Download

1 / 27

270 likes | 446 Views

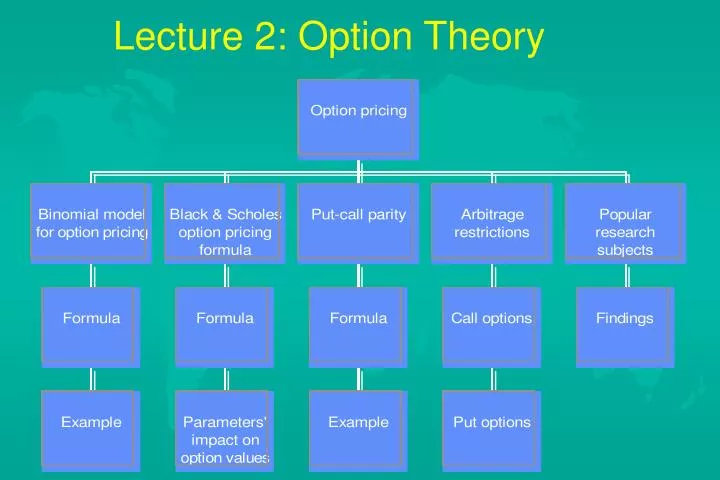

Lecture 2: Option Theory. How To Price Options. The critical factor when trading in options, is determining a fair price for the option. The binomial model for option pricing. Computes the value of a call option

E N D

How To Price Options • The critical factor when trading in options, is determining a fair price for the option.

The binomial model for option pricing • Computes the value of a call option • The value can change only at the end of the period (t+1) and the possible maximal and minimal values are currently (t) known.

Explanations of the parameters C = Call option = Call value at t+1, when stock price goes to max. = Call value at t+1, when stock price goes to min. = Riskless interest rate u = Multiplicative upward movement in stock price (S) d = Multiplicative downward movement in stock price (S)

Features of the binomial model • The formula doesn’t depend on investors’ attitudes towards risk • Investors can agree on the relationship between C, S and r even if they have different expectations about the upward or downward movement of C

The only random variable on which the call value depends, is the stock price itself • p can take values between 0 and 1 (0 < p < 1). If investors were risk neutral then p=q.

A Short Example K = 15 mu (striking price) S = 20 mu = 25 mu = 15 mu = 10 monetary units = 0 mu r = 1,06 ( 6 %) u = 1,25 d = 0,75

The Black & Scholes formula(A continuous time formula) • “It is possible to create a risk free portfolio” by owning 1 stock and writing hcall options on it.” • The most frequently used option pricing formula • Originally a heat transfer equation in physics

Assumptions behind the formula: 1. The stock price follows a continuous Wiener- process and the future stock prices are lognormally distributed. 2. There exist no transaction costs or taxes. 3. No dividends are paid during the lifetime of the option. 4. The capital market is perfect: there exist no arbitrage-possibilities. 5. The composition of the portfolio can be continuously adjusted. 6. The risk free interest rate is constant during the lifetime of the option.

Black & Scholes Option Pricing Formula where Copeland & Weston. 1988. p 276.

Parameters C = The price of the call option S = Stock price N = The standard normaldistribution = The continuous risk free rate of return [=ln(1+ )] t = The time to expiration (if 63 days, then t=63/365) K = Striking price = The variance of the stock return

N(d1) = the inverse hedge ratio e.g. for each stock that is owned, 1/N(d ) options has to be written for the portfolio to be risk free. = the discounted value of the striking price. N(d2) = the probability for the option to be “in the money” on due date (e.g. the option will be exercised).

The price of an option is dependent on the following parameters: P C • Current stock price (S) • Time to expiration (t) • Striking price (K) • Stock volatility • Interest rates (Cash dividends)

The Put-Call Parity: • There is a connection between the price of a call and a put option • If the prices differ from this equation, there exist arbitrage opportunities

An intuitive example • Buy a share: S = 19 mu • Buy a put option: P = 1 mu (striking price K = 20 mu) • Buy a call option with the same striking price and maturity: C = 1,50 mu • Deposit 18,50 mu at the risk free rate r = 10,95% 1 + 19 = MAX(19-20,0) + 20 = 20

Outcome 9 months later on expiration date Discounted to t(0) Prolonged to t Put + Share = Call + Deposition 3 + 17 = 0 + 20 in the money out of the money Input vaules: r=10,95%;t=0,75; K=18,50;C=1,50;P=1;S=19

If we take cash dividends (D) into consideration the formula is slightly modified • Further modifications required if applied on american options Dividends

Arbitrage restrictions on call values(1) The value of a call is never less than the larger of: • zero • S - K (2) The value of a call is never greater than: • the price of its underlying stock The amount of cash deposited In other words: (equals to K)

Call price Stock price C = S Cox & Rubinstein. 1985. p 131.

Cox & Rubinstein. 1985. p 136. Call price Striking price C = S - K S C

Arbitrage restrictions on put valuesThe value of a put is never less than the larger of • zero • K-S The value of a put is never greater than • its striking price The amount of cash deposited In other words: (equals K)

Put price Stock price K K - S Cox & Rubinstein. 1985. p 147.

Putprice P = K - S Striking price P = K P Cox & Rubinstein. 1985. p 148.

Popular research subjects • Forecasting the future volatility (Engle Robert F.: “Statistical Models for Financial Volatility”, Financial Analysts’ Journal Jan/Feb 1993) • Comparing the theoretical and the actual pricing of options (Kahra Hannu: “Pricing FOX Options Under Conditional Heteroscedasticity In Returns”, Tampere Economic Studies 1/1992)

Option Valuation under Stochastic Volatility. With Mathematica Code. (Alan L. Lewis, Finance Press, NewPort California, 2000) • Option pricing, using distributions other than the standard normal distribution (Cox John C & Steven A. Ross: “The Valuation of Options for Alternative Stochastic Processes”, Journal of Financial Economics Jan-Mar 1976)

Findings: • Call options tend to be overpriced • Put options tend to be underpriced • Volatility seems to be forecastable in the short run • Only the broker makes profits in the long run