Download

1 / 28

280 likes | 408 Views

PPPs for Infrastructure: Global Opportunities & Emerging Market Potential. Elaine Glennie Senior Capacity Building Specialist Asian Development Bank Institute. Govindan Nair Lead Economist World Bank Institute. David Bloomgarden Project Specialist Multilateral Investment Fund –

E N D

PPPs for Infrastructure: Global Opportunities& Emerging Market Potential Elaine Glennie Senior Capacity Building Specialist Asian Development Bank Institute Govindan Nair Lead Economist World Bank Institute David Bloomgarden Project Specialist Multilateral Investment Fund – Inter-American Development Bank

Global TrendsPre-Financial CrisisPPI Investment by Region, US$ Million Source: World Bank PPIAF Database

Global TrendsPre-Financial CrisisPPI Investment by Sector, US$ Million Source: World Bank PPIAF Database

Annual Commitments to Infrastructure Projects in Sub-Saharan Africa by Emerging Market Financiers, 2001-2007 Flows from Emerging Economies to Africa Grew Significantly • In 2006, emerging financiers – including China, India and Arab states – committed more than $8 billion to infrastructure in Africa. • Chinese investment in Africa was at least $7 billion in 2006 and estimated $4.5 billion in 2007. • In June 2006, Premier Wen Jiabao said China has offered more than $44 billion over past 50 years to finance 900 infrastructure projects.

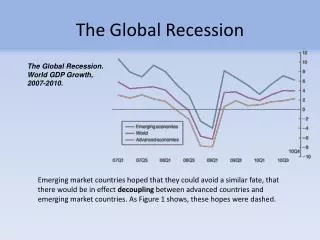

Global Economic Outlook Real GDP (%) Industrial World Developing World Global Economy CEEMEA Asia (Ex-Japan) Latin America Real GDP (%) Real GDP (%) Real GDP (%) Growth Growth Growth And then...the Financial Crisis:Impact on Short-term Economic Health Source: Morgan Stanley Research, December 2008

GFC Impact:Emerging Market Spreads Increased Dramatically Emerging-market Sovereign Bond Spreads: EMBI January 2007 – December 5, 2008 Emerging-market Corporate Bond (CEMBI) Spreads: January 2007 – December 1, 2008 Source: World Bank PPIAF Database

GFC Impact:Constrained Access to Capital • For new PPP projects : Reduced access to lending particularly from foreign banks,requirements for greater sponsor equity, shorter underwriting periods, more stringent conditions, and greater financing costs for long-term concessions • For existing PPP projects : Increased refinancing risk for long-term concessions, potential delays in refinancing with risk of cancellation and market disruption

GFC Impact: Project Closures Down 26% By Income Group: • upper middle income countries reporting lower investments • lower middle income countries attracting higher investments • low income countries seeing stable investments By Region: • Eastern Europe/Central Asia, Latin America/Caribbean hardest hit • Sub-Saharan Africa stable • Asia and the Pacific, and the Middle East and North Africa attracting higher investment By Sector: • Transport, energy and water reporting lower investments

But PPP Remains an Actively Pursued Option • Increasing public infrastructure demands worldwide • Fiscal constraints place more importance on private sector engagement • Fiscal stimulus responses to global financial crisis focus on infrastructure …Countries continue to tender/award new PPP projects and/or prepare new project pipelines

Asia Pacific PPPs: A Diverse Picture of “Stars and Black Holes”Total 2007 PPP Investment, US$ Million Kazakhstan 833 China 7,456 Afghanistan 240 Pakistan 4,487 India 22,485 Philippines 4,386 Viet Nam 1,332 Thailand 1,050 Malaysia 1,057 Cambodia 816 Sri Lanka 387 Papua New Guinea 150 Indonesia 1,441 Source: World Bank PPIAF Database

Recent Asia PPP Trends:Enormous infrastructure demand(Annual infrastructure needs, 2005-2010) In US$ Million Source: World Bank Policy Research Working Paper

India: World’s Biggest PPP Market?Average Project Size Reaching Financial Close, US$ Million

Extensive but very domestic Extensive but limited sectors Mainly IPPs, trying others A few IPPs or nothing much at all Asia Pacific Region: PPP Country Readiness Complete buy-in, institutionalized, open, international, physical & social infrastructure Extensive, established, largely domestic, mainly physical infrastructure

Latin America: PPP MarketPrivate-Sector Commitments to Infrastructure Investment, US$ Million

Emerging Market PPPs: Capacity and Knowledge Gaps are Key Bottlenecks • Public Sector: PPPs a “new procurement approach” that requires “new PPP skills” • Private Sector: A new market opportunity that requires market intelligence to evaluate “emerging country” opportunities

MP3IC: Global PPP Learning Program • Cutting edge learning modules to enable PPP institution building and development of PPP practitioner skills • Benchmarking tools to identify gaps and remedy PPP institutional and policy frameworks which deter investors

MP3IC: Global PPP Learning ProgramStrategic Design • Designed as a global learning product with features to adapt to country circumstances • Customized to multiple audiences – policy makers, managers, professional and technical staff • Based on multiple global comparative analyses and tools • MP3IC Country and Project Case Studies • Law and Infrastructure website • Global PPP Readiness Index

MP3IC Global Comparisons: Infrastructure & Law Websitewww.worldbank.org/inflaw Takes users through the PPP project development process - starting with Government Objectives, then moving on to Legal and Regulatory Frameworks and Agreements

MP3IC Global Comparisons: Infrascope Readiness Scorecard 1. Legal and regulatory framework 1.1 Consistency and quality of PPP regulations 1.2 Effective PPP selection and decision making 1.3 Fairness/openness of bids, contract changes 1.4 Dispute resolution mechanisms 2. Institutional framework 2.1 Quality of institutional design 2.2 PPP contract, hold-up and expropriation risk 3. Operational maturity 3.1 Public capacity to plan and oversee PPPs 3.2 Methods and criteria for awarding projects 3.3 Regulators’ risk allocation record 3.4 Experience in transport & water concessions 3.5 Quality of transport and water concessions 4. Investment climate 4.1 Political distortion 4.2 Business environment 4.3 Social attitudes towards privatization 5. Financial facilities 5.1 Government payment risk 5.2 Capital market: private infrastructure finance 5.3 Marketable debt 5.4 Government support for low income users

Public Sector Comparing PPP Attractiveness Identifying what it takes to improve PPP attractiveness Prioritizing actions to improve PPP attractiveness Private Sector Identifying Opportunities Evaluating Conditions Predicting Bottlenecks MP3IC Global Comparisons: PPPI Approaches

ADB Business Forum PPPI Knowledge Sharing - Comparing PPP Programs, Projects, and Country Readiness PPPI Days Conference PPPI Knowledge Sharing – Frontier Issues in Global PPP Development 9-10 November 10 November 11-12 November 13 November PPPI Days 20099-13 November 2009, Manila Philippines

PPPI Days 2009:PPPs in a Changing Global Environment • Revisiting Risk in the Aftermath of Global Financial Crisis • Megacities and Rise of Urban PPPs • Climate Change and Greening of PPPs • Escalating Demand for Social Services • Globalization and Increasing Need for Harmonization

PPPI Days 2009:New PPP Frontiers • Social Sectors – Unlocking PPP Potential for Human Capital Development • Bundled Service Delivery and Multisectoral PPP Approaches • Harmonization and Cross Border PPPs • Challenges for PPPs in Fragile and Small Island States

MDBs Role in Changing Landscape • Strengthening policy guidance and Bringing additional financial and technical expertise • Expanding lending programs to assist in rapid delivery of infrastructure projects • Offering innovative range of credit enhancements and risk mitigation measures

Investment Catalytic Transactions Entrepreneurship Economic Growth Enabling Poverty MDBs Environment Alleviation MDBs Role in Changing Landscape

![Global Micro Irrigation Market,Opportunities, Segmentation And Forecast [2015 - 2021]](https://cdn4.slideserve.com/7281964/slide1-dt.jpg)