Download

1 / 19

190 likes | 206 Views

A deliberate and continuing process to achieve the financial goals of the client, including cash flow planning, tax planning, retirement planning, estate planning, and asset allocation. This report analyzes the client's current financial situation, sets quantifiable goals, and outlines strategies to achieve those goals.

E N D

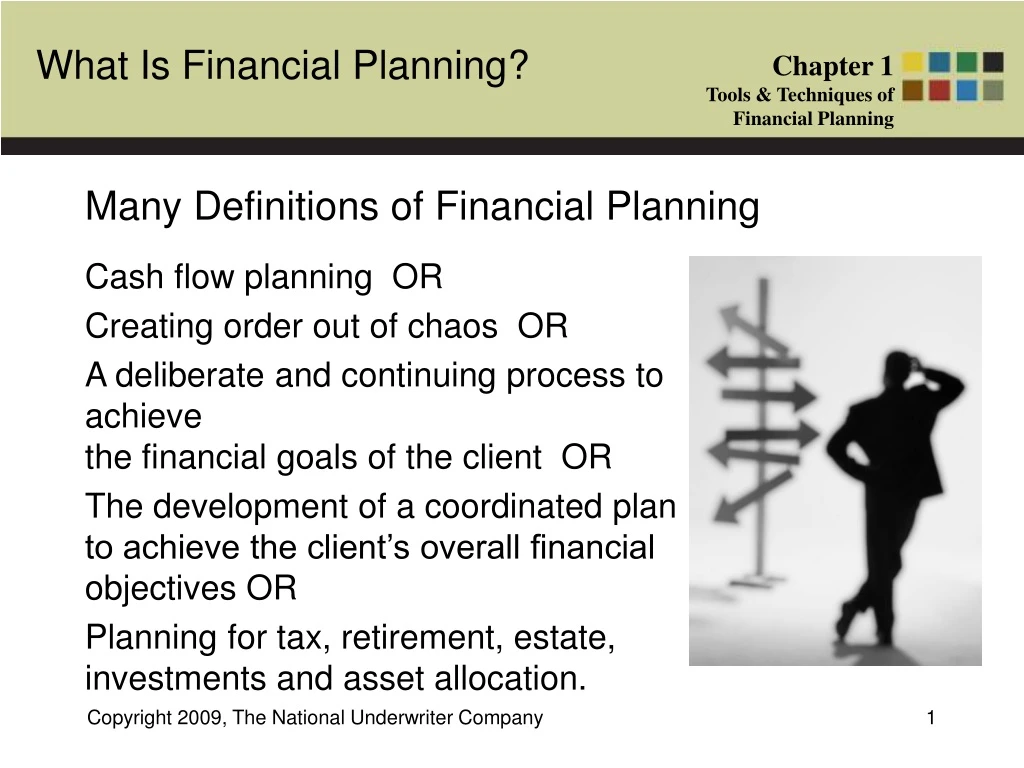

Many Definitions of Financial Planning Cash flow planning OR Creating order out of chaos OR A deliberate and continuing process to achievethe financial goals of the client OR The development of a coordinated plan to achieve the client’s overall financial objectives OR Planning for tax, retirement, estate, investments and asset allocation.

No two people’s problems will ever be exactly the same Some people will need very complex and detailed plans For others, just putting together a system that helps them control their cash and get their bills paid on time will be a successful plan.

Lack of Liquidity Not enough cash to meet current needs Can cause a “fire sale” of illiquid assets Definition: An inability to quickly turn capital assets into spend-able cash without incurring unreasonable cost. Note: Clients often overestimate their need for liquidity.

Inadequate Resources Not enough capital or income to meet needs for death, disability, retirement, education, or medical expenses. A common problem is clients who live above their means leaving inadequate resources for these important needs.

Inflation The crippling impact of loss of purchasing power -- the ability of each dollar to buy goods or services. Special Today! Only $50! Note: For long term planning, this is one of the biggest problems, and is often unrecognized by clients.

Inflation is a Fact of Life Since 1945, the purchasing power of the dollar has declined in every year but two – 1949 and 1950. From 1900 -1970, inflation averaged 2.5% 1970s were time of severe inflation – rose to 6%, then peaked at 13.3% in 1979. Recent inflation has averaged 2.5 to 3%. *Source: U.S. Bureau of Labor Statistics.

Improper Disposition of Assets Transferring the wrong asset to the wrong person at the wrong time. Example: Will leaves vintage sports car to 1 year old or a large sum of cash to an 18 year old.

Value The need to stabilize and secure the value of assets such as a business. Example: A business is dependent on the owner’s contacts and personal friendships to stayin business – a risk of value. I personally selected this just for you, Elizabeth….

Excessive Taxes • Too much tax reduces investment return and makes it harder to achieve financial goals. • Arranging the client’s affairs to minimize tax can help them realize their desires.

Special Needs Clients have varying psychological needs for security and safety. They may want to provide security for people such as children or siblings with special needs.

Resources Available • Earned income • Investment Assets • Employer pension plans and Social Security benefits Resources are a three-legged stool that support client needs. You need all three sources.

Most Common Goals and Objectives Current lifestyle Retirement planning Education Parental issues Estate planning Special needs

You can’t have it all… Set priorities and use strategies to achieve the most important goals. Common Strategies: • Reduce current lifestyle • Invest more aggressively • Postpone the goal.

The Financial Planning Report The report to the client should include: • ANALYSIS -- Where are you now? • OBJECTIVES -- Where do you want to be? • STRATEGIES -- How to get where you want to be. • SUMMARY – Summary and assignment of responsibilities Remember – Less is more. Be concise. Use pictures, charts and graphs.

The Financial Report – AnalysisWhere You Are Now Balance sheet Cash flow analysis Normal situation – current Normal situation – projected Death of breadwinner Disability of breadwinner Retirement Asset liquidity analysis

The Financial Report – ObjectivesWhere You Want to Be Quantification of Goals: • Increasing investable income • Improving liquidity • Reducing Risk • Increasing income at death, disability or retirement • Increasing financial security for heirs and satisfying charitable objectives Remember: Goals must be quantified! “Comfortable retirement” is vague.

The Financial Report – StrategyHow to Get Where You Want to Be • Tax strategy • Investment strategy • Risk management strategy • Wealth transfer strategy

The Financial Planning Report – Summary & Responsibilities Summary Who must take action What must be done Timetable for Implementation Date of Next Review