Download

1 / 2

20 likes | 285 Views

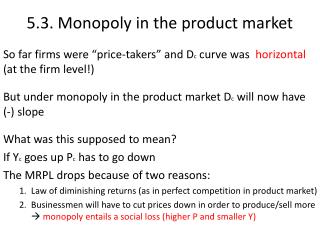

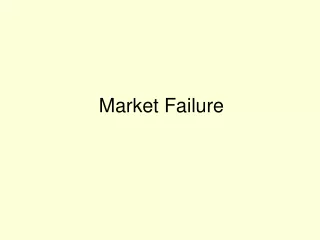

Competition, Monopoly, and Market Failure in the Market for Drugs. P*. c. Demand. MC=$1. a. b. Marginal Revenue. Quantity.

E N D

Competition, Monopoly, and Market Failure in the Market for Drugs P* c Demand MC=$1 a b Marginal Revenue Quantity This figure shows the equilibrium price for a medication over which the manufacturer has monopoly power. The profit-maximizing price P* is the price where marginal revenue equals marginal cost. Pareto efficiency requires that the price be equal to the marginal cost. Since price is much higher, there is an economic inefficiency: consumers between points a and b would be willing to pay more than $1 for the drug, but because the maximum they are willing to pay is < P* they will not obtain the medication.