Download

1 / 25

260 likes | 452 Views

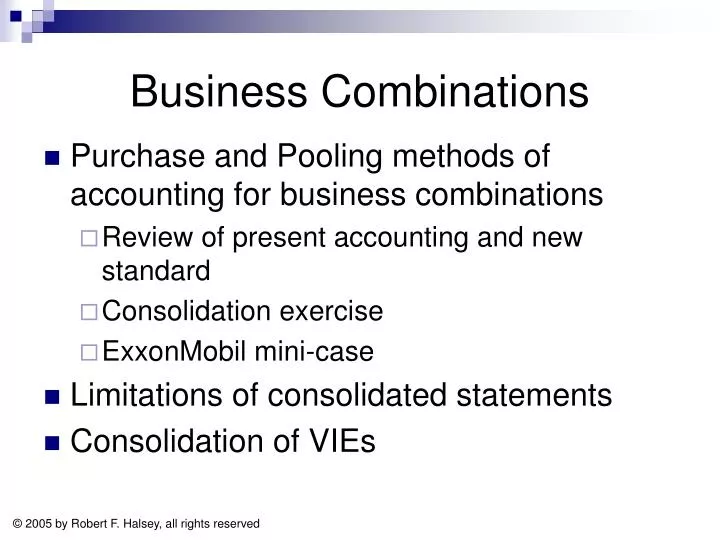

Business Combinations. Purchase and Pooling methods of accounting for business combinations Review of present accounting and new standard Consolidation exercise ExxonMobil mini-case Limitations of consolidated statements Consolidation of VIEs. Business Combinations Standard FAS 141/142.

E N D

Business Combinations • Purchase and Pooling methods of accounting for business combinations • Review of present accounting and new standard • Consolidation exercise • ExxonMobil mini-case • Limitations of consolidated statements • Consolidation of VIEs

Business Combinations Standard FAS 141/142 • Use Purchase method only (no pooling) • Record FMV of acquired tangible and intangible assets and depreciate/amortize these assets over UL unless the intangible asset has an “indefinite life” (e.g., goodwill ) • I/S reflects costs relating to FMV of acquired tangible assets and amortization of identifiable intangible assets (no amortization of goodwill) • Record goodwill for the excess (“Negative Goodwill” is recognized immediately as an extraordinary gain). • Goodwill is not amortized, but is tested annually for impairment. Also applies to goodwill in equity method investments. • Effective date: acquisitions after 6/30/01, and for fiscal years beginning after 12/15/01. • Affects preexisting goodwill.

Consolidation exercise Purchase Price Allocation:

Investment balance – equity method + Investment -

Pooling of interest method (no longer used in US) • Record assets/liabilities of target at book values (not FMV) • No goodwill recorded • Depreciation / amortization expense is less.

Acquired Identifiable Intangibles • Intangibles • Current and noncurrent assets that lack physical substance. • Do not include financial instruments. • When should an Intangible be recognized? • Does it arise from contractual or other legal rights? • Can it be sold or otherwise separated from the acquired enterprise?

Marketing-related intangible assets Trademarks, tradenames Service marks, collective marks, certification marks Trade dress (unique color, shape, or package design) Newspaper mastheads Internet domain names Noncompetition agreements Customer-related intangible assets Customer lists Order or production backlog Customer contracts and related customer relationships Noncontractual customer relationships Artistic-related intangible assets Plays, operas, ballets Books, magazines, newspapers, other literary works Musical works such as compositions, song lyrics, advertising jingles (4)Pictures, photographs Video and audiovisual material, including motion pictures, music videos, television programs Contract-based intangible assets Licensing, royalty, standstill agreements Advertising, construction, management, service or supply contracts Lease agreements Construction permits Franchise agreements Operating and broadcast rights Use rights such as drilling, water, air, mineral, timber cutting, and route authorities Servicing contracts such as mortgage servicing contracts Employment contracts Technology-based intangible assets Patented technology Computer software and mask works Unpatented technologies Databases, including title plants Trade secrets, such as secret formulas, processes, recipes. Types of intangible assets that must be recorded (SFAS 141, Appendix A)

Tangible assets Acquired intangible assets Liabilities assumed IPR&D Hewlett-Packard provides the following allocation of its $24.2 billion purchase price for Compaq Computer in the footnotes to its 2002 10-K.

Investment yes FMV < CV? Mkt. Price reporting unit -FMV net equity Implied Goodwill - CV Goodwill Impairment loss Goodwill impairment test FMV=fair market value CV = carrying value Note: not an issue for poolings

The following footnote disclosure from Intel’s 2003 10-K explains its goodwill impairment process: During the fourth quarter of 2003, the company completed its annual impairment review for goodwill and found indicators of impairment for the Wireless Communications and Computing Group (WCCG) reporting unit… In the fourth quarter of 2003, it became apparent that WCCG was now expected to grow more slowly than previously projected… and triggered the goodwill impairment [review]. The impairment review requires a two-step process. The first step of the review compares the fair value of the reporting units with substantial goodwill against their aggregate carrying values, including goodwill…Based on the comparison, the carrying value of the WCCG reporting unit exceeded the fair value. Accordingly, the company performed the second step of the test, comparing the implied fair value of the WCCG reporting unit’s goodwill with the carrying amount of that goodwill. Based on this assessment, the company recorded a non-cash impairment charge of $611 million, which is included as a component of operating income in the “all other” category for segment reporting purposes. Have shareholders suffered a loss?

Effects SFAS 140/141 (Business Combinations) • We see both purchased intangibles and goodwill on balance sheet • Profits have increased due to elimination of goodwill amortization • We will see significant future write-off amounts if goodwill becomes impaired

Gains on Sub IPOs TYCOM LTD During Fiscal 2000, TyCom Ltd., a majority-owned subsidiary of the Company, completed an initial public offering (the "TyCom IPO") of 70,300,000 of its common shares at a price of $32.00 per share. Net proceeds to TyCom from the TyCom IPO, after deducting the underwriting discount, commissions and other direct costs, were approximately $2.1 billion. Of that amount, TyCom paid $200 million as a dividend to the Company. Prior to the TyCom IPO, the Company's ownership in TyCom's outstanding common shares was 100%, and at September 30, 2001 the Company's ownership in TyCom's outstanding common shares was approximately 89%. As a result of the TyCom IPO, the Company recognized a pre-tax gain on its investment in TyCom of approximately $1.76 billion ($1.01 billion, after-tax), which has been included in net gain on sale of common shares of subsidiary in the Fiscal 2000 Consolidated Statement of Operations.

Gains on Sub IPOs • Assume that an investor company owns 100% of its investee with a book value for its stockholders’ equity of $1,000,000. • Also assume that the investee company issues previously unissued shares for $500,000 and, thereby, reduces the investor’s ownership to 80%. • The investor company then owns 80% of a subsidiary with a book value of $1,500,000 for an investment equivalent of $1,200,000 (80% × $1,500,000). • The value of its investment account has, thus, risen by $200,000. • This increase in the investment account can be recorded as income or a credit to APIC.

IPO accounting examples Treatment as a gain - Citigroup: Treatment as an increase in APIC – Barnes & Noble:

Purchased In-Process R&D • Under former standard, earnings drag was a problem. • Solution: allocate significant portion of purchase price to purchased R&D and write off immediately under R&D accounting standard (FAS 2) • Effect: large loss in period of acquisition; less earnings drag in future statements because goodwill is reduced • Note: in the proposed amendment to FAS 142, IPR&D will be capitalized and tested annually for impairment, not expensed

Hewlett-Packard, in its $24.1 billion acquisition of Compaq Computer, allocated $735 million to IPR&D: In-process research & development Of the total purchase price, $735 million was allocated to IPR&D and was expensed in the third quarter of fiscal 2002. Projects that qualify as IPR&D represent those that have not yet reached technological feasibility and for which no future alternative uses exist. Technological feasibility is defined as being equivalent to a beta-phase working prototype in which there is no remaining risk relating to the development. The value assigned to IPR&D was determined by considering the importance of each project to the overall development plan, estimating costs to develop the purchased IPR&D into commercially viable products, estimating the resulting net cash flows from the projects when completed and discounting the net cash flows to their present value. The revenue estimates used to value the purchased IPR&D were based on estimates of the relevant market sizes and growth factors, expected trends in technology and the nature and expected timing of new product introductions by Compaq and its competitors. The rates utilized to discount the net cash flows to their present values were based on Compaq's weighted average cost of capital. The weighted average cost of capital was adjusted to reflect the difficulties and uncertainties in completing each project and thereby achieving technological feasibility, the percentage-of-completion of each project, anticipated market acceptance and penetration, market growth rates and risks related to the impact of potential changes in future target markets. Based on these factors, discount rates that range from 25%-42% were deemed appropriate for valuing the IPR&D.

Effects of current exposure draft • Transactions valued at closing date, vs. agreement date (future acquisition price is uncertain) • IPR&D will be capitalized as an indefinite lived asset until completion or abandonment of the project, then depreciated or written off • Restructuring costs will be expensed (vs. accruing a liability) • Acquisition-related costs will be expensed • Bargain purchases will be recorded as an extraordinary gain (vs. current practice of reducing carrying amount of L-T assets w/ gain for excess) • Contingent consideration will be recognized and re-valued annually (I/S effects: better results of sub expense, not income) • Noncontrolling interests will be reported as equity (vs. mezzanine) • Any incidence of control will be treated as a business combination (valued at market), even if via contract with no consideration. • No longer a presumption that development stage entities are not a business (treat acquisitions as business combinations vs. asset purchases)

Business Combinations vs. Asset Purchases • Identifiable assets valued at market under both • No liabilities recorded under asset purchase unless assumed • No goodwill recorded under asset purchase (total price must be allocated to assets purchased) • Purchased IPR&D is capitalized for a business combination and expensed for an asset purchase • Contingent consideration is not valued in an asset purchase (vs. initial valuation and changes in future values run through income)

Limitations of Consolidated Statements • Income versus Cash Flow • The consolidated income statement reports the combined earnings of all consolidated entities, but the possibility of dividend restrictions as previously discussed can limit the ability of those earnings to be paid to the investor company. • Debt in Consolidated Financial Statements • In the absence of a specific guarantee of the debts of the subsidiary by the parent company, creditors have recourse in the event of default only to assets owned by the corporation that incurred the liability. • Financial statements individual companies that comprise the larger entity are not always prepared on a comparable basis. Differences in accounting principles, valuation bases, amortization rates, and other factors can inhibit homogeneity and impair the validity of ratios, trends, and other analyses. • Consolidated financial statements do not reveal cash flows of subsidiaries. • Companies in poor financial condition sometimes combine with financially strong companies, which can obscure analysis since assets of one member of the consolidated entity cannot necessarily be used to settle liabilities of another. • Intercompany transactions are generally unknown unless the procedures underlying the consolidation process are reported, but consolidated statements usually reveal only end results. • Aggregation of dissimilar subsidiaries with the total entity (e.g., manufacturing and finance) can distort ratios and other relations.

Consolidation of VIE’s • Value both sides of balance sheet independently: • Assets (any assets transferred from primary beneficiary are reported at cost - no write-up) • Implied Value (liabilities + noncontrolling interest + capital & retained earnings • Consolidation • FMV assets>implied value assets proportionately reduced • FMV assets<implied value extraordinary loss (no goodwill) • Eliminate intercompany transactions • Income allocated via contract, not stock ownership • Other disclosure requirements: • Description of VIE • Description of assets serving as collateral • Limitations of recourse against primary beneficiary • Consolidation is avoided for QSPEs