Download

1 / 45

450 likes | 660 Views

UNDERGRADUATE STUDENT MANAGED FUND . Interim Report December 4, 2009. Undergraduate Team. Officers Michael Bokoff – Lead Manager Jeffrey Annello – Portfolio Manager Simone Hill – Treasurer . Managers Connor Antisdale Gregory Autuori Michael Baldi Ethan Beschler Juan Casanova

E N D

UNDERGRADUATE STUDENT MANAGED FUND Interim Report December 4, 2009

Undergraduate Team Officers Michael Bokoff – Lead Manager Jeffrey Annello – Portfolio Manager Simone Hill – Treasurer Managers Connor Antisdale Gregory Autuori Michael Baldi Ethan Beschler Juan Casanova Ameya Gokarn Steven Reiman Jennifer Sataline

Investment Objective & Philosophy Objective: We aim to outperform the S&P 500 Index Philosophy:What would a prudent business person do? • Buy the entire business • Good businesses and talented managers • Focus on companies that are trading well below their intrinsic value • Long-term orientation: 5-10 year holding period • Bottom-up , with a top-down look in current environment

Investment Strategy Goal: Own 15-20 well-chosen businesses selling at advantageous prices What we look for in a business • Recurring free cash flow • Sound capital allocation • Enduring competitive advantage • Sound and ethical management • Transparency • Looking at Risk • Aggregation risks • Business model risks • Balance sheet risks • Valuation risks • Management risks

Investment Process • Ten sectors, each covered by two or three managers • Research is focused on, but not limited to, assigned sectors • Stock is brought to a meeting for presentation and peer evaluation • The manager recommending a stock will lead the discussion • 70% vote in favor of a position, price limit, and quantity is required for approval • Positions not approved may be reintroduced at a later meeting • To date, 9 of 20 recommended stocks chosen

Portfolio Breakdown & Approach • Seek to take positions anywhere from 2.5% to 15% of our assets at cost • 2.5% position • Generally has a higher upside • Relatively higher risk • 10%-15% position • Core companies • Possess AAA style balance sheets • Trading below their intrinsic value • When fully allocated, the portfolio will be composed of 15-20 businesses • Diversified activities • Minimally correlated risk exposure • We evaluate each position as if we owned the entire business

Sector Allocation As of November 20, 2009

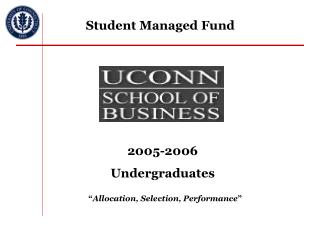

Economic Summary • Bank failures • Credit markets tightened • Government bailouts • Weakening of the dollar • Incredibly Volatile • S&P 500 • March 2008 to March 2009: (48%) • Low: 676.53 • March 2009 to present: 64% • 12/2/09 close: 1109.24 S&P 500 2-Year Chart (48%) 64%

Economic Indicators • 3Q 09 • Real GDP increased by 3.2% • Productivity increased by 8.1% • Freight: Rail cars in storage decreased by over 11,000 in October • Capacity utilization increased to 70.7% in November • Factory orders increased 0.9% • Initial and continuing jobless claims decreased during November • Business inventories decreased during November • New home sales increased by 25,000 during November • Causes for concern • Unemployment rate still at 10.2% • Crude Inventories have increased along with price • Expansion of the Fed’s balance sheet

Economic Outlook • Short Term • Unemployment (10.2%) • Overconfidence • Long-Term • Inflation • Consistency with the Fed’s outlook: • “My own view is that the recent pickup reflects more than purely temporary factors and that continued growth next year is likely. However, some important headwinds--in particular, constrained bank lending and a weak job market--likely will prevent the expansion from being as robust as we would hope.” - Ben Bernanke

Economic Outlook: How does this affect our strategy? • International exposure • MCD • Looking to invest in energy due to inflation concern • Asset inflation? • XOM, RDS • Pricing power/dominant position • MDT • Strong balance sheets • JNJ, BRK

Risk Management • We seek to manage risk in a variety of ways, including: • Detailed research • Extensive group discussion • Diversification among industries • Active avoidance of business model risk, valuation risk, management risk, and others • Formal risk management • Stop-loss orders at levels approximately 30% below our cost basis • Constantly evaluate holdings • Automatic downside review at 10%, 20% below our cost basis • In the event of a triggered stop-loss, we will thoroughly review the position and evaluate its future investment prospects

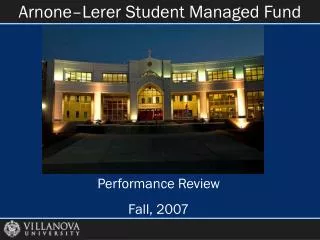

Sector Performance As of November 20, 2009

Portfolio Performance Holding period: October 27, 2009—December 1, 2009 As of December 1, 2009, the Undergraduate SMF Portfolio has underperformedthe S&P 500 index by 1.20%

Future Considerations • Looking to invest in Utilities, Energy & Transportation sectors • Increase our stake in the Materials sector • Researching both small and large-sized companies • Closely monitoring economic trends that will affect our current and future positions

Lessons Learned • Cannot be overly price sensitive • Going forward, we must continue to: • Research and evaluate the economy, sectors, and individual securities • Have conviction in our evaluations of individual securities • Purchase securities at reasonable valuations with attractive return potential, while avoiding being overly price sensitive • Deploy capital in an appropriate asset allocation in a timely manner

Research Sources • Yahoo! Finance • Google Finance • Bloomberg • Reuters • Wall Street Journal • BusinessWeek • Vcall • Association of American Railroads • Seekingalpha.com • S&P Net Advantage • Morningstar • Valueline • Thomson Research • EDGAR Filings • Mergent Online • Earnings Calls • Annual Reports • Federal Reserve Site

Acknowledgements • Pat Terrion • Dr. ChinmoyGhosh • Shikha Sharma • Steering Committee • Investment Advisory Board • Mentors • UConn Foundation

Capital Goods Industrials • 14.7% expected decline in manufacturing for 2009 • Optimistic for 2010 through global stimulus spending programs with an emphasis on infrastructure • Increased liquidity and easing credit should help Aerospace & Defense • Commercial Airlines had a tough 2009; outlook is uncertain but optimistic • 2010 Defense budget calls for 4.2% increase in base budget but is expected to shrink down the line • Consolidation of the industry is expected as a result of the focused budget cuts

Consumer Discretionary & Services • The sector has returned 32.65% versus the S&P 500’s 22.87% return YTD • Positive Trends • Equity market increases have restored some of the wealth lost since 2008 • Consumer confidence is improving • Consumer savings rates are normalizing • Consumers’ discretionary incomes are low, however they are steadily increasing • Why we will be cautious • The unemployment rate is currently 10.2%, however additional job loss expected • Banks and other depository institutions are holding unprecedented amounts of reserves; credit markets have remained tight • Many stocks are trading at historically high earnings multiples, making the outlook for this sector mixed

Consumer Staples • Subsectors: • Food and beverage retail and distribution • Household and personal products • Demand for consumer staples remains relatively constant regardless of the economy • Trade-down effect: • However, we have noticed a pattern in consumers purchasing less expensive, generic goods as opposed to name brand goods • We’re seeking companies that are prepared regardless of the direction of the economy • Low-priced products to protect against a downturn • Loyal customer base to prevent a drop off should the economy pick up

Energy • Economic rebound supports a positive outlook • Number of operational oil rigs and natural gas rigs is crawling back up • Oil prices increased dramatically from previous year’s lows • Demand for oil and natural gas will increase with growing world markets (China, India) and rising populations • Forecasted colder-than-average winter should increase demand from heating needs

Financials • US and global economies starting to see relief from financial market stress • Detrimental factors affecting financial companies: • Volatility in global financial markets • Credit tightening • Falling home prices • Increasing delinquencies, both commercial and residential • Rising unemployment • Why we are hesitant to invest in financial company equities: • Uncertainty surrounding financial sector • Limited ability to understand full exposure to risky assets and uncertain values • Government bail-out money…end results of programs such as TARP? • Imminent financial reform • Legislation that might break up large financial institutions • Dodd’s call to establish a council of financial regulators that could require such companies to divest holdings

Healthcare • Largest sector, with $2.4 trillion spent in the U.S. in 2008 • Spending expected to rise 5.5% in 2009 • Worldwide pharmaceutical sales expected to increase 2.5% to 3.5% in 2009. • Pharmaceuticals traditionally seen as recession-resistant • High volume of M&A activity among large pharmaceuticals • Relatively weak R&D productivity and impending patent expirations • Aging populations are likely to create a robust future for the healthcare industry • Strong growth in emerging markets throughout the next 5 years • Medical products & supplies industry remains favorable • Uncertainty surrounding Obama’s healthcare reform agenda

Materials • Majority of materials companies have rebounded sharply since March • Investors continuing to move into commodities as inflation hedge • Price of gold has moved to over $1200 an oz • Gold futures up about 37% this year • Steel sub-sector has begun to consolidate potentially higher pricing power • Worldwide shortage of usable fresh water • Water transportation, desalinization, treatment, and infrastructure companies should benefit

Technology • Technology expenditures down YTY • Should rebound in 2010 • Emerging markets forecast to lead IT demand • Trends • Data Storage/management demand increasing • Move toward virtualization, non-hardware based technology

Transportation • Conditions are challenging, some signs of recovery • Freight rail traffic down 15.3% in carloads, and 11.2% intermodal YOY • Excess capacity in trucking industry downward pressure on freight rates • High fuel prices • “Flight to quality” • Decline in rail freight cars in storage • Outlook • Outsized returns unlikely • Warren Buffett --acquisition of Burlington Northern Santa Fe (BNI)--betting on the long-term future growth of the industry • Possible that holiday season will serve as a further stimulus. • Transportation stocks often lead economic recovery

Utilities • Price performance vs. S&P 500 YTD • Positives • Many issues are trading at historically low multiples and have attractive dividend yields • Negatives • The industry is highly regulated, including firms’ pricing power and return on equity • Competition is monitored and it is difficult to find businesses with distinct competitive advantages

AutoZone (AZO) • Specialty Retailer – 4,417 stores • Auto replacement parts, discretionary items • Serves the DIY market • ALLDATA diagnostic software • Best in class ROC and margins • 9.5% free cash flow yield • Bought back 2/3 of company in a decade • 40% owned by ESL Partners

Berkshire Hathaway (BRK.B) • Warren Buffett’s holding company. • Equity stakes in KO, WPO, KFT, WFC, COP among others. • High quality operations in: • Insurance and reinsurance • Utilities • Railroad (BNSF) • Retail/Services • Lender of first resort, Buyer of first resort • Bought at 75% of true business value.

ITT Corporation (ITT) • 3 Business Segments • Fluid Technologies (33%)- Pumps and fluid systems • Defense Electronics and Services (54%)- Advanced electronic systems • Motion and Flow Control (13%)- provides integral components for aerospace, industrial, transport, medical, and consumer markets • Fluid Tech. should benefit from infrastructure projects • DES has contracts with every branch of the armed forces • Motion and Flow is highly globalized (63% of its rev. from abroad) • Each branch provides a diversified product mix industry leaders • Generated a 21% increase in FCF in 2009 YTD • Improved Receivables collections • 40 bps improvement in working capital as % of sales

Johnson & Johnson (JNJ) • One of the largest and most diversified healthcare firms with both pharmaceutical and medical device products. The company also produces many consumer products. • Diversified sales stream throughout segments • Decentralized business model • Very active in the M&A market

Lockheed Martin Corporation (LMT) • One of the top U.S. defense contractors • Services, Researches, Designs, and Manufactures a wide range of products in the field of Aerospace and Defense • F-35 aircraft looks to be the future of defense aeronautics • Company is well positioned within U.S. war strategy • Consistently high Cash Flow numbers, and 2008 saw an all time high in sales over $42B

McDonald’s Corporation (MCD) • Purchased 1,150 shares of McDonald’s Corporation at a price of $62.75 • Company Strengths • Exceptional ability to adapt to changing consumer preferences • Large international exposure • Strong, growing presence in Europe • Growth plans in emerging markets • Stellar management, evidenced by the success of their “Plan to Win” • As of November 20th, 2009, we have realized a 1.9% return on our position in McDonald’s

Medtronic (MDT) • World’s largest medical technology company • Main operating segments include Cardiac Rhythm Management, Spinal, Cardiovascular, Diabetes and Surgical Technologies • Recently announced earnings of $0.77 per share in Q2, beating analyst predictions by $0.03 • Consistently allocates a significant portion of its sales towards R&D • Planning on releasing new products in virtually all of its operating segments • Generates consistently high free cash flow, with a free cash flow yield of 7% in 2009

Sanofi-Aventis (SNY) • A pharmaceutical group engaged in the research, development, manufacture and marketing of healthcare products • Broad product portfolio • Strong R&D Focus • Market leadership in vaccines • Global presence

Sysco Corporation (SYY) • We purchased 1,800 shares of Sysco Corporation at a price of $26.79 per share on October 30, 2009 • Company Strengths • Diversified customer and supplier base • Dominant market share provides bargaining power • Consistent history of dividends • Distribute both name-brand and generic products • Current emphasis on cutting costs and improving efficiency • As of November 20th, 2009, we have realized a return of 0.9% on our position in Sysco