Download

1 / 9

90 likes | 262 Views

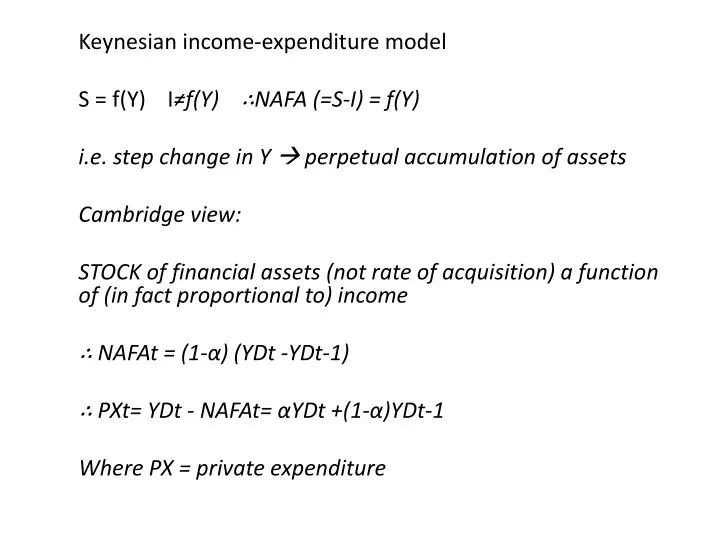

Keynesian income-expenditure model S = f(Y) I ≠f (Y) ∴NAFA (=S-I) = f(Y) i.e. step change in Y perpetual accumulation of assets Cambridge view: STOCK of financial assets (not rate of acquisition) a function of (in fact proportional to) income ∴ NAFAt = (1 - α) ( YDt -YDt-1 )

E N D

Keynesian income-expenditure model S = f(Y) I≠f(Y) ∴NAFA (=S-I) = f(Y) i.e. step change in Y perpetual accumulation of assets Cambridge view: STOCK of financial assets (not rate of acquisition) a function of (in fact proportional to) income ∴ NAFAt = (1-α) (YDt -YDt-1) ∴ PXt= YDt - NAFAt= αYDt +(1-α)YDt-1 Where PX = private expenditure

And period is length of time agents take to adjust stock of assets to incomes CEPG research found this to be one year Therefore estimated equation (with 3 other variables) and found (1975) PX = 0.533YD +0.416YD(t-1) + 0.899 HP +0.790BA +0.962S (increase in HP debt, increase in bank lending, stockbuilding) Since NAFAt = (1-α) (YDt -YDt-1)

And NAFA = (S-I) = (X-M) + (G-T) Therefore (M-X) = (G-T) – (1-α) (YD -YDt-1) Fiscal policy must be consistent with current account target If this is inconsistent with employment target, then the two could be reconciled by exchange rate depreciation but * Hard to engineer under a floating regime

* real effects liable to be undone by real wage resistance • * CEPG were ‘elasticity pessimists’ anyway Therefore might have to resort to * Credit controls * Rationing (Kaldor) * Import controls (tariffs and/or quotas)

SITUATION IN MARCH 1974 * oil prices up 300% in 6 months * current account deficit £4bn (4% of gdp) * price inflation 20%v (wage inflation higher) * unemployment still only 700,000 but rising sharply

TREASURY CHARGES AGAINST CEPG • No theory of investment • Ignored evidence that overseas sector was source of instability on the economy • Total NAFA had been fairly stable but its components (personal & corporate) hadn’t -- instead they cancelled out for reasons no one had explained Godley accepted third point but said it couldn’t rehabilitate discretionary fiscal policy

PARLIAMENTARY COMMITTEE’S CONCLUSIONS • don’t say inflation when you mean reflation • Treasury and CEPG should hold joint Seminars Treasury: CEPG (with stockbuilding & credit aggregates in equation) STRENGTHENED case for short-term forecasting + repeated criticism that stable surplus was sum of 2 unstable elements BUDGET AND CURRENT ACCOUNT DEFICITS PART COMPANY Fiscal deficit 7.2% of gdp in 1974, 9% in 1975 Current account deficit 4.5% of gdp in 1974, 1.7% in 1975

Kaldor: ‘New Cambridge has ceased to hold’ • CEPG 1976 review denied this: • Full-employment budget deficit hadn’t widened – if actual deficit had, this was due to the recession • M-X) = (G-T) – (1-α) (YD -YDt-1)

CHANGING TREASURY ATTITUDE TO DEMAND MANAGEMENT • Dec 1975; accepted vertical LR Phillips curve (by majority vote) • --move away from Cambridge so far as Godley, Kaldor still hostile to ‘natural rate’ doctrine • -- but moved Treasury towards Cambridge position so far as it gave them firmer basis for rejecting fine-tuning

![Election Expenditure Monitoring [EEM] Assembly Elections- 2013](https://cdn1.slideserve.com/3400245/slide1-dt.jpg)