Download

1 / 28

280 likes | 300 Views

July 14, 2000. Confidential & Proprietary. Internal Presentation NewCo Overview. Table of Contents. 1. Executive Summary 2. Existing Asset Profile and Development Pipeline 3. Financial Summary 4. Next Steps. 1. Executive Summary. Executive Summary. Mission Statement.

E N D

July 14, 2000 Confidential & Proprietary Internal Presentation NewCo Overview

Table of Contents 1. Executive Summary 2. Existing Asset Profile and Development Pipeline 3. Financial Summary 4. Next Steps

Executive Summary Mission Statement • To establish the premier North American energy company involved in the businesses of: • Development, acquisition, ownership, and operation of electric power generation facilities • Optimization of generation portfolio through active risk management of assets and commodity positions

World Class CapabilitiesENA FPLE NewCo National power/gas trading, risk management Trading technology Construction and development backlog Existing asset base Management/lead sponsorship Operations Executive Summary Keys to Success World Class GENCO + ENA FPLE

Executive Summary Business Model • Combine physical and intellectual assets from FPL Energy (“FPLE”) and Enron North America (“ENA”) • Rapid growth through greenfield development utilizing combustion turbine position • Employ Enron’s model for risk management and trading • Supplement growth by pursuing strategic acquisitions • Retain, attract and grow intellectual capital • Leverage sponsors’ expertise to supplement NewCo resources 20,000+ MW by 2005

Executive Summary NewCo’s Growth Story Target five year EPS compounded annual growth rate of 25-30% Net Income 5-yr.CAGR 31%

Executive Summary Transaction Overview ENRON FPL Energy Operating Assets (3,094 MW) Advanced Development (1,423MW) Up to 6 Turbines (300 MW) 24 Development Sites People Development ROFR Three-year Toll Temporary Credit Support Operating Assets (3,881 MW) Advanced Development (3,905 MW) 31 Unallocated CTs (7,750 MW) 10 Development Sites People Development ROFR Temporary Credit Support $/Note/Equity Services Agreements Fuel/Power ROFR $ Shares NEWCO INVESTORS Debt Holders Notes $

Executive Summary Capability Sources ENA FPLE New Hires Outsource Comments Executive Management A A B - - Development AA B - - Power/Gas Trading, Risk Management A B C B ENA Back-office support Asset Management - A B - - Operations B A B B FPLE to supplement Finance A A B - - Technical Support C A - B FPLE to supplement Construction Management A A B B FPLE to supplement Legal B B B A - Information Management B B B A FPLE & ENA to supplement Human Resources B B A A FPLE to supplement Note: Primary Source = A, Secondary Source = B, Tertiary Source = C

Enron Unparalleled capabilities in power and gas trading, marketing and risk management Most Innovative Company - five years in a row (Fortune Magazine) FPL World class operator and manager of generation facilities Competitive development infrastructure that includes commercial talent, identified sites and secured equipment Executive Summary Parent Company Sponsorship Benefits • Realize value in unregulated generation businesses • Accelerate the attainment of critical mass • Diversify generation portfolio mix • Complement existing competencies • New investor base

Executive Summary Domestic Portfolio Comparables

Executive Summary Comparable Stock Prices Current P/E Forward P/E* Calpine 76.51 58.31 Dynegy 60.60 29.78 AES 43.37 33.63 Enron 57.50 51.16 FPL 13.04 12.13 * Source: Bloomberg as of July, 12, 2000

Existing Asset Profile and Development Pipeline Company Profile • National generation company that initially has: • 6,975 MW of net operating capacity in all nine NERC regions • 5,328 MW in late stages of development (2001-2003) • 7,750 MW in turbine queue spots (2003-2004) • 20,053 MW of total capacity by 2005 • NewCo embodies: • ENA’s trading, marketing and risk management expertise • FPL Energy’s development, operational and asset management expertise

Maine Assets: Hydro Units (373) Yarmouth (654) Wiscasset (101) Fort Fairfield (31) Total = 1,159 MW MAPP NPCC MAAC WSCC MAIN ECAR SPP MAAC Assets: Sayreville, NJ (150) Delaware Co, PA (50) CA Assets: Harper Lake (80) Altamont Pass (161) Tehachapi (180) Total = 421 MW SERC ERCOT Existing Asset Profile and Development Pipeline NewCo’s Existing Assets (6,975 Net Operating MW) Helix, OR (25) Lake Benton, MN (104) Clear Lake, IA (42) Bellingham, MA (150) Manhattan, IL (656) Ashland, VA (665) Wheatland, IN (508) Gleason, TN (536) Gaffney, SC (50) Brownsville, TN (494) New Albany, MS (396) Paris, TX (990) Caledonia, MS (504) McCamey, TX (75) NewCo Fuels Natural Gas (62%) Wind (7%) Oil (23%) Hydro (6%) Wood (1%) Solar (1%)

Existing Asset Profile and Development Pipeline NewCo’s Existing Assets

Existing Asset Profile and Development Pipeline Development Assets • Major Equipment Secured • 47 GE 7FA and up to 6 LM 6000 combustion turbines (11,750 MW combined cycle capacity) • GE 7FA ship dates: 2001 (9), 2002 (14), 2003 (12), and 2004 (12) • LM 6000 ship date: 2001 • FPLE to contribute executed master steam turbine agreement; HRSG agreement is executed • Substantial Development Talent • Forty-five (45) (30-FPLE/15-ENA) developers working in all NERC regions • ENA and FPLE possess complementary regional staffing • Parent company to commit technical expertise

Existing Asset Profile and Development Pipeline Development Pipeline • Advanced Development Projects (5,328 MW) • ENA controls three projects totaling 1,423 MW in operation by 2003 • FPLE controls ten projects totaling 3,905 MW in operation by 2003 • Very high probability of success • Thirty-four (34) Greenfield Sites • ENA controls 24 sites • FPLE controls 10 sites • Development Acquisition (15,000 MW) • FPLE is actively pursuing acquiring greenfield sites and third party development rights

MAPP NPCC MAAC WSCC MAIN ECAR SPP MAAC Assets: Marcus Hook, PA (750) Philadelphia, PA (750) SERC ERCOT Existing Asset Profile and Development Pipeline Development Asset Location Everett, WA (500) Bellingham, MA (500) Sarnia, ON (453) Providence, RI (500) Ashland, VA (170) Pastoria, CA (750) Las Vegas, NV (270) Bastrop, TX (250) Greenfield Sites SERC - 7 Sites ECAR - 2 Sites SPP - 6 Sites MAIN - 3 Sites WSCC - 9 Sites Nepool - 2 Sites PJM - 3 Sites ERCOT - 2 Sites Development Assets (MW) In Operation: 976 MW (2001)* In Operation: 2,520 MW (2002)* In Operation: 1,498 MW (2003)* * 485 MW in Wind Assets to come on line in 2001.* Additional 1,700 MW in queue spots for 2002.* Additional 6,000 MW in queue spots for 2003 & 2004.

Existing Asset Profile and Development Pipeline Portfolio Breakdown

Financial Summary Five Year Proforma (Millions) 2001 2002 2003 2004 2005 Existing Assets EBITDA $ 541 $ 499 $ 505 $ 560 $ 572 Net Income $ 106 $ 94 $ 111 $ 166 $ 197 After-Tax Cash Flow $ 180 $ 156 $ 168 $ 292 $ 316 Existing Assets with Development Pipeline EBITDA $ 561 $ 718 $1,010 $1,338 $1,597 Net Income $ 133 $ 159 $ 200 $ 305 $ 389 After-Tax Cash Flow $ 206 $ 253 $ 300 $ 487 $ 547

Financial Summary Valuation Summary (Millions) *Prior to IPO

Financial Summary Debt Financing ENA Tranche 1 Tranche 2 Tranche 3 Total Amount (MM) $ 50 $ 210 $ 475 $ 735 Term (yrs) 3 10 20 Treasury Rate 6.80% 6.50% 6.20% 6.33% Spread2.25% 4.50% 5.00% 4.67% All-in Coupon Rate 9.05% 11.00% 11.20% 11.00% FPLE Merchant Assets Contract Assets Total Amount (MM) $ 659 $ 875 $ 1,534 Term (yrs) 20 20 Treasury Rate 6.50% 6.20% 6.33% Spread3.00% 2.50% 2.72% All-in Coupon Rate 9.50% 8.70% 9.04%

Financial Summary Capital Requirements (Millions) • 2001 2002 2003 2004 2005 • Capital Expenditures ($ 193) ($ 1,524) ($ 2,488) ($ 1,650) ($ 1,650) • Cash Flow from Operations $206 $ 253 $ 300 $ 487 $ 547 • Debt Proceeds $135 $ 960 $ 1,851 $ 1,163 $ 1,155 • IPO Proceeds $500 • Net Capital Sources/(Uses) $ 148 ($ 311) ($ 337) $ 0 $ 52 • Cumulative Capital $ 648 $ 337 $ 0 $ 0 $ 52 Capital needs funded from internally generated cash, debt and IPO proceeds

Next Steps Issues • Transaction Terms • Development non-compete • Fuel/Power ROFR • Valuation • Support services agreements • Non-core assets • Wind assets • NewCo headquarters location • Schedule • Negotiation, documentation and due diligence • FERC filing schedule • Transaction schedule • Investment Bank Feedback • Use of proceeds • JV formation and IPO timing • Historical operating and financial information • Target debt rating

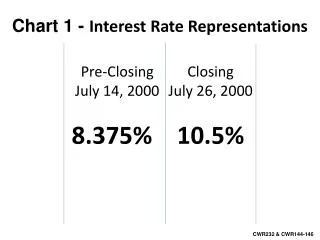

Next Steps Schedule Public Holidays