Download

1 / 70

710 likes | 861 Views

Review of Bond Pricing. Fixed Income Securities. What are FI securities?. Financial claims issued by governments, government agencies, state governments, municipalities, corporations, banks, and other financial intermediaries They represent contract obligations of the issuers.

E N D

What are FI securities? • Financial claims issued by governments, government agencies, state governments, municipalities, corporations, banks, and other financial intermediaries • They represent contract obligations of the issuers. • E.g., bonds – principals, coupons • Also called debt securities

FI Markets • FI securities are issued, traded, and invested in markets that are called fixed-income markets • Representations: • Issuers • Financial intermediaries • investors

Issuers: Governments and their agencies Corporations State and municipalities Special purpose vehicles (SPV) Foreign institutions Intermediaries Primary dealers Other dealers Investment banks Credit agencies Credit and liquidity enhancers FI Markets

FI Markets: Investors • Governments • Pension funds • Insurance companies • Mutual funds • Commercial banks • Foreign institutions • House holders

FI: Terminology • Coupon, Principals, Time to maturity/term • Bid/Ask spread • Bullet security • With fixed maturity date and fixed coupons • Without options embedded • Debts with options • Callable / putable • convertible

Risks • Interest rate risk • Price of FI securities critically depends on the overall interest – price uncertain when one has to sell the debt security • Market risk • Reinvestment risk • Coupons are assumed to be reinvested and earn interest • Greater for longer holding periods

Risks: cont’d • Credit risk • FI securities are contract obligation for the issuer • Issuers may fail to pay the promised cashflow, which will lead to default • What will happen when default occur? • Important for low grade corporate bonds (or high yields/junk bonds)

Risks: cont’d • Inflation risk • Purchasing power risk • Reflected in the relative size of coupon rate and inflation rate • For some FIS, coupon is indexed to some consumer index • Timing risk • When it has callable feature • Very important for MBS

Risks: cont’d • Liquidity risk / Marketability risk • Reflected through bid/ask spread • Less important if plan to hold the security to maturity • FX risk • Volatility risk • Risk-risk

Classifications of FI Securities • US Treasury Securities • On-the-run vs off-the-run • T-bills, T-notes, T-bonds • Regularly issue 3m, 6m, 1y, 2y, 3y, 5y, 10y, and 30y bonds • Issued through auction • Discriminating prices • Uniform prices

Government bonds • Canadian government debt • Maturities range from 2 to 25 years • Issued through auction on yields • Gilt • Index linked gilt – both face value and coupons • Convertible gilts • Irredeemable gilts, or perpetual • Single price auction

Government bonds • JGB • 2, 5, and 10 years maturities • Callable • Part of the issue is underwritten by banks, insurance company and security firms. Remaining is by auction

Agency Securities • They are sponsored and backed by the government, but are usually privately owned • Examples • FHLB • Federal National Mortgage Association (Fannie Mae) • Federal Home Loan Mortgage Corp. (Freddie Mac) • Debentures and MBS • Student Loan Marketing Association (Sally Mae) • floaters

Corporate Debt Securities • Debt issued to raise capitals • Actively traded • Present credit risk • What will happen if default? • Usually rated by rating agencies • Usually carry coupons • Mandatory sinking funds • May have call features, or convertible features • High yields / junk bonds

Securitized Assets -- MBS Originator1 Pool of Mortgages Credit and liquidity Enhancements (guarantees) Originator1 SPV Originator1 MBS Credit rating agencies Intermediaries Institutional and retail investors

MBS Types • Pass-through securities • IOs • POs • High timing risk

Municipal Issues • General obligation bonds • Revenue bonds • Have default risks • Tax plays important roles in this type of bonds

Bond Characteristics • Face or par value • Coupon rate • Zero coupon bond • Compounding and payments • Indenture • Issuers

Provisions of Bonds • Secured or unsecured • Registered or bearer bonds (Canada) • Call provision • Convertible provision • Retractable and extendible (puttable) bonds • Floating rate bond

Discounting • Simple rate: • Time (expressed in years) is less than or equal to one year • Subject to different day count convention in different market • Annual rate: • y is called the annual rate • N is the number of years Wulin Suo

Compounding • Annual compounding • Semi-annual comp.: • Compounding m time a year • Continuous compounding: • FV vs PV Wulin Suo

Compounding … Wulin Suo

Rate Conversion Wulin Suo

Annuity • Pays same amount C in N consecutive periods • FV: • PV • PV for perpetuity Wulin Suo

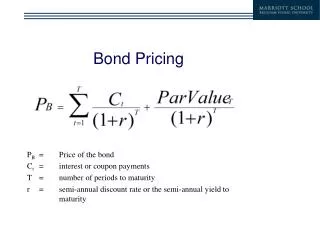

Yields (1) • Yield is the internal rate of return; also known as yield to maturity • Annual compounding: for a bond pays $C per year for N years, yield is defined as the y such that Wulin Suo

Yields (2) • Write the coupon as a percentage of face value: C=100c, • P <, =, or >100 if c<y, c=y, or c>y, respectively • Current yield: Wulin Suo

Yields: Semi-Annual • Notation: • C: total annual coupon • y: semi-annual compounding yield • P: price of the bond • N: number of coupons remaining • Premium, par, and discount • Also called bond equivalent yield Wulin Suo

Yields: m-Compounding • Compounding m-times a year, with N years remaining: • Continuous yield: Wulin Suo

Yields in Other forms • Yield to call • yield to 1st call, yield to 2nd call, etc • yield to put • Yield to par • Yield to worst: compute the yield to maturity, yield to call, and yield to put Wulin Suo

Cash Flow Yield • Amortizing securities: cash flow includes interest + principle prepayments (e.g., MBS/ABS) • CF yield: yield such that the PV of the projected cash flows equal to par Wulin Suo

Yield Measure for Floating Rate Securities • Coupon rate may change according to some reference rate • impossible to determine the future cash flow • Effective margin: a measure estimates the average spread or margin over the reference rate that the investor can expect to earn over the life of the security Wulin Suo

Floating Rate Securities … • How to compute the effective margin: • Step 1: Determine the CF assuming the reference rate does not change • Step 2: Select a margin (spread) • Step 3: Discount the CF in Step 1 by the current value of the reference rate plus the margin in Step 2 • Step 4: Compare PV in Step 4 with the price. Wulin Suo

Price for Treasuries • Day cont convention: • T-bill: Actual/360 • T-bill: • d is called the discount rate, or the quoted price Wulin Suo

T-Bills • d: annualized dollar return provided by the T-bill expressed as a percentage of the face value • Cash price P: • or • for the example, ask price • Discount rate is different from rate of return: • For the example, rate of return is 7.0877% Wulin Suo

Price T-Notes/Bonds • Price paid to buy the note/bond is different from those prices quoted: Invoice price = Quoted Price + Accrued Int • Invoice price is also called cash price, or dirty price • Quoted price: clean price • Day count convention for calculating accrued interest: Act/Act • Day Count convention • Actual/Actual (in period): Treasury Bonds • 30/360: Corporate Bonds • Actual/360: Money Market Instruments • Example Wulin Suo

Price T-Notes/Bonds • Compute accrued interest: • LCD: 15/05/91 • NCD: 15/11/91 • Total days between the coupon dates: 182 • Days between quote date and LCD: 32 • Accrued int: (8/2)x(32/182)=$0.7033 • Quoted bid price: 102.29=$102+29/32=102.9062 • Cash price (bid): 103.6720 Wulin Suo

Yields for T-Bills • For maturity n<182 days: • discount rate • relationship • example Wulin Suo

Yields for T-Bills … • For n>182 days • Assume a coupon is paid in 6 month’s time and interest is reinvested • at maturity: Wulin Suo

Yields for T-Notes/Bonds • If in the last coupon period: short government • accrued interest: • cash price is calculated as before • yield can be annualized as • in practice, yield is quoted as • price x S.D. MAT z LCD Wulin Suo

Yields for T-Notes/Bonds … • With more than one coupon left • if P is the invoice price, then yield is defined by • N is the number of remaining coupons Wulin Suo

Yield Curve • Graphical depiction of the relationship between the yields of the same credit and different maturities • Treasury yield curve is the benchmark • very liquid • Should not be used to price a bond • sometime bonds with similar maturities carry very different coupons • not appropriate to discount all cash flows by the same rate • should treat the bond’s each cash flow separately Wulin Suo

Default Risk and Ratings • Rating companies • Moody’s Investor Service • Standard & Poor’s • Canadian Bond Rating Service (CBRS) • Rating Categories • Investment grade • Speculative grade

Factors Used by Rating Companies • Coverage ratios • Leverage ratio • Liquidity ratios • Profitability ratios • Cash flow to debt

Protection Against Default • Sinking funds • Subordination of future debt • Dividend restrictions • Collateral

Managing interest rate risk • Bond price risk • Coupon reinvestment rate risk • Matching maturities to needs • The concept of duration • Duration-based strategies • Controlling interest rate risk with derivatives