Download

1 / 15

150 likes | 461 Views

INSURANCE AGENT. Usual link between the consumer and the insurance company for personal lines.Commercial insurance often involves brokers.The agency relationship is controlled by agency law. 2. . . LAW OF AGENCY (Common Law). An agent is a person authorized to act on behalf of another person who is the principalDuties of the agent:LoyaltyNot to be negligentTo obey instructionsDuties of the principal:Pay the agent for services renderedMeet other contractual obligations (training, expense1145

E N D

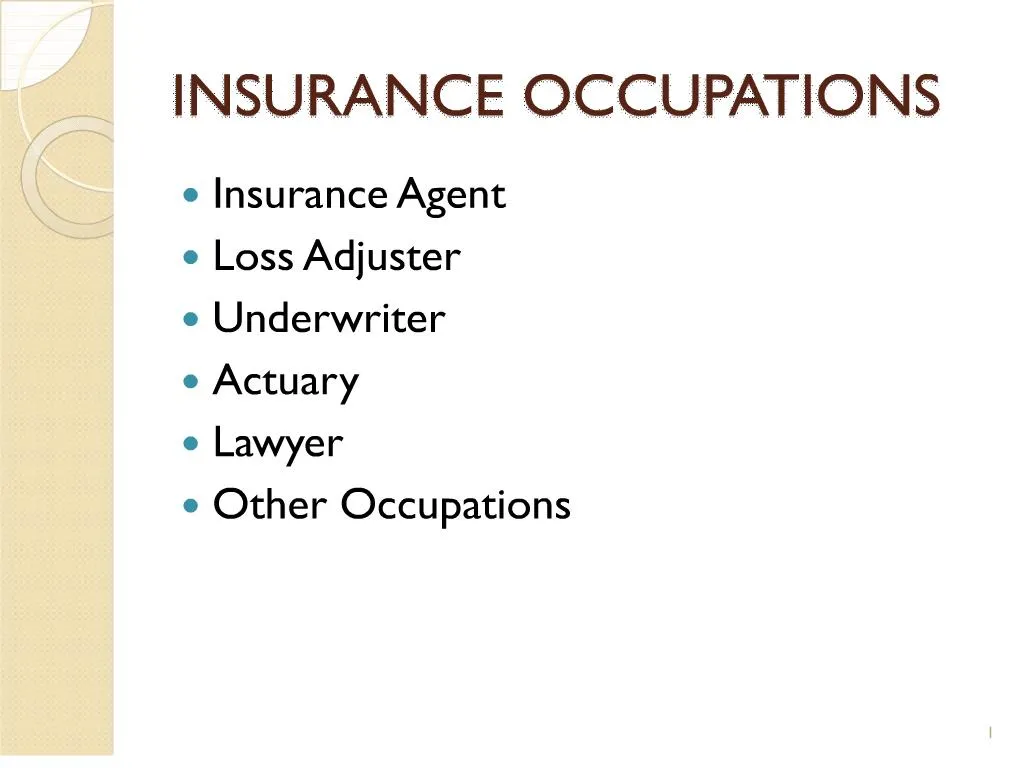

1. INSURANCE OCCUPATIONS Insurance Agent

Loss Adjuster

Underwriter

Actuary

Lawyer

Other Occupations 1 The main occupations that are considered necessary to operate an insurance organization are discussed in turn in this chapter. There will be an extended discussion of the sales agent because the student needs to understand the principal agent relationship. This relationship extends beyond just the sales agent but extends to the loss adjuster too.The main occupations that are considered necessary to operate an insurance organization are discussed in turn in this chapter. There will be an extended discussion of the sales agent because the student needs to understand the principal agent relationship. This relationship extends beyond just the sales agent but extends to the loss adjuster too.

2. INSURANCE AGENT Usual link between the consumer and the insurance company for personal lines.

Commercial insurance often involves brokers.

The agency relationship is controlled by agency law 2 When any insurance is sold, some form of sales agent is involved since corporations cannot literally do anything without people being involved. So insurance agents are the usual link between the company and the policy owner that facilitates the creating of an insurance contract.

The agency relationship is controlled by agency law by default. However, most agents have signed a contract called an agency agreement which spells out the rights and duties of all parties to the contract. And therefore, the contractual relationship would control the relationship between the agent and company.

Ethical issues

the need to survive in a very competitive market;

company practices (heavy front-end loads, and replacement)

the legal and financial complexity of life insurance contacts (and misleading illustrations)

When any insurance is sold, some form of sales agent is involved since corporations cannot literally do anything without people being involved. So insurance agents are the usual link between the company and the policy owner that facilitates the creating of an insurance contract.

The agency relationship is controlled by agency law by default. However, most agents have signed a contract called an agency agreement which spells out the rights and duties of all parties to the contract. And therefore, the contractual relationship would control the relationship between the agent and company.

Ethical issues

the need to survive in a very competitive market;

company practices (heavy front-end loads, and replacement)

the legal and financial complexity of life insurance contacts (and misleading illustrations)

3. LAW OF AGENCY (Common Law) An agent is a person authorized to act on behalf of another person who is the principal

Duties of the agent:

Loyalty

Not to be negligent

To obey instructions

Duties of the principal:

Pay the agent for services rendered

Meet other contractual obligations (training, expense reimbursement, etc.) 3 The students should have a fundamental understanding of the legal aspects of the law of agency and understand that the sales agent, claims adjuster or any person authorized to act on behalf of another person is considered an agent. And with this relationship duties and responsibilities are imposed by law.The students should have a fundamental understanding of the legal aspects of the law of agency and understand that the sales agent, claims adjuster or any person authorized to act on behalf of another person is considered an agent. And with this relationship duties and responsibilities are imposed by law.

4. Agent�s Authority Agents receive authority from principals in several ways

Agency agreement (contract)

Ratification � through a series of unauthorized and accepted repeated acts

Apparent authority � principal leads the public to believe the agency relationship exists

Scope of authority is established in the agency agreement - contract between agent and the insurance company

Agency agreement spells out extent of authority as well as all the contract specifics 4 The agency agreement is the main way that agents receive their authority to transact business for an insurance company beyond being qualified by the state (passed the state exams) and licensed by the company.

Ratification is where there is a series of repeated activities that the principal does not object to. By not objecting, they have effectively ratified the relationship.

Apparent authority is where the principal leads the public to believe that the person has the authority. This is where the principal should have done something or failed to do something to allow the belief to occur.

The agency agreement is the main way that agents receive their authority to transact business for an insurance company beyond being qualified by the state (passed the state exams) and licensed by the company.

Ratification is where there is a series of repeated activities that the principal does not object to. By not objecting, they have effectively ratified the relationship.

Apparent authority is where the principal leads the public to believe that the person has the authority. This is where the principal should have done something or failed to do something to allow the belief to occur.

5. Types of Insurance Agents In Property and Liability

When limited to soliciting business - called a "special" or "soliciting" agent

When agent able to bind principal then called a "general agent"

In Life Insurance

Insurance agents are soliciting agents because they do not have the power to bind

General agents (branch managers) are hired to develop a geographic territory 5 Insurance agents differ in the life insurance and the property and casualty side of the business.

In property and liability insurance:

The insurance agent that can bind coverage is called a �general agent� � the power is usually provided to the agent through the agency agreement.

Special or soliciting agents are not allowed to bind because they have not passed the requisite state exams and do not have the authority as provided by the insurance company.

In the life insurance industry:

Agents selling coverage are technically soliciting agents because they do not have the power to bind. Insurance companies want to control very closely who it insures because there is little opportunity to destroy the contract once it is started. There is no cancellation clause in the life insurance contract.Insurance agents differ in the life insurance and the property and casualty side of the business.

In property and liability insurance:

The insurance agent that can bind coverage is called a �general agent� � the power is usually provided to the agent through the agency agreement.

Special or soliciting agents are not allowed to bind because they have not passed the requisite state exams and do not have the authority as provided by the insurance company.

In the life insurance industry:

Agents selling coverage are technically soliciting agents because they do not have the power to bind. Insurance companies want to control very closely who it insures because there is little opportunity to destroy the contract once it is started. There is no cancellation clause in the life insurance contract.

6. Insurance Brokers Brokers also market insurance in both life and health and property and liability insurance

Brokers do not have the power to bind

Broker is agent of the consumer - not the company 6 Reasons for brokerage (commercial insurance, hard to place life insurance cases).

Analogy to investment banker. (Insurance market changes regularly, underwriting cycle.)

Brokers are used in commercial insurance generally to seek insurance carriers and have them bid on the insurance. For example General Motors could write their own insurance contract (manuscript contract) and have a broker solicit bids for the insurance. The broker would then analyze the bids and make a recommendation as to whom should be the insurer.Reasons for brokerage (commercial insurance, hard to place life insurance cases).

Analogy to investment banker. (Insurance market changes regularly, underwriting cycle.)

Brokers are used in commercial insurance generally to seek insurance carriers and have them bid on the insurance. For example General Motors could write their own insurance contract (manuscript contract) and have a broker solicit bids for the insurance. The broker would then analyze the bids and make a recommendation as to whom should be the insurer.

7. Comparison of Agents and Brokers AGENCY RELATIONSHIP

consumer agent company

BROKERAGE RELATIONSHIP

consumer broker company

Questions: Who does the agent work for? What was the agent doing at the time of the incident?

7 The principal agent relationship exists both in the agency relationship and the brokerage relationship. However, the relationship is between different parties. In the agency relationship, there is a connection between the company and the agent and any knowledge told the agent is automatic knowledge of the company.

In the brokerage relationship, the connection is between the consumer and the broker. And any knowledge provided the broker is not automatic knowledge of the company.

Who does the agent work for? It depends. While generic recommendations are being made, the agent works for the client. When the agent places the coverage, the agent is working for the company. The general agent could have placed the business with a different insurance company.The principal agent relationship exists both in the agency relationship and the brokerage relationship. However, the relationship is between different parties. In the agency relationship, there is a connection between the company and the agent and any knowledge told the agent is automatic knowledge of the company.

In the brokerage relationship, the connection is between the consumer and the broker. And any knowledge provided the broker is not automatic knowledge of the company.

Who does the agent work for? It depends. While generic recommendations are being made, the agent works for the client. When the agent places the coverage, the agent is working for the company. The general agent could have placed the business with a different insurance company.

8. DISTRIBUTION OF INSURANCEProperty and Liability 8 Sales relationships range from the direct writer to the independent agent.

Companies are experimenting with many formulas of agent independence versus levels of control and cost or service arrangements.

Direct writers and independent agents are on the opposite side of the continuum of how insurance can be distributed in the property and liability area.

Sales relationships range from the direct writer to the independent agent.

Companies are experimenting with many formulas of agent independence versus levels of control and cost or service arrangements.

Direct writers and independent agents are on the opposite side of the continuum of how insurance can be distributed in the property and liability area.

9. DISTRIBUTION OF INSURANCE Life Insurance Branch manager has control of territory and recruits and trains soliciting or special agents

Life insurance agents can never bind coverage - authority limited power to bind remains at the home office 9 This slide illustrates the distribution system in the life and health insurance industry.

Life insurance traditionally has been distributed by geographic territory. The company assigns a branch manager or general agent to a geographic territory and is responsible for hiring, training, and getting soliciting agents licensed to sell or solicit life insurance.This slide illustrates the distribution system in the life and health insurance industry.

Life insurance traditionally has been distributed by geographic territory. The company assigns a branch manager or general agent to a geographic territory and is responsible for hiring, training, and getting soliciting agents licensed to sell or solicit life insurance.

10. LOSS ADJUSTERSor Claims Investigator Loss adjusters make the product perform - pays the claim

Steps in adjusting a claim

Investigate

Determine if policy covers

Determine amount of the loss

Pay the claim

Independent Adjusters vs. Company Adjusters vs. Public Adjusters 10 Loss adjusters are extremely important to the insurance transaction because they can make or destroy the reputation of the insurance company (industry) so it is said that loss adjusters make the product perform.

Loss adjusters must go through a logical process in determining if a claim should be paid or denied. And these are the general steps shown in the loss adjustment process.

Many reasons why an insurer will not pay a claim:

Wrong company, expired policy, exclusion, fraud, wrong policy, no insurable interest, no peril covered, under deductible amounts

Amount of loss can be a question and further discovery may be needed to determine this amount

No premium payment

There are various types of loss adjusters.

Company adjusters are paid to adjust claims as employees of the company.

Independent adjusters are part of a business to adjust claims and are paid on a fee for service basis.

Public adjusters are generally independent adjusters but they are hired by the insured to bolster their side of the claims process. Public adjusters need to be careful about conflicts of interest issues. Being a public adjuster for an insured while on other cases representing the company as an independent adjuster.

Loss adjusters are extremely important to the insurance transaction because they can make or destroy the reputation of the insurance company (industry) so it is said that loss adjusters make the product perform.

Loss adjusters must go through a logical process in determining if a claim should be paid or denied. And these are the general steps shown in the loss adjustment process.

Many reasons why an insurer will not pay a claim:

Wrong company, expired policy, exclusion, fraud, wrong policy, no insurable interest, no peril covered, under deductible amounts

Amount of loss can be a question and further discovery may be needed to determine this amount

No premium payment

There are various types of loss adjusters.

Company adjusters are paid to adjust claims as employees of the company.

Independent adjusters are part of a business to adjust claims and are paid on a fee for service basis.

Public adjusters are generally independent adjusters but they are hired by the insured to bolster their side of the claims process. Public adjusters need to be careful about conflicts of interest issues. Being a public adjuster for an insured while on other cases representing the company as an independent adjuster.

11. LOSS ADJUSTERS QUESTION: Why do insurance agents and loss adjusters have to be very careful about what they tell the insured when they process a loss or adjust a claim?

Waiver - voluntary relinquishment of a known right.

Estoppel - legal order to create consistent behavior. 11 Most people think that loss adjusters are insensitive to the client�s needs. However, adjusters and agents have to be extremely careful about what they do and say since they could be committing the company to paying losses when the contract does not call for it.

The mechanism of this is through waiver and estoppel.

If the insurer (through the agent or adjuster) waives a right (for example tells the insured that the claim will be paid) and then changes its mind, the court can estopp the insurer from denying liability to create consistent behavior.Most people think that loss adjusters are insensitive to the client�s needs. However, adjusters and agents have to be extremely careful about what they do and say since they could be committing the company to paying losses when the contract does not call for it.

The mechanism of this is through waiver and estoppel.

If the insurer (through the agent or adjuster) waives a right (for example tells the insured that the claim will be paid) and then changes its mind, the court can estopp the insurer from denying liability to create consistent behavior.

12. UNDERWRITER Job is to accept exposures at appropriate rate

Reject application if underwriting rules do not allow acceptance (too few exposures or lack of data to determine credibility of the class)

Must be a skillful judge of people

Goal is to produce a group of insureds by categories whose actual experience will approximate or approach expected.

Goal is not to reject people going to have losses. 12 The term �underwriter� came from signing at the bottom on a Lloyds� (coffee house) slip indicating a commitment to accept part of the coverage desired.

Underwriters strive to minimize adverse selection

It is an art - not a science for commercial or other uncommon exposures.

Their job is to evaluate, select, classify, and rate.

There may be a conflict between privacy issues and a fair insurance premium.

Some people believe it is the job of the underwriter to identify people that are going to have losses and reject them. Some people believe that this can actually be done. However, the job of the underwriter is to correctly classify the exposure to generate a large number of similar exposures in the pool all paying a fair price.

The term �underwriter� came from signing at the bottom on a Lloyds� (coffee house) slip indicating a commitment to accept part of the coverage desired.

Underwriters strive to minimize adverse selection

It is an art - not a science for commercial or other uncommon exposures.

Their job is to evaluate, select, classify, and rate.

There may be a conflict between privacy issues and a fair insurance premium.

Some people believe it is the job of the underwriter to identify people that are going to have losses and reject them. Some people believe that this can actually be done. However, the job of the underwriter is to correctly classify the exposure to generate a large number of similar exposures in the pool all paying a fair price.

13. ACTUARY Develops statistics and classifications for insurance rates

Reviews past and projected future results

Involved in product development

Regulatory compliance issues

Calculation of participating dividends 13 The actuary is a mathematically minded person who is involved in several activities that are required by the insurer. These activities go beyond merely developing rates and classifications schemes.

The actuary is a mathematically minded person who is involved in several activities that are required by the insurer. These activities go beyond merely developing rates and classifications schemes.

14. LAWYER Lawsuits

Wording of insurance contracts

Deal with regulatory agencies

General advice and counsel 14 Lawyers are employed in the insurance industry in a variety of capacities beyond providing legal advice and counsel similar to any business organization.

Insurance companies sue and subrogate against other insurers. They also are sued and sue people.

They are extensively involved in the wording of insurance contracts to make sure that there is a high probability that the insurance contract will be interpreted by the courts the way they think is should be interpreted. If not, the contracts are generally rewritten or rates are adjusted.

In addition, lawyers deal with state and federal regulatory authorities in the areas of rating, form language, marketing, licensing of companies and agents as well as dealing with financial compliance issues.

Lawyers are employed in the insurance industry in a variety of capacities beyond providing legal advice and counsel similar to any business organization.

Insurance companies sue and subrogate against other insurers. They also are sued and sue people.

They are extensively involved in the wording of insurance contracts to make sure that there is a high probability that the insurance contract will be interpreted by the courts the way they think is should be interpreted. If not, the contracts are generally rewritten or rates are adjusted.

In addition, lawyers deal with state and federal regulatory authorities in the areas of rating, form language, marketing, licensing of companies and agents as well as dealing with financial compliance issues.

15. Other Occupations Financial administrators

Accountants, Financiers, Managers, Statisticians, Economists

Architects, Engineers

Doctors, Health Care Professionals

Marketing, Advertising

Personnel Administrators, Law Enforcement

Computer System Operators and Software Authors

. . . 15 I stress that just about any person in just about any profession can be hired or employed by the insurance industry. This overhead provides a incomplete list of the types of people employed.I stress that just about any person in just about any profession can be hired or employed by the insurance industry. This overhead provides a incomplete list of the types of people employed.