Download

1 / 36

370 likes | 375 Views

Compare activity-based & strategic-based accounting, features of Balanced Scorecard, achieving strategic alignment, performance measures, rewards, strategy translation, and customer value in organizations.

E N D

The Balanced Scorecard: Strategic-Based Control Prepared by Douglas Cloud Pepperdine University

Objectives 1. Compare and contrast activity-based and strategic-based responsibility accounting systems. 2. Discuss the basic features of the Balanced Scorecard. 3. Explain how the Balanced Scorecard links measures to strategy. 4.Describe how an organization can achieve strategic alignment. After studying this chapter, you should be able to:

Activity-Based versus Strategic-Based Accounting The activity-based system adds a process perspective to the financial perspective of the functional-based responsibility accounting system. A strategy-based responsibility accounting system translates the strategy of the organization into operational objectives and measures.

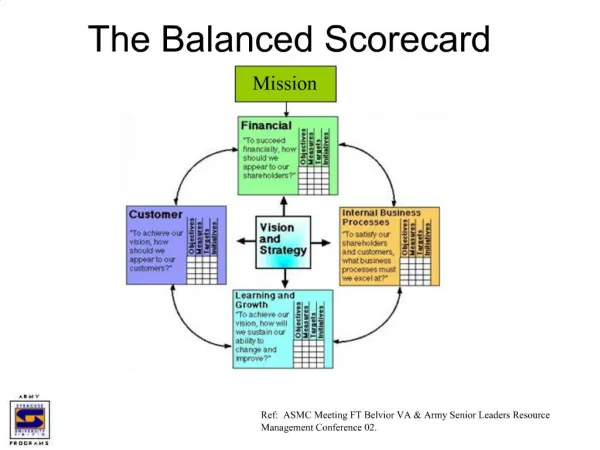

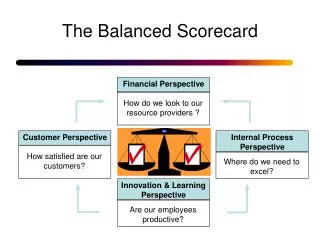

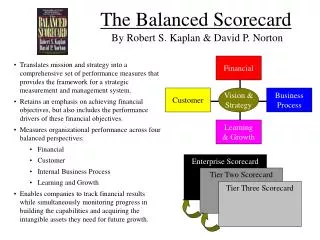

Activity-Based versus Strategic-Based Accounting The Balanced Scorecard is a strategic-based performance management system that typically identifies objectives and measures for four different perspectives. • The financial perspective • The customer perspective • The process perspective • The learning and growth perspective

Assigning Responsibility Activity-Based Responsibility Strategic-Based Responsibility 1. No tie to strategy 2. Systemwide efficiency 3. Team accountability 4. Financial perspective 5. Process perspective 1. Linked to strategy 2. Systemwide efficiency 3. Team accountability 4. Financial perspective 5. Process perspective 6. Customer perspective 7. Learning and growth perspective

Establishing Performance Measures Activity-Based Measures Strategic-Based Measures 1. Process-oriented and financial standards 2. Value-added standards 3. Dynamic standards 4. Optimal Standards 1. Standards for all four perspectives 2. Used to communicative strategy 3. Used to help align objectives 4. Linked to strategy and objectives 5. Balanced measures

ABC versus Strategic-Based Activity-Based Strategy-Based Performance Evaluation Performance Evaluation 1. Time reductions 2. Quality improvements 3. Cost reductions 4. Trend measurements 1. Time reductions 2. Quality improvements 3. Cost reductions 4. Trend measurements 5. Expanded set of metrics 6. Set stretch targets for all four perspectives

Rewards Compared Activity-Based Rewards Strategy-Based Rewards 1. Based on multidimensional performance 2. Group rewards 3. Salary increases 4. Promotions 5. Bonuses, profit sharing, and gainsharing 1. Based on multidimensional performance 2. Group rewards 3. Salary increases 4. Promotions 5. Bonuses, profit sharing, and gainsharing

Strategy Strategy is choosing the market and customer segments the business unit intends to service, identifying the critical internal and business processes that the unit must excel at to deliver the value propositions to customers in the targeted market segments, and selecting the individual and organizational capabilities required for the internal, customer, and financial objectives.

Financial Customer Process Infrastructure Objectives Measures Targets Initiatives Visions and Strategy Strategy Translation Process

Summary of Objectives and Measures: Financial Perspective Objectives Measures Revenue Growth: Increase the number of new Percentage of revenues from products new products Create new applications Percentage of revenue from new applications Develop new customers and Percentage of revenues from markets new sources Adopt a new pricing strategy Products and customer profitability Continued

Objectives Measures Cost Reduction: Reduce unit product cost Unit product cost Reduce unit customer cost Unit customer cost Reduce distribution channel Cost per distribution cost channel Asset Utilization: Improve asset utilization Return on investment Economic value added

Core Objectives and Measures • Increase market share • Increase customer retention • Increase customer acquisition • Increase customer satisfaction • Increase customer profitability Only financial measure Among the core objectives

Customer Value Customer value is the difference between realization and sacrifice, where realization is what the customer receives and sacrifice is what is given up.

Summary of Objectives and Measures: Customer Perspective Objectives Measures Core: Increase market share Market share (percentage of market Increase customer retention Percentage growth, existing customers Percentage of repeating customers Increase customer acquisition Number of new customers Increase customer satisfaction Ratings from customer surveys Increase customer Customer profitability profitability Continued

Objectives Measures Performance Value: Decrease price Price Decrease postpurchase costs Postpurchase costs Improve product functionality Ratings from customer surveys Improve product quality Percentage of returns Increase delivery reliability On-time delivery percentage Aging schedule Improve product image and Ratings from customer surveys reputation

Cycle Time and Velocity The time it takes a company to respond to a customer order is referred to as responsiveness. Cycle timeand velocity are two operation measures of responsiveness. Cycle time(manufacturing) is the length of time it takes to produce a unit of output from the time materials are received until the good is delivered to finished goods inventory. Velocityis the number of units of output that an be produced in a given period of time..

Conversion Cost Example A company has the following data for one of its manufacturing cells: Theoretical velocity: 40 units per hour Productive minutes available (per year): 1,200,000 Annual conversion costs: $4,800,000 Actual velocity: 30 units per hour

Actual Conversion Cost per Unit Standard cost per minute = $4,800,000/1,200,000 = $4 per minute Actual cycle time = 60 minutes/30 units = 2 minutes per unit Actual conversion cost = $4 x 2 = $8 per unit Theoretical Conversion Cost per Unit Theoretical cycle time = 60 minutes/40 units = 1.5 minute per unit Ideal conversion cost = $4 x 1.5 = $6 per unit Conversion Cost Example

Objectives and Measures: Process Perspective Objectives Measures Innovation: Increase the number of new Number of new products/total products products: R & D expenses Increase proprietary products Percentage revenue from proprietary products Number of patents pending Decrease product Time to market (from start to development cycle time finish)

Objectives Measures Operations: Increase process quality Quality costs Output yields Percentage of defective units Increase process efficiency Unit cost trends Output/input(s) Decrease process time Cycle time and velocity MCE Postsales Services: Increase service quality First-pass yields Increase service efficiency Cost trends Output/input(s) Decrease service time Cycle time

Objectives and Measures: Learning and Growth Perspective Objectives Measures Increase employee Employee satisfaction ratings capabilities Employee turnover percentages Employee productivity (revenue/employee) Hours of training Strategic job coverage ratio (percentage of critical job requirements filled)

Objectives Measures Increase motivation and Suggestions per employee alignment Suggestions implemented per employee Increase information systems Percentage of processes with capabilities real-time feedback capabilities Percentage of customer-facing employees with on-line access to customer and product information

Increase Shareholder Value Decrease Process Costs Increase Profits Increase Revenues Financial Improve Delivery Reliability Increase Customer Retention Increase Market Share Customer Casual Flow Diagram: Testable Strategy Illustrated Improve Cycle Time Redesign Process Internal Process Learning and Growth Improve Employee Skills

Targets and Weighting Scheme Illustrated Perspectives Objectives Financial (25%) Increase shareholder value (25%) Measures Targets Share price 50% increase

Targets and Weighting Scheme Illustrated Perspectives Objectives Financial (25%) Increase profits (25%) Measures Targets Profits Double

Targets and Weighting Scheme Illustrated Perspectives Objectives Financial (25%) Increase revenues (25%) Measures Targets Revenues 30% increase

Targets and Weighting Scheme Illustrated Perspectives Objectives Financial (25%) Decrease process costs (25%) Measures Targets Costs 20% decrease

Targets and Weighting Scheme Illustrated Perspectives Objectives Customer (25%) Increase market share (20%) Measures Targets Market share 25%

Targets and Weighting Scheme Illustrated Perspectives Objectives Customer (25%) Increase customer retention (30%) Measures Targets Repeat orders 70%

Targets and Weighting Scheme Illustrated Perspectives Objectives Customer (25%) Improve delivery reliability (50%) Measures Targets On-time percentage 100%

Targets and Weighting Scheme Illustrated Perspectives Objectives Internal Process (25%) Improve cycle time (60%) Measures Targets Cycle time 2 days

Targets and Weighting Scheme Illustrated Perspectives Objectives Internal Process (25%) Redesign process (40%) Measures Targets Yes or No Yes

Targets and Weighting Scheme Illustrated Perspectives Objectives Learning and Growth (25%) Improve employee skills (100%) Measures Targets Hours of training 30 hours per employee

End of Chapter