Download

1 / 14

140 likes | 401 Views

Enclosure 10 Trust Board Meeting – 25th March 2010 FINANCE REPORT for the period ending 28th February 2010 (Month 11). Section One- EXECUTIVE SUMMARY. Section Two - Forecast Outturn based on Month 11 YTD Performance.

E N D

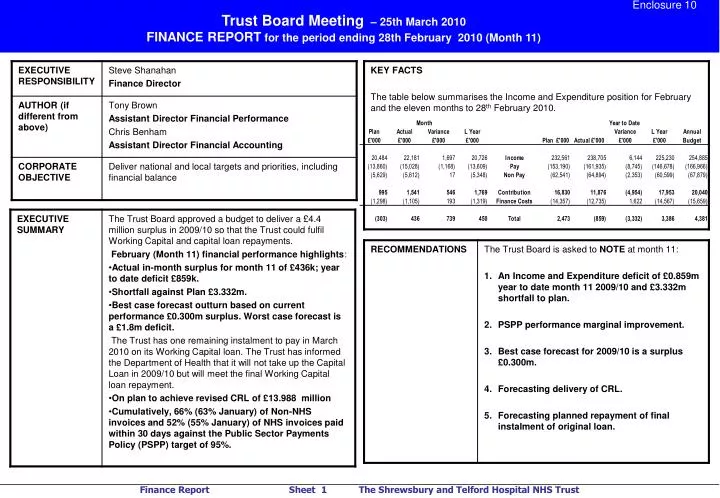

Enclosure 10 Trust Board Meeting – 25th March 2010 FINANCE REPORT for the period ending 28th February 2010 (Month 11)

Section Two - Forecast Outturn based on Month 11 YTD Performance • The initial planned I&E surplus of £4.4m was revised following SHA discussions around loan requirements at month 6 to £4.3m. It is anticipated that the planned working capital loan repayment will be made in March 2010 • The table opposite shows the Best and Worst case forecasts for the year. The columns to the left represent the forecast £300k surplus reported at month 8. The columns to the right show the months 9,10 and 11performance against forecast and the revised forecast £300k incorporating the additional SHA support. Best Case : • Improving Income run rate due to emergency activity and additional SHA support in respect of EWTD rota compliance, Hospital at Night and innovation investment expenditure. • Pay run rate reflects reduced agency reliance, vacancy management and Divisional working arrangement changes but no reduction in Month 12. • No 2009/10 spend on additional A&E Consultants. Earliest start dates 2010/11 • Additional 28 beds at PRH at an additional cost of £300k. Therapies weekend working at an additional cost of £60k. • Non Pay spend reduction due to strict management of requisitions and non accountable stock control measures Worst Case : • Income at c.£21.5m for Month 12 • Pay run rate increases to £15.3m in Month 12 • Non pay run rate does not reduce below £6.0m Both Cases : • Deferral of return of the £1.8m 2007/08 tariff support to SHA. • MEA revaluation of assets giving £1.0million depreciation charge gain 2009/10. • Current Improvement Programme run rates continue, to give £6.5m forecast. KEY RISKS: • Reliance on Divisional expenditure and commitment management. • Management of waiting list cost pressures within income constraints and baselines • Achieving required income levels.

Section Three – Expenditure - Pay • Pay expenditure continues to exceed plan. Best case forecast now assumes continuation of February run rate due to expected increase in reliance on agency as a consequence of escalation in early March. • Month 11 run rate includes new ward at PRH, costs £75k • Waiting list payments in February were £264k (£2,908k YTD) • In February agency costs have reduced to £0.6m,an improvement of £0.3m on the month 10 spend. This is equivalent to 96 wte, in January agency was equivalent to 141 wte. The in month agency spend per wte of £6,521 is above the month 10 average of £5,787 – a reflection of the switch in spend to medical staffing. • Medical staff agency cover costs have reduced in February to £286k (£362k in January). As previously reported this is due to the need to cover rota gaps to ensure EWTD compliance. • The nursing agency spend in February was £176k, a reduction on the January levels and the number of shifts filled by agency was 474(January 1,052).

Section Four - Cash • Closing cash balance £317,000, this is an increase of £84,000 on the prior month balance and £74,000 higher than plan. • EBITDA shortfalls continue to be managed through creditor payments within working capital and capital expenditure. • The Trust is working with the SHA to (i) understand the historical working capital loan drawdown and (ii) assisting in accelerating cash allocations from the local PCT’s to improve the BPPC. • Revised forecasting procedures are in place and will be closely managed to ensure sufficient cash is available towards the latter part of the calendar year, last quarter of 2009/10 and first quarter of 2010/11 – this is due to (i) the completion and timing of large capital projects (including decontamination offsite solution) and (ii) the second tranche of loan and dividend obligations.

Section Five - Improvement Programme • A more detailed report is presented monthly to the Finance & Performance Committee. • The September reforecast of the CIP gave a forecast outturn of £7.2m. Taking into consideration YTD CIP run rate the current forecast outturn is £6.5m. • IP target for 2009/10 was £10.4 million (original FIMs plan submission £10.65 million). • For the year to month 11 the Trust achieved 69% of its planned Improvement Programme (IP)

Section Six - Financial Risk Rating • At month 11 the risk rating remains at 2. The in month surplus has improved performance against all criteria when compared to month 10. • The cumulative deficit and shortfall to plan continue to adversely affect the financial performance criteria. • There has been a slight improvement in the cash balance at Month 11, however the overspend continues to affect cash and other working capital balances. • The table opposite summarises anticipated performance against our NHS Trust Statutory and Departmental financial duties. • Surplus forecast remains at £0.3m • Impact of I & E performance on cash management and consequence ability to meet BPPC targets.

Section Seven – Activity and Income The graphs below detail the 2009/10 activity against plan and 2008/09 actual levels for each activity type. • Total elective and day case activity is 54 spells/£287k above plan in February. Cumulatively activity is 1,839 spells below plan, the income shortfall is £858k. Activity is above 2008/09 levels. • Day case activity was 33 spells above plan in February with a £184k surplus. • Day case activity for General Surgery, Ophthalmology, Gastroenterology and Anaesthetics were above plan in the month. • Non elective activity is 90 spells above plan in the month and cumulatively 717 spells (£3,074k) over plan, which is above previous year’s levels. • Maternity activity is below plan 80 spells in month and 267 spells YTD below plan. Planned growth was 7.2% on last years outturn, actual activity is 95.8% of plan

Section Seven – Activity and Income • Outpatient attendances continue above plan for February and the year to date. • In February new outpatients are 1,048 attendances above profile (6,543 YTD). • Follow up outpatients are 1,218 attendances above plan in February (4,358 YTD). • Outpatient income shows a £1,419k YTD over performance. • Included within the New Outpatient attendances are Outpatients Procedures which show 230 attendances over performance in February (1,567 YTD) • A & E attendances are 237 below plan in February, (926 above plan YTD). • Cumulatively income is £496k (6.6%) above plan. • Year to date activity analysis shows RSH 50.7% and PRH 49.3%, income shows a near 50/50 split.

Section Eight- Expenditure – Non-Pay and Finance Costs • Non pay shows a £17k under spend in month; £2.3 million over spend Year-to-date (YTD). • The key contributing factors YTD are as follows • Activity outsourced to private providers to maintain 18 week waiting times • Overhead recharges from RJAH in respect of orthotics services. • Drugs outside PbR tariff offset by income over recovery • Developing Health and Healthcare contribution • All non-clinical non-pay expenditure requisitions continue to be reviewed and scrutinised for validity and necessity before being approved. • This review has highlighted areas where standardisation of non-clinical spend items and restriction of catalogue choice will reduce expenditure levels. These restrictions will be actioned as appropriate. • The spend to Month 11 now includes non-recurring gains from goods received reviews and IT capitalisations • Finance costs are £193k under spent in February (£1,622k YTD). This is due to a reduction in the depreciation charge (£1,266k YTD) as a result of the revaluation of assets on a Modern Equivalent Asset (MEA) basis at month 6

Section Nine - Debtors • Total trade debtors have decreased by £1,063,000 compared to prior month. • All categories have decreased with current reducing by £288,000, +30 day category reducing by £320,000 and +60 day category reducing by £455,000 • The outcome of the arbitration with Shropshire County PCT is not reflected within the trade debtor positions. • Shropshire County PCT have settled some elements of current and +30 days, but a small increase of £7,000 has been seen within the +60 days category. The outcome of the arbitration with Shropshire County PCT is not reflected within the trade debtor positions. • Telford and Wrekin PCT have settled £519,107 of the September 2009 dated over-activity invoice. The outstanding balance of £49,460 relates to a tariff dispute for planned same day (PSD) elective work. • Following the intervention at Finance Director level a further, significant reduction has been seen within the position of RJAH. • Danwood debtor relates to the Trust’s printing management contract and will be partially offset by an outstanding creditor. • Of the other debtors outstanding £30,000 has been referred to a specialist collection agency with appropriate provisions for write off made based on expected collection success. • £56,000 in respect of an overseas visitor with no means to pay is shown in line with DH guidance – this debtor has been provided for in full.

Section Ten – Creditors (Non NHS) • The table and graph summarise the non-NHS creditor payment performance for the month 11, month and year to date position. • The Better Payment Practice Code stipulates a target of 30 days. • Compliance remains as last month with the Trust continuing to try to prioritise non-NHS payments. The current cumulative compliance position is 66% for volume and 64% for value.

Section Ten – Creditors (NHS) • The table and graph summarise the NHS creditor payment performance for month 11, and the year to date position. • The Better Payment Practice Code stipulates a target of 30 days. • Compliance remains as last month and whilst the Trust continues to try to prioritise non-NHS payments significant pressure is being felt by certain NHS bodies (NHSLA and NHS Supply Chain).The current cumulative compliance position is 52% for volume and 35% for value.

Section Eleven - Capital • Revised CRL remains at £13.988 million. • In month spend of £1,229,000 brings year to date spend to £8,244,000. • £869,000 has been under spent across the capital schemes. This has been re-allocated to other capital schemes to achieve our CRL. • Pharmacy Aseptic unit build handover took place on 22 January 2010. A 3-4 month commissioning and validation process is required before a phased transfer of services can start. • Paediatric outpatient department, new 28 bedded ward at PRH and MAU move – completed as planned. • Decontamination offsite solution to be completed by end of August 2010, with operational services planned to commence January 2011. • The Maternity Project Board are reviewing the scope of the project of the redevelopment of Women and Children’s Zone. • Privacy and dignity screens and windows completed..