Download

1 / 13

130 likes | 332 Views

Risk Adjustment in Medicare Part D Prescription Drug Benefit. Open Door Forum December 2004. Risk Adjuster Basics. Capitated payment is adjusted according to the expected cost of the enrollee. Expected cost is derived from enrollee characteristics:

E N D

Risk Adjustment in Medicare Part DPrescription Drug Benefit Open Door Forum December 2004

Risk Adjuster Basics • Capitated payment is adjusted according to the expected cost of the enrollee. • Expected cost is derived from enrollee characteristics: • Enrollees may be sorted, by their characteristics, into cells that have assigned risk factors, or • Characteristics may be assigned risk factors that are added to produce a total risk factor • In Part D the basic payment formula is: Payment = standardized bid enrollee’s risk factor – plan’s enrollee premium

Risk Adjuster Structure • The CMS risk adjuster produces a person-specific risk factor by summing the factors associated with characteristics such as: • Age/sex, e.g., male 70-74, female 70-74 …. • Originally disabled status, e.g., male 65+ who entered Medicare < 65 because of disability • Presence of medical conditions, e.g., cancers, diabetes, liver disorders, ischemic heart diseases, heart failure, psychiatric disorders …

Risk Adjuster Structure • The risk model is prospective: the medical conditions from a given year are used to predict expenditures in the next year. • The disease groupings are clusters of related ICD-9-CM diagnosis codes. • Diagnoses from hospital inpatient, hospital outpatient, and clinician sources are used. • The disease groups are derived from the CMS-HCC risk model used in the Medicare Advantage program today, but have been modified to reflect drug spending as opposed to spending on A/B services.

Risk Adjuster Structure • The risk factors for disease groups are additive when the diseases are not closely related: • inflammatory bowel disease, AMI, schizophrenia • The groups may be in hierarchies when related and their costs have a logical ranking: • Diabetes with complications, diabetes without complications • Only the highest coded group in a hierarchy counts for payment.

Risk Adjuster Structure Additive model: factors for demographic characteristics + factors for diagnoses

Risk Adjuster Development • Principal data source: Drug claims for Federal retirees in FEHB Blue Cross Blue Shield Service Benefit Plan + Medicaid sample • Diagnoses from linked Medicare files • Diagnoses from 2001 to predict costs in 2002 and similarly from 2000 to predict 2001 • Decedents in cost years were included till death. • A linear regression model was estimated • Dependent variable – total spending on prescription drugs, annualized, mix of retail and mail order • Explanatory variables – the array of person characteristics - age/sex, diseases • Estimated coefficients are the incremental costs of each condition or demographic characteristic.

Risk Adjuster Development • In an iterative process, the disease groups were disassembled into smaller subgroups, and reassembled to allow empirical estimation of costs and clinical judgment to weigh in the development. • The explanatory power of the model is on a par with other drug models reported (R2=.23 for spending) and is higher than similar models for Parts A and B.

Risk Adjuster – rough example 1 for 2006 Spending Model Coded Spending Relative CharacteristicIncrement Factor Female, age 76 $ 850 .283 Diabetes, w. complications 1,600 .533 Diabetes, uncomplicated 1,000.333 High cholesterol 450 .150 Congestive Heart Failure 650 .217 Osteoporosis 500 .167 Total Annual Pred. Spending $4,050 1.350 For implementation, dollar amounts are divided by the national mean (~ $3,000) to create relative factors that multiply base rates.

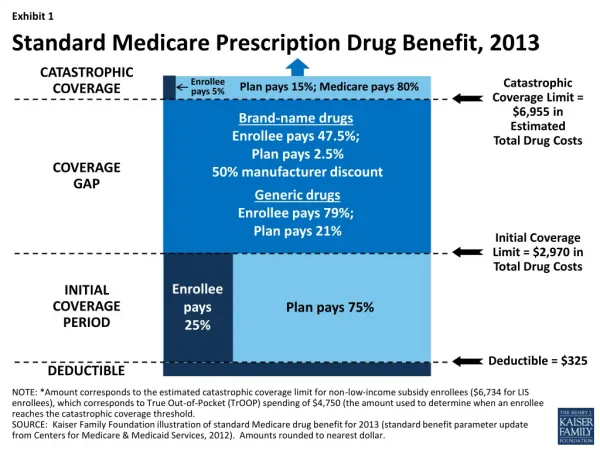

Risk Adjuster for Plan Liability • Plans are not liable for the total spending. Standard benefit liability is 75% of spending from $250 to $2250, about 15% above $5100, and 0% elsewhere. • The structure developed for modeling spending has been re-estimated on the same data set, with the standard benefit structure applied to each enrollee’s spending. • This is the Plan Liability model. (R2=.25) • The average projected 2006 spending in the data is about $3,000; the average plan liability from the data is about $1,100.

Risk Adjuster – rough example 2 for 2006 Liability Model Coded Payment Relative CharacteristicIncrement Factor Female, age 76 $ 550 .500 Diabetes, w. complications 300 .273 Diabetes, uncomplicated 200.182 High cholesterol 150 .136 Congestive Heart Failure 250 .227 Osteoporosis 150 .136 Total Annual Pred. Spending $1,400 1.272 For implementation, dollar amounts are divided by the national mean (~ $1,100) to create relative factors that multiply base rates.

Risk Adjuster for Plan Liability • Tasks to be completed • Development of New Enrolleemodel for people new to Medicare with insufficient data for risk adjustment. This model is based on demographics. • Study of Medicaid population to investigate: • factors for under-65 disabled population • adjustments for institutional population • adjustments for low-income population

Schedule • Late December • Release of Bidders Data Set - 5% files of FFS beneficiaries with imputed drug utilization • Late January • Posting of draft model coefficients and mappings of diagnoses to disease groups • Release of drug risk factors for people in 5% files • Mid February • 45-day notice for MA with PDP information • Late March • Bid and Risk Adjustment training • April • Release of final model, software and final risk factors for 5% file if different from draft