Download

1 / 11

120 likes | 328 Views

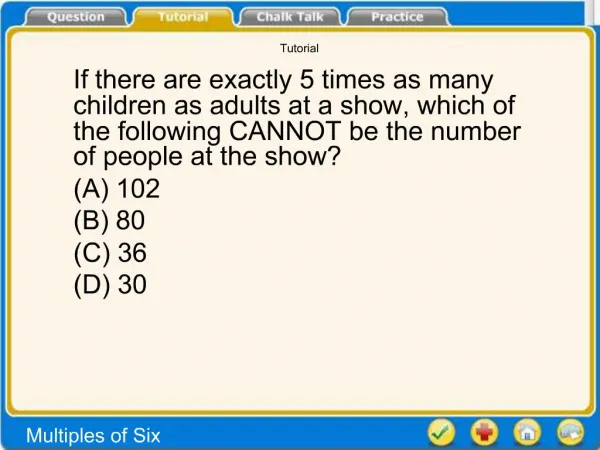

T2125 Tutorial . How to complete the T2125 form this coming tax season if you are a Sole Proprietor . Business Income. If you have business income, fill out part 1 of form 2125 In the example above Jane has gross sales of $100,000 this year.

E N D

T2125 Tutorial How to complete the T2125 form this coming tax season if you are a Sole Proprietor

Business Income • If you have business income, fill out part 1 of form 2125 • In the example above Jane has gross sales of $100,000 this year. • She also has returns and allowances of $1,000 which is deducted from • sales • Jane’s adjusted gross sales end of year is $99,000 • This amount will be carried forward to part 3

Professional Income • Check this box if you have professional income • Professional income includes Work in Process(WIP) • If you have both professional and business income complete • separate T2125 forms • Cannot check both boxes on the same return

Gross Business Income • Carry forwarded the amount from part 1 line C to be starting • amount • Jane has no reserves deducted last year or other income (recapture) • Carry line 8299 forward to cost of goods sold

Cost of Goods Sold • Start with carry forward amount from Part 3 line 8299 • Basic equation for costs of good sold is: • Beginning Inventory + Purchases – Ending inventory = COGS • If any other costs are not listed above, add them as well • Subtract COGS from the carry forward amount to get gross profit • This will be thenew carry forward amount, Line 8519

Expenses • Part 5 is where to deduct expenses for the year • Most of the expenses might be similar to the income statement amounts • For motor • vehicle and CCA expenses , separate calculations are needed. • Deduct total expenses from gross • income to get net income (loss) • before adjustments • Carry Line 9369 forward to Part 6

CCA Example 1 • Jane purchases a building for $100,000 on January 15, 2013 • Building is Class 1 and has a rate of 4% under classes of depreciable property • Since the Building was purchased this year it has 0 UCC or tax value • When purchasing a depreciable property during the current year only half its value can be deducted • Area C is for Building Additions • Area E is for Building Dispositions

CCA Example 2 • Say in that same year Jane had disposed of some equipment. The equipment had a remaining UCC (tax value) of $10,000 and was sold for $5,000. • If total CCA is negative it is considered recapture and must be added on Line 8230 as other income • Recapture occurs when selling depreciable property for more than its UCC or tax value • Since CCA is positive the $3,000 will be added to CCA expense section line 9270 • Area B is for equipment additions • Area D is for equipment dispositions

Motor Vehicle Expense • Enter business km • Enter car expenses that CRA allows deductions for • business use km • total km • x • Expenses claimed • = • Your allowable motor vehicle expense for the year • added to line 9281 in Part 5 • CCA can be claimed on your car • See Class 10.1 for further details

Net Income • Carry forward line 9369 from Part 5 to be starting point for Part 6 • If your business has any GST/HST rebates for partners received • during the year they must be added to net income under line N • If a vehicles is shared with your partner and they have not paid • you back for expenses it can be claimed. • The business home expense can be deducted in this section. • The T2125 form is now complete and net income for tax purposes has been calculated

Conclusion • If you are a sole proprietor and have active business or professional income you must complete the T2125 form. • Be Sure to speak to your accountant if you have any questions concerning the form or for other ways they might be able to save you tax