Download

1 / 47

470 likes | 505 Views

Learn about negative amortization loans through examples, calculations, and insights. Explore compound interest, discounting, and effective annual interest rates. Get to grips with complex financial concepts in an accessible way.

E N D

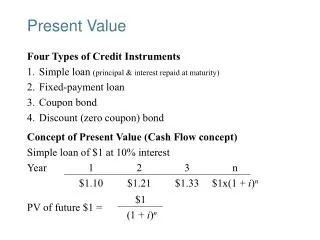

More on present value analysis How do we discount multiple times within the same year? More tools for the building-for-sale example

Warm up application: Negative amortization loans • Good for… • Cyclical jobs • When there are good investment opportunities • Be careful to think about risk here • Why aren’t there many Neg Am loans out there? • “Underwater”

Negative amortization loans:An example • $80,000 loan on a house valued at $100,000 • Stated annual interest rate is 6%, compounded monthly • 0.5% per month • Minimum payment required per month is 0.3% of the loan • Notice that the minimum payment (0.3%) is less than the monthly interest rate (0.5%)

Negative amortization loans:An example • The first month’s interest • $80,000 0.005 = $400 • The first month’s minimum payment • $80,000 0.003 = $240 • The minimum payment adds $160 to the principal after the first month • New balance is $80,160

Negative amortization loans:An example • The second month’s interest • $80,160 0.005 = $400.80 • The second month’s minimum payment • $80,160 0.003 = $240.28 • New balance after 2 months: $80,320.52 • Notice that the balance is increasing at an increasing rate When does the bank get its money back?

Main goals for today • We want to continue our understanding of interest and discounting • There are many subtleties that we need to know how to deal with

Recall:Our building-for-sale example • In the real world, we may get much more complicated offers for the building • $40,000 per year in years 0-2 • $21,000 every six months in years 0-2 • $15,000 per year in years 0-14 • $12,000 per year forever, starting in year 0 • $5,900 every six months forever, with the first two payments in year 0 • Assume that r = 10%

Recall: Compounding interest over a long period time matters… a lot • The difference for 3 years between compound interest & simple interest • 3r 2 + r3 is 0.031, or 3.1%, when r = 10% • The difference between the two methods gets bigger very fast as the number of years grows • 1% difference with two years compounding (left to student to figure) • 6.41% for four years (left to student to figure) • 59.37% for 10 years (left to student to figure)

What if we compound interest more than once a year? • Banks typically compound interest for loans and deposits on a monthly or daily basis • How does it do it? • If annual interest rate is r, then monthly interest rate is r /12 and daily rate is r /365 in a non-leap year • Notice that interest within the same year is compounded when this happens • Without any repayment, $100 loaned today leads to an amount owed one year from now of… • …$100 (1 +0.01)12 = $112.68

EAIR • The effective annual interest rate (EAIR) is the annual rate of return once compounding has been accounted for • Also sometimes referred to as EAR or APY • When $100 turns into $112.68 a year from now, the EAR is 12.68% • How many of you did this? • Recall that the stated annual interest rate (SAIR) is 12% (or 1% per month) • SAIR is also sometimes referred to as SAR or APR

Can we reach annual interest rate of infinity? • Can we compound more and more frequently to get an EAR of infinity? • No • The use of limits tells us what the greatest EAR is, given a SAIR • Continuous compounding

Exponential functions • If we continued to increase the frequency of compounding forever, we eventually get to “continuous” compounding • If exp(·) represents the exponential function, then Note: exp(1), or e1, is about 2.718

Back to the building problem • What is the present value of the following payment streams? • $40,000 per year in years 0-2 • $21,000 every six months in years 0-2

$40,000 per year in years 0-2 • $40,000 in year 0 has a PV of… • $40,000 (no discounting) • $40,000 in year 1 has a PV of… • $40,000/(1.1) = $36,363.64 • $40,000 in year 2 has a PV of… • $40,000/(1.1)2 = $33,057.85 • Total PV for 3 payments: $109,421.49

What is our discount rate every six months here? • We need to figure out the discount rate every six months to get an effective annual rate of 10% per year • Square root of 1.1 is 1.0488 • When compounding every six months, we must use a stated discount rate of 4.88% every six months • Essentially, a stated annual interest rate of 9.76% if we are compounding twice per year, compounded twice a year, with an effective annual interest rate of 10% Good article to read if you are still confused: http://www.investopedia.com/articles/basics/04/102904.asp#axzz1n3HpdCmr

We want the effective rate to be 10% per year • When compounding every six months, we must use a discount rate of 4.88% every six months • Essentially, a stated annual interest rate of 9.76% if we are compounding twice per year, with an effective annual interest rate of 10% • We need the effective rate to be the same for all calculations or else we do not have correct calculations for comparison

$21,000 every six months in years 0-2 • PV of six payments (try this on your own) • $21,000 • $20,022.71 • $19,090.91 • $18,202.47 • $17,355.37 • $16,547.70 • Total PV of six payments: $112,219.16

Which to choose? • If we could only receive $40,000 per year in years 0-2 or $21,000 every six months in years 0-2, which would we choose? • The latter • $112,219.16 > $109,421.49

Are there shortcut formulas to help with the other offers? • Yes, given a constant percentage rate of increase or decrease • Perpetuities • A payment stream that goes on forever • Annuities • A payment stream that has a finite end date

Perpetuities • Sometimes, an asset can offer a stream of cash flows forever • Example: A bond that pays $100 per year forever • How much is this stream of cash flows worth? • Is it infinite?

Perpetuities • If someone receives C dollars each year forever (starting one year from now), the present value (PV) is • PV = C / r • Intuition? Recall that we assume a discount rate r

Example • Mrs. Jones is set to receive $5,000 per year from Crowes, Inc., starting next year • Her discount rate is 8% • How much is the present value of this stream of payments? • PV = $5,000 / 0.08 = $62,500 What if first payment is made today?

Growing perpetuity • Sometimes, perpetuities are more complicated • The annual payment starts at C, but increases by fraction g each subsequent period • Example of growing perpetuity • First payment in one year is $100, and increases by 3% each year • Here, g = 3% = 0.03

Growing perpetuity • Similar to a regular annuity, a growing annuity’s present value can generally be expressed as • PV = C / (r – g) if r > g • What if r is not greater than g?

Example • Charlie Scream is due to earn $50,000 in royalties next year • Every year thereafter, the amount of royalty payments increases by 20% • Charlie’s yearly discount rate is 25% • How much is this stream of payments worth? • Plug into PV = C / (r – g)

Annuities:Like perpetuities? • An annuity is a constant stream of payments made for a fixed time period • Example: The CA lottery has a game in which you can be “Set For Life” with a top prize is $100,000 per year for 20 years • How can we easily figure out how much this is worth? • Assume in this case that the first payment is made in one year

How to figure out how much an annuity is worth • We can calculate how much the 20 payments are worth by taking the difference of the following two values • Payments in year 1 (one year from now) to infinity • A perpetuity worth $1.25 million in PV terms • Payments in years 21 to infinity • A perpetuity that we have to discount by 20 years • $1.25 million, divided by 1.0820, or $268,165 Assume r = 0.08 in this example

Formula for PV of annuity • The general form of what we did on the last slide is

Alternate ways for PV of an annuity or The term in brackets is often referred to as the “annuity factor”

Growing annuity • Finite number of payments that grows each year at growth rate g

Back to payment streams • In the real world, we may get much more complicated offers for the building • $40,000 per year in years 0-2 • $21,000 every six months in years 0-2 • $15,000 per year in years 0-14 • $12,000 per year forever, starting in year 0 • $5,900 every six months forever, with the first two payments in year 0 We will analyze these payment streams now We will also analyze this payment stream, but pay careful attention

$15,000 per year in years 0-14 • Annuity (starting in year 1) with an additional payment in year 0 • Recall r = 0.1 • PV = 15,000 + • PV = $125,500.31

$12,000 per year forever, starting in year 0 • Perpetuity (starting in year 1) with an additional payment in year 0 • PV = C + C / r = 12,000 + 12,000 / 0.1 • PV = $132,000

$5,900 every 6 months forever, with the first two payments in year 0 • Recall: Square root of 1.1 is 1.0488 • PV of two payments in year 0 • 5,900 + 5,900 / 1.0488 = 11,525.48 • Payment of $5,900 at the beginning of the year and a payment of $5,900 six months later is equivalent to a single payment of $11,525.48 at the beginning of the year

$5,900 every 6 months forever, with the first two payments in year 0 • We will now treat this problem as equivalent to a payment of $11,525.48 per year forever (starting in year 0) • PV = $11,525.48 + $11,525.48 / 0.1 • PV = $126,780.28

Determining the best offer to accept for the building • $40,000 per year in years 0-2 • PV = $109,421.49 • $21,000 every six months in years 0-2 • PV = $112,219.16 • $15,000 per year in years 0-14 • PV = $125,500.31 • $12,000 per year forever, starting in year 0 • PV = $132,000 • $5,900 every six months forever, with the first two payments in year 0 • PV = $126,780.28

Four types of loans to consider Unless mentioned otherwise, assume that the payments are made yearly in these examples Principal reduced by the same amount each year Payments are the same each year Loans with a “balloon” payment Negative amortization loans We started looking at this earlier Loan amortization

Principal paid back is the same each year • Simple to calculate for a T year loan • Pay 1 /T of the principal each year • Example: $3,000 loan to be paid back over 3 years, r = 20% • Let’s do this on the board

Payments are the same each year • Many loans you will receive from banks will require you to pay back the same amount of money each month • Personal loans • Mortgages • If you loan more than 80% of the value of the house, you may also need to pay private mortgage insurance (PMI) until you have 20% equity in the house

Example: $3,000 loan, paid back over 3 years, r = 20% • We have to figure out how a stream of payments will be worth $3,000 today • Annuity formula: • Plug in values that we know • PV = $3,000 • r = 0.2 • T = 3 • Annuity factor: 2.10648 • C = $1,424.18 Recall: The term in brackets is often referred to as the annuity factor

Loan with a “balloon” payment • Some loans will let you pay less than the amount required to reach a zero balance at the end of the loan • The extra amount is a “balloon” payment that is due at the end of the loan • A new loan is often made to pay off the “balloon” payment • How do we do this?

Example: $3,000 loan, paid back over 3 years, r = 20% • Partial amortization loan • Some of the principal gets paid back • In this case, we assume a 10-year amortization • If we paid all of the principal back over 10 years, we would need to pay $715.57 per year (calculation left to student) • What is the balloon payment after 3 years? • Note: The balloon payment is the payment that is made above the regular payment

Pay $715.57 per year Year 1 Pay $715.57 $600 in interest Reduce principal by $115.57 New balance is $2884.43 Year 2 $576.89 in interest Reduce principal by $138.68 New balance is $2745.75 Year 3 New balance is $2579.33 Example: $3,000 loan, paid back over 3 years, r = 20%

Example: $3,000 loan, paid back over 3 years, r = 20% • 3-year loan based on a 10-year amortization • Yearly payment of $715.57 • An additional $2,579.33 is due at the end of three years (balloon payment) • Reminder: Unless mentioned otherwise, the balloon payment is defined for this class as the amount ABOVE the regular payment that is made at the end of the loan • We also have an alternate way of calculating the balloon payment

Balloon payment calculation • We can calculate how much the remaining payments are worth three years from now, using the annuity formula • We calculate the value in “Year 3” dollars • Loan balance = $715.57 [1 – (1/1.27)]/0.2 = $715.57 3.60459 = $2579.34 We are off by a penny due to rounding of yearly payment