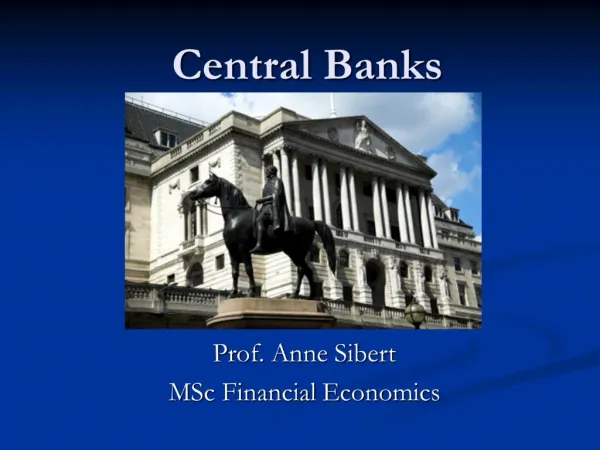

Download

1 / 21

210 likes | 431 Views

PRESENTATION TO THE 2ND AFRACA CENTRAL BANKS FORUM BY MRS. NORIANA MUNEKU, MANAGING DIRECTOR ZAMBIA NATIONAL BUILDING SOCIETY (ZNBS ). TOPIC Housing Market – Financing Home Ownership in Zambia. Synopsis. Background of Zambia National Building Society The Housing Market In Zambia

E N D

PRESENTATION TO THE 2ND AFRACA CENTRAL BANKS FORUM BY MRS. NORIANA MUNEKU, MANAGING DIRECTORZAMBIA NATIONAL BUILDING SOCIETY (ZNBS) TOPIC Housing Market – Financing Home Ownership in Zambia

Synopsis • Background of Zambia National Building Society • The Housing Market In Zambia • Financing Home Ownership • Market Developments • Challenges Faced In Home Ownership Financing

Background of the Zambia National Building Society • The Zambia National Building Society (ZNBS) was established in 1970 by an Act of Parliament, resulting from a merger of three private building societies . • Its primary purpose was the provision of housing finance. The ZNBS was for along time the largest Housing finance institution in Zambia since inception in 1970. Today there are two other Building Societies. These are Pan African Building Society and Finance Building Society.

The Housing Market in Zambia • There is a shortage of housing in Zambia due to lack of investment in the housing sector and the rapid population growth. • The Central Statistics Office put the number of available housing units at 2.1million for a population of 10.9 million in 2004 • Most of this housing stock is informal and poorly serviced or not serviced at all.

The Housing Market in Zambia….. • According to the National Housing Policy of January 1996, the backlog in housing stood at approximately 846,000 units. • To clear the backlog within a period of 10 years required that about 110,000 dwelling units be built per annum. • This has not been possible due to various reasons the major one being inadequate sustainable funding for homeownership.

Financing Home ownership in Zambia • The National Housing Policy identified clearly that the lack of a systematic allocation of financial resources to housing lay at the core of the problem identified. • Seen in this perspective, it is determined that public sector efforts should be focused at creating a system of financial institutions that will support the housing sector financially in a sustainable and orderly manner.

Financing Home ownership in Zambia • Historically employers were responsible for providing accommodation to their employees. Most employers built houses for their staff and maintained the same for them. This disadvantaged the building society industry as there was almost no need for people in employment to own homes. • However house loans were being given to individuals who saw the need especially those who were preparing for retirement.

Financing Home ownership in Zambia • Following the liberalization in the nineties most employers sold off company houses in order to free resources. Employees were being encouraged to own houses as most employers had come up with deliberate policies of not providing accommodation. • The need therefore arose for housing finance as more and more people saw the benefits of home empowerment.

Financing Home ownership in Zambia However efforts made towards provision of Housing finance have not been so effective because of: • High interest rates especially in the early nineties when rates shot to about 130% and only recovered after 2000 • Poor liquidity levels arising from low capital inflows after the interest rate shocks experienced in the market • Focus on the predominantly low income groups who were the most exposed to the effects of economic structural adjustments programmes and liberalisation

Financing Home Ownership in Zambia • Due to periods of high inflation experienced in the nineties and the consequent high interest rates in the economy, more and more people began finding it difficult to borrow and service their mortgage loans as affordability was increasingly eroded by interest

Market Developments • The above notwithstanding, there have been deliberate efforts of acquiring fresh capital into the industry by the players in the market. • In the recent past, other financial institutions including commercial Banks have also entered the housing finance market creating some levels of competition. • The industry mortgage portfolio has grown from K18billion as at March 2005 to K123 billion as at June 2008. This tenfold growth in a few years is a clear indicator of better things to come.

Market Developments • Other non finance institutions have entered the market and are engaged in construction of houses for sale to the public on loan and purchase basis. • These include Mean wood Property Development Company, Lilayi Housing Development Project and Vorne Valley Housing Limited • A National Housing Bond Trust to mobilize resources has been created and already started operations

Challenges faced in financing Home ownership • There is a poor credit culture among our people resulting in bad loans. The newly introduced Credit Reference Bureau will certainly help in mitigating bad loans

Challenges faced in financing Home ownership • Lack of affordable long term finance for onward lending which would benefit more people. • Interest rates continue to remain high because of the commercial sources of funds.

Challenges faced in financing Home ownership • Zambia had only 500,000 people in formal employment as at 2006 against a population of over 10.9 million, according to Central Statistics Office records. • Most of those in the informal sector don’t keep financial records making it difficult for a financier to assess their ability to meet installments in case a loan is granted to them. • As a result the target group by lenders is usually limited to people with verifiable stable income.

Challenges faced in financing Home ownership • About 94% of land in Zambia is customary land under the authority of Chiefs and no Title Deeds are available for such pieces of land making it impossible for one to access finance to build his home. • Lending institution would normally require that a long term home loan be secured by way of a mortgage on the property in question. • Access to land is difficult as the procedures involved are highly centralised and cumbersome. This discourages would be borrowers from going through the process of acquiring land before they can build.

Challenges faced in financing Home ownership • The growing competition is also a challenge as the same market is being targeted to the exclusion of the informal but well financed sector. • In an effort to win more clients there is the temptation to compromise professional credit assessment norms resulting in delinquent cases. The introduction of a Credit Reference Bureau will certainly help in mitigating bad loans.

Recommendations There is need for an apex organisation to provide long .term financing to primary mortgage lenders There is need for innovative approaches to housing finance products to cater for a large variety of clientele accessing housing finance . There is also need for alliances and partnerships among financing organisations for enhanced coverage of the market.

Recommendations There is need to simplify land acquisition procedures including the full decentralization of Government units responsible for land alienation to the grassroots such as local authorities The role of the planning authorities and structures at the local level need to be enhanced to make development predictable and easier