Download

1 / 19

190 likes | 294 Views

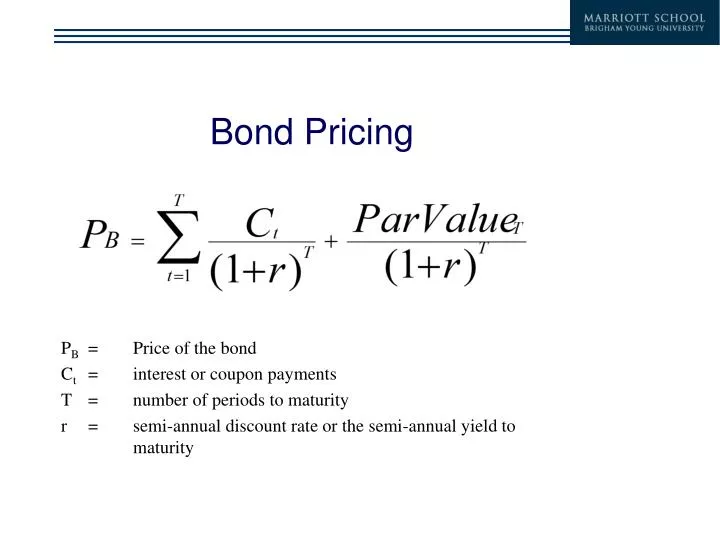

Bond Pricing. P B = Price of the bond C t = interest or coupon payments T = number of periods to maturity r = semi-annual discount rate or the semi-annual yield to maturity. Price of 8%, 10-yr. with yield at 6%. Coupon = 4%*1,000 = 40 (Semiannual) Discount Rate = 3% (Semiannual)

E N D

Bond Pricing PB = Price of the bond Ct = interest or coupon payments T = number of periods to maturity r = semi-annual discount rate or the semi-annual yield to maturity

Price of 8%, 10-yr. with yield at 6% Coupon = 4%*1,000 = 40 (Semiannual) Discount Rate = 3% (Semiannual) Maturity = 10 years or 20 periods Par (Face) Value = 1,000

Holding Period Return • What is the price of the bond in 6 months time (ex-coupon), and what was the holding period return over that time?

Premium and Discount Bonds • Premium Bond • Coupon rate exceeds yield to maturity • Bond price will decline to par over its maturity • Discount Bond • Yield to maturity exceeds coupon rate • Bond price will increase to par over its maturity

Prices and Yield to Maturity • YTM is discount rate that sets PV of bond cash flows equal to current market price Price Yield

Yield to Maturity Yield to maturity = interest rate that equates today’s value with present value of all future payments • Need Today’s Price or ‘Value’ to find implicit interest rate • Like Internal Rate of Return

Current YieldCoupon Bonds • Is better approximation to yield to maturity, nearer price is to par and longer is maturity of bond • Change in current yield always signals change in same direction as yield to maturity

Yield to Maturity Yield on a Discount Basis or Bank Discount Yield Yields on Discount Instruments Yield Measure Annualization

Alternative Measures of Yield • Yield to Call • Call price replaces par • Call date replaces maturity • Holding Period Yield (actual return) • Considers actual reinvestment of coupons • Considers any change in price if the bond is held less than its maturity • Realized Compound Yield • Reinvestment rate of coupons

Default Risk • Agency Assessment • Coverage ratios • Leverage ratios • Liquidity ratios • Profitability ratios • Cash flow to debt • Company’s Protection Against • Sinking funds • Subordination of future debt • Dividend restrictions • Collateral

Term Structure of Interest Rates • Relationship between yields to maturity and maturity • Yield curve - a graph of the yields on bonds relative to the number of years to maturity • Usually Treasury Bonds • Have to be similar risk or other factors would be influencing yields

Expectations Hypothesis Key Assumption: Bonds of different maturities are perfect substitutes Implication: Expected Return on bonds of different maturities are equal For n-period bond: yt + yt+1 + yt+2 + ... + yt+(n–1) ynt = n In words: Interest rate on long bond = average short rates expected to occur over life of long bond Numerical example: One-year interest rate over the next five years 5%, 6%, 7%, 8% and 9%: Interest rate on two-year bond: (5% + 6%)/2 = 5.5% Interest rate for five-year bond: (5% + 6% + 7% + 8% + 9%)/5 = 7% Interest rate for one to five year bonds: 5%, 5.5%, 6%, 6.5% and 7%.

Liquidity Premium Theory Key Assumption: Bonds of different maturities are substitutes, but are not perfect substitutes Implication: Modifies Expectations Theory with features of Segmented Markets Theory Investors prefer short rather than long bonds must be paid positive liquidity (term) premium, lnt, to hold long-term bonds Results in following modification of Expectations Theory yt + yet+1 + yet+2 + ... + yet+(n–1) ynt = + lnt n

Relationship Between the Liquidity Premium and Expectations Theories

Theories of Term Structure • Expectations • Long term rates are a function of expected future short term rates • Upward slope means that the market is expecting higher future short term rates • Downward slope means that the market is expecting lower future short term rates • Liquidity Preference • Upward bias over expectations • The observed long-term rate includes a risk premium

Innovations in the Bond Market • Reverse floaters • Asset-backed bonds • Pay-in-kind bonds • Catastrophe bonds • Indexed bonds • TIPS (Treasury Inflation Protected Securities)