Download

1 / 34

340 likes | 627 Views

Balanced Scorecard. Objective. Provide a more complete and balanced view of corporate performance Give senior managers a concise but comprehensive view of the business Balanced Scorecard (BSC) approach described by Kaplan and Norton. Premise. “Measurement motivates”. Measurable Items.

E N D

Objective • Provide a more complete and balanced view of corporate performance • Give senior managers a concise but comprehensive view of the business • Balanced Scorecard (BSC) approach described by Kaplan and Norton

Premise • “Measurement motivates”

Measurable Items • Broadened set of measurable items to complement financial measures • Multiple measures provide balanced perspective • Included customer, internal process, and learning and growth measures

Perspective • Traditional financial metrics are backward-looking • Now look at “leading indicators” that are predictors of future success

Performance Perspectives • Customer perspective • Internal perspective • Innovation and learning perspective • Financial perspective

Use of BSC • BSC is deployed in more than half the Fortune 500 companies* Intelligent Enterprise, July 2002

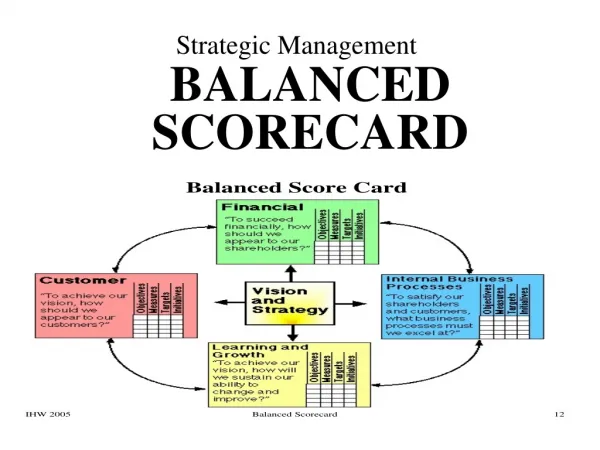

Learning & Growth Financial Internal Business Process To achieve our vision, how will we sustain our ability to change and improve? To succeed financially, how should we appear to our shareholders? To satisfy our shareholders and customers, what business processes must we excel at? Objectives Objectives Objectives Measures Measures Measures Targets Targets Targets Initiatives Initiatives Initiatives Customer To achieve our vision, how should we appear to our customers? Objectives Measures Targets Initiatives What is the BSC? VISION AND STRATEGY

Customer Perspective • Who are our customers? • What is our value proposition? • Operational excellence (Wal-Mart) • Product leadership (Nike) • Customer intimacy (Nordstrom)

Internal Process Perspective • What are our key processes? • Should be based on our value proposition • Operational excellence (Wal-Mart) • Product leadership (Nike) • Customer intimacy (Nordstrom)

Learning and Growth Perspective • Do we have key skills and information systems? • Where are the gaps?

Financial Perspective • Profitability...

Developing Objectives - Customers • Who are our customers, and what is our value proposition in serving them? • Customer intimacy – increase customer retention

Developing Objectives – Internal Processes • To satisfy our customers and shareholders, at what processes should we excel? • Customer objective processes

Developing Objectives - Financial • What financial steps are necessary to ensure the execution of our strategy? • Cost-leadership – lower unit costs

Developing Objectives – Internal Employee Learning • What capabilities and tools do our employees require to help them execute our strategy? • Skill gap • Information systems

Total assets Total assets per employee Profits as a % of total assets Return on total assets Revenues/total assets Gross Margin Net Income Profit as a % of sales Profit per employee Revenue Revenue from new products ROE ROI Commonly Used Financial Measures

Customer Satisfaction Customer Loyalty Market Share Customer Complaints Return rates Response time Direct Price Price relative to competition Total cost to customer Customers lost Customer retention Customer acquisition costs Number of customers Commonly Used Customer Measures

Average cost per transaction On-time delivery Average lead time Patents pending Stockouts Labor utilization rates Response time to requests Defect percentage Breakeven time Cycle time Warranty claims Waste reduction Commonly Used Internal Process Measures

Employee participation Training investment Average years of service Turnover rate Employee suggestions Motivation index Diversity rates Quality of work environment Training hours Reportable accidents Ethics violations Commonly Used Learning and Growth Measures

Subsidiary ScorecardExample • Consolidated ROA • Subsidiary on-time goals by month • Subsidiary baggage handling goals by month • Subsidiary operational dependability goalby month

Link Measurements to Strategy • Define mission and strategy • Determine how performance will differ if I succeed with vision • Determine Critical Success Factors • Determine critical measurements

Implementation • 3-4 measures per perspective • Frequency of measurement • Establishing targets • Performance measurement • Incentive systems

Building a Balanced Scorecard • Preparation • Interviews (first round) • Executive workshop (first round) • Interviews (second round) • Executive workshop (second round) • Implementation • Periodic reviews

First Generation BSC • BSC software developed and designed as reporting or management dashboard tools • First applications to integrate financial and non-financial reporting • “Red, yellow, green” reporting of achievement of targets

Goal of First Generation BSC Reporting • Quickly understand health of organization • Focus attention on areas requiring attention

Evolution of BSC • Use BSC to help implement and manage strategy

Strategy-Focused Organization • Executive leadership to lead change • Translate strategy into operational terms • Align organization to strategy • Make strategy everyone’s job • Make strategy a continual process

Sources • BSCol Functional Standards • www.bscol.com/standards • Balanced Scorecard Institute • www.balancedscorecard.org