Download

1 / 16

590 likes | 2.01k Views

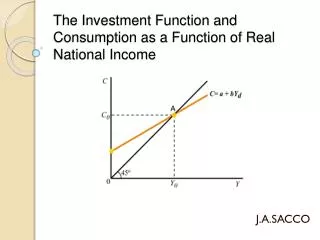

Chapter 6. Investment Function. Investment Function. 1. Significance * Principal determinant of economic growth * Principal cause of business cycles * Stabilization policies operate via investment * S = I for the world but not necessarily for country. 2. What is investment ?.

E N D

Chapter 6 Investment Function

Investment Function 1. Significance * Principal determinant of economic growth * Principal cause of business cycles * Stabilization policies operate via investment * S = I for the world but not necessarily for country 2. What is investment ? * Three components : - Fixed non-residential (business) investment (plant + machines) (new) (largest) • Fixed residential investment (households and firms) • (new) - Inventory investment (small but most volatile)

* Produced means of production * Not purchase of shares or bonds. • * Incremental capital stock: • I = capital stock (physical), Not human capital, a flow variable Capital stock = Rupee value of all the buildings, machines and inventories at a point in time.

* Dual role -Component of AD -Capacity creator (AS) : produced FOP High powered expenditure * Self-terminating, self financing * Most volatile component of AD Source of business cycles * Serves the primary link for monetary policy & a counter factor to fiscal policy

3. Motivations for Investments • Business fixed investment • -Profit motive -Innovation -Relative factor price advantage • Inventory investment -Production smoothing -Factor of production -Stock out avoidance -Work in progress • Residential investment -Housing: own/staff

4. Investment and capital Capital Stock (6.1) • Adjustment function: Actual vs. Desired Investment It = Kt - Kt-1 = (Kt* - Kt-1) (6.2) 1 Thus, It = f(Kt* , Kt-1) (6.3) f1 > 0 > f2

5. Investment theories: Determinants of all investments (i) Change in output (Accelerator Theory) K* = AY (6.4) K* = A Y or, I* = A (Y - Y-1) (6.5)

Limitations: - excess capacity • - temporary increase in demand - funds and plants constraints - asymmetry in investments • Lagged accelerator I* = A(Y-1 - Y-2) (6.6)

(ii) Output (Profit theory) • Retained profit as a source of fund • Profit varies directly with output • Neo classical theory Y = f ( K, L) (6.7) C = R K + W L (6.8) MPPK/ R = MPPL/ W (6.9) K = ǿ( Y, R/W ) (6.10) ǿ1 > 0 > ǿ2

e (iii) Interest Rate (Real) MPK = R / P (6.11) R / P = CoC COC = i + d - Or, COC = r + d (6.12) MPK = r + d (6.13) Gross and net investment (iv) Wage rate vide Neo-classical theory, equation(6.10)

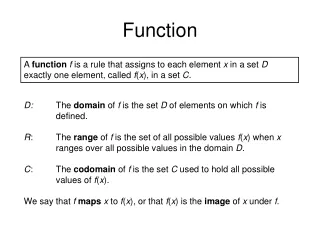

Figure 6.1: Investment Schedule / Curve Real Interest rate Investment

(v) Tobin’s Q Q = (6.14) (vi) Tax laws - Depreciation issue - Tax rebate on housing loan & interest there on - Investment tax credit, capital subsidy, tax concessions/ holidays - Minimum alternative tax (vii) Financing constraints/ Firm balance sheet - Retained profit - Credit rationing - Ability to borrow (viii) Technology Knowledge based industries • Business confidence/ stock market behavior • Government policy

6. Investment Function I = f (Y, r, w, Q, FMP, F, T, BC, Y-1, K-1, u) (6.15) f1,f3,f4,f7,f8 > f2, f6, f9, f10 f5, f11 >< o

7. Specific determinants for specific investments 7.1. Private / induced non-residential investment • Change in output / demand (+ve) • Output (+ve) • Interest rate (-ve) (Real = Nominal – exp inflation): Marginal efficiency of capital schedule • Corporate tax rate and tax shields on investments

Availability of credit • Firms balances sheet (retained earning /reserves) (+ve) • Wage rate vis-à-vis cost of capital (+ve) • Tabin’s q (+ve) • Business expectations / confidence • 7.2 Public/Autonomous investment • Innovations / inventions / technical progress • Social benefit-cost analysis • Policy variable

7.3. Fixed residential investment * Mortgage rate/credit availability (-ve) * Wealth/income (+ve) * Return on non-housing investments (-ve) * Tax incentives (+ve) • 7.4. Inventory Investment • * Expected sales (+ve) * Inventory carrying cost (r + d) (-ve) • * Inventory shortage cost (+ve) • - Square root formula