capture “shadow banking system” (as highlighted in G20). • In this sense, the paper intends to assess to what extent FFA captures the securitization under the current statistical treatment.– How do we compile securitization figures?– What is the coverage of securitization?– What can we learn from the FFA data?– What should we do to improve the statistics? 2/16

Outline • Definition of the sector and instruments. • Compilation method (Sources/Scope/Valuation/ Holding sector) • Treatment of securitization through JHFA 1. Statistical treatment 2. Assessment of coverage 3. What can we learn from FFA data? 4. Possible future approach 5. Conclusion 3/16

“SPC and Trust” sector A sub-sector of non-banks in other financial institution 80.8% 1.Statistical treatment – sector, instruments • What sector captures securitization activity? • How does the sector work? It issues ABS, ABCP, and MCT backed by loans, installment credit (i.e. lease), bonds, and trade credits. 4/16

MCT Trust MCT MCT Typical Securitization Scheme in Japan 1.Statistical treatment – compilation method Loan sales (not securitization) Originator Investors Case 1 (Banks) (Banks) Trust Trust Originator Trust Investors Case 2 Monetary claim trust (MCT) SPC and Trust ABS Case 3 Originator Trust SPC Investors 5/16

4 major trust banks 11 trust subsidiaries 5 trust companies MCT Direct reporting from 20 institutions ABS Publicly available data aggregate data from JSDA (Japan Security Dealers Association) classified by each type of underlying asset. ABCP Estimation is conducted by assuming that it is proportionate to MCT. Private or public issues ABS includes privately placed issues but since there is no primary data we conduct estimation. Residency Domestic bonds issued by non-resident SPC are within the scope of “SPC and Trust” sector but available data are limited to the publicly placed issues. Book value basis 1.Statistical treatment – compilation method • Sources • Scope of the “SPC and Trust” sector • Valuation 6/16

1.Statistical treatment – compilation method • Information of holding sector Most difficult part to know. • Treatment of securitization through JHFA Holding amounts of banks, insurance companies, finance companies, and social security funds are based on the financial statement. Those of non-residents are estimated. The residual with no specific holding entity goes to private non-financial institutions. JHFA (Japan Housing Finance Agency) is the largest issuer of MBS. The outstanding amount of MBS reaches 8.9 trillion yen. JHFA’ securitization is “On-balance sheet” securitization. So it is excluded from the SPC and Trust sector but included in the “Government financial institution” sector. 7/16

2. Assessment of coverage • FFA has a good coverage in that All major financial institutions are contributing to reporting MCT which are quite often used in Japan’s securitization. Private placement and non-resident SPC are partly covered. • However, the coverage is incomplete in that Primary data source of private placement of ABS/MBS is almost absent. Non-resident SPC’s private placement is inseparable from the primary data source of BP and IIP statistics. 8/16

3. What can we learn from FFA data?(1) Turning point Total assets of the SPC and Trusts sector • There is outstanding of 30 trillion yen in Structured-financing instruments. • The volume has been expanding during the first half of 2000s. • The data correctly traces the turning point of the sector in mid 2007. 9/16

3. What can we learn from FFA data?(1) Turning point Proportion of Underlying Assets • “Housing loans”includesJHFA’s MBS. • “Housing loans” excludesJHFA’s MBS. 10/16

Loans to companies and governments Housing loans Trade credits and foreign trade credits Installment credit (i.e. lease) 3. What can we learn from FFA data?(1) Turning point SPC and Trust sector classified by type of underlying assets 11/16

Direct investment Portfolio investment in securities 3. What can we learn from FFA data?(2) Cross-border securitization Balance of Payment Statistics • Both increase toward the 4Q 2008 and decrease shortly after then. • If we assume that a part of such increase should attribute to any private placements of non-residents SPC, the figure would have behaved differently; it might have continued to increase until the end 2008. 12/16

Securitization Borderline Borderline Sells assets Tokyo branch of the non-resident SPC Domestic Investors Issues MBS Buy MBS Portfolio investment in securities (outward) Banks’ Recapitalization Subordinated loans Direct investment or portfolio investment in securities (outward) Preferred stocks 3. What can we learn from FFA data?(2) Cross-border securitization Types of SPC related transaction Non-resident SPC Originator • Expected transactions to be captured • Transactions really happened Non-resident SPC Banks Domestic Investors 13/16

3. What can we learn from FFA data?(3) Holding sector of “Structured-financial instruments” (trillion yen) Sources: Bank of Japan, “Flow of Funds Accounts” 14/16

4. Possible Future Approach • Use of electronically registered data for statistical purpose instead of using survey data Using existing data source is efficient without additional reporting burden if the data is permitted to use for social statistical purpose. Electronically registered book-entry transfer system (i.e. JASDEC) has already been in operation. Such database is expected to contain security-by-security information. Co-operation between the related bodies (industry association, depository center, other statistical authorities) should be prerequisite. • International co-operation in data collection Statistics may not improve solely by compilers’ domestic efforts. International co-operation in data collection is helpful for identifying cross-border secutitization. 15/16

5. Conclusion • FFA serves to capture securitization activity. It correctly traces the turning point in mid 2007. • Enriching primary data source is needed. Data gap is a problem where no primary data exists. Usefulness of FFA can be more enhanced by precise primary data. - End of presentation - 16/16