Download

1 / 5

70 likes | 292 Views

SAVINGS. CORPORATE SAVINGS IMPACTED BY ECONOMIC EXPECTATIONS SAVINGS FOR EXPANSION/ACQUISITIONS POSIBILITY OF LABOR/MATERIAL DISRUPTION POLITICAL UNCERTAINTIES INFLATION/DEFLATION EXPECTATIONS ECONOMIC CYCLES INDIVIDUAL SAVINGS IMPACTED BY LIFE STAGE PATTERN FORMATIVE/EDUCATION DEVELOPING

E N D

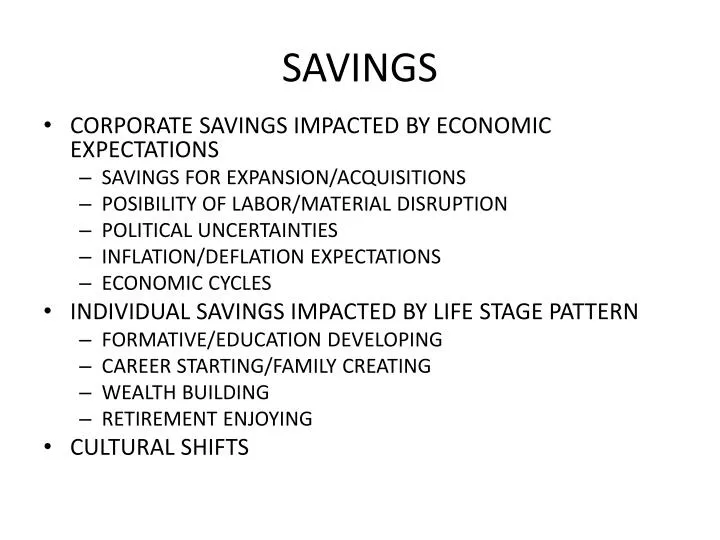

SAVINGS • CORPORATE SAVINGS IMPACTED BY ECONOMIC EXPECTATIONS • SAVINGS FOR EXPANSION/ACQUISITIONS • POSIBILITY OF LABOR/MATERIAL DISRUPTION • POLITICAL UNCERTAINTIES • INFLATION/DEFLATION EXPECTATIONS • ECONOMIC CYCLES • INDIVIDUAL SAVINGS IMPACTED BY LIFE STAGE PATTERN • FORMATIVE/EDUCATION DEVELOPING • CAREER STARTING/FAMILY CREATING • WEALTH BUILDING • RETIREMENT ENJOYING • CULTURAL SHIFTS

INTEREST RATES • LOANABLE FUNDS THEORY—INTEREST RATES ARE A FUNCTION OF THE SUPPLY AND DEMAND FOR LOANABLE FUNDS • SUPPLY INCREASE, DEMAND STABLE, INTEREST RATES GO DOWN • SUPPLY DECREASE, DEMAND STABLE, INTEREST RATES GO UP • DEMAND INCREASE, SUPPLY STABLE, INTEREST RATES GO UP • DEMAND DECREASE, SUPPLY STABLE, INTEREST RATES GO DOWN

FACTORS AFFECTING SUPPLY OF LOANABLE FUNDS • INCOME LEVEL—HIGH INCOME-HIGH SAVINGS, LOW INCOME-LOW SAVINGS • INCOME TAXES • AGE OF POPULATION • RESPONSE TO INTEREST RATES • U. S. TREASURY ACTIVITIES • FED ACTIONS • INTERNATIONAL FACTORS

INTEREST RATE TERMINOLOGY • NOMINAL INTEREST RATE (r)—MARKET INTEREST RATE • REAL RATE OF INTEREST (RR)—RISK-FREE RATE WITH NO INFLATION EXPECTED • INFLATION PREMIUM(IP)—AVERAGE INFLALATION RATE EXPECTED OVER THE LIFE OF THE LOAN • DEFAULT RISK PREMIUM (DRP)—COMPENSATION FOR RISK OF NON-PAYMENT • MATURITY RISK PREMIUM (MRP)—ADDED RETURN TO COMPENSATE FOR OPPORTUNITY COST OF POSSIBLE FUTURE INTEREST RATE INCREASES • LIQUIDITY PREMIUM (LP)—ADDED RETURN IF DEBT INSTRUMENT IS NOT EASILY TURNED INTO CASH

r = RR + IP + DRP + MRP + LP • RISK-FREE RATE OF INTEREST—INTEREST APPLICABLE TO THE U.S. TREASURY DEBT INSTRUMENTS • TERM STRUCTURE (YIELD CURVE)—RELATIONSHIP BETWEEN INTEREST RATES (YIELDS) AND MATURITY OF COMPARABLE QUALITY DEBT INSTRUMENTS • EXPECTATIONS THEORY—SHAPE OF YIELD CURVE REFLECTS INVESTOR EXPECTATIONS ABOUT FUTURE INFLATION RATES • LIQUIDITY PREFERENCE THEORY—INVESTORS PREFER TO INVEST SHORT TERM FOR GREATER LIQUIDITY AND LESS MATURITY RISK • MARKET SEGREGATION THEORY—DIFFERENT DEMANDS OF INVESTORS IN EACH MARKET SEGMENT AFFECTS THE SHAPE OF THE YIELD CURVE