Download

1 / 14

140 likes | 311 Views

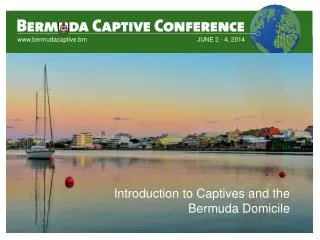

Introduction to Captives and the Bermuda Domicile. Moderator: Federico Candiolo , Counsel, ASW Law Ltd Panelist(s): Roger Aliaga -Diaz, PhD, Senior Economist, Vanguard Investment Strategy Group Gerardo Filorio , Business Administration, Director, Lockton , Mexico

E N D

Introduction to Captives and the Bermuda Domicile Moderator: • Federico Candiolo, Counsel, ASW Law Ltd Panelist(s): • Roger Aliaga-Diaz, PhD, Senior Economist, Vanguard Investment Strategy Group • Gerardo Filorio, Business Administration, Director, Lockton, Mexico • Dr. Marcelo Ramella, Deputy Director, Policy and Research, Policy, Legal Services & Enforcement Department, Bermuda Monetary Authority • Tino van den Heuvel, Partner, Tax Attorney, Hill Smith King & Wood New York

CIRCULAR 230 NOTICE: Under the applicable Treasury regulations we are required to inform you that any information in this communication is not intended or written by HILL SMITH KING & WOOD to be used, and cannot be used, by a client or any other person or entity (i) for the purpose of avoiding penalties that may be imposed on any taxpayer or (ii) promoting, marketing or recommending to another party any matters addressed herein. The information contained herein is of a general nature and based on authorities that are subject to change. Applicability of the information to specific situations should be determined through consultation with your tax adviser. The views expressed herein are those of the authors and do not necessarily reflect the views of Hill Smith King & Wood.

Overview Today’s Topics: • Tax treatment of the insured • Taxation of the captive insurance company • Tax treatment of the owner of the captive insurance company

Overview Base Case Legend A corporation. Unless otherwise stated all entities are wholly-owned An individual (natural) person or a group of individuals Owner (Peru) 3. Operating/Holding Cy (Peru) Captive Insurance Cy (Bermuda) 2. Insurance Premiums 1. Operating Subsidiary (Colombia) Insurance Premiums

Tax treatment of the Insured Many LATAM countries have a consider- able corporate tax rate and thus imposing a high cost on (i) earned, (ii) retained and (iii) distributed income. Therefore, if properly structured a captive insurance company may significantly reduce the effective tax rate of the insured company by deduction insurance premiums paid to the captive insurance company

Deductibility Premiums • Deductibility and timing of the insurance premiums: • Most LATAM countries allow for a deduction of insurance premium payments to related captive insurance companies; • Some countries however defer the deduction of the insurance premiums to a captive insurance company if it is based in a tax haven to the moment they are actually paid; • A number of countries restrict deductions if the captive insurance company does not have sufficient (functional) substance. A captive with only a few insured participants or inadequately financed may not be respected.

Withholding Taxes on Premiums • Withholding taxes on insurance premium payments: • Almost all LATAM countries impose withholding taxes at the source on the payment of insurance premiums. Usually the rate of withholding depends on the location of the captive insurance company. If the captive is based in a tax haven country then the withholding tax rate is usually higher. • In these cases the interposition of a holding company in country which has a tax treaty with the country of the insured company may offer a solution. Under most treaties the insurance premiums are treated as business profits and thus allocate the right to tax to the recipient country. • Bermuda has entered into a significant number of Taxation Information Exchange Agreements with countries which results in the removal of ‘blacklists’ and a reduction of withholding taxes.

Taxation of the Captive • Main tax considerations: • Income tax rate • How is taxable income determined? • Dividend withholding tax on distribution of profits? • Tax treaty network?

Taxation of the Owner • Controlled Foreign Corporation (“CFC”) legislation: • Under CFC legislation the owner of the captive insurance company would have to include in income on a current basis, whether distributed or not, the profits of the insurance company if certain conditions are met; • Generally, one or more of the following criteria should be met for a company to be considered a CFC: • A certain ownership percentage by one person of the company’s shares; • The company’s income is derived from passive investments (e.g., dividends, interest, etc.) or related party transactions • The company is based in a tax haven; • CFC legislation effectively eliminates the tax benefits of a captive insurance company if applicable.

Taxation of the Owner • Tax treatment of dividends received from the captive insurance company: • Many countries apply a partial exemption or lower rate to dividends received by individuals from corporations; • Careful planning may allow for the efficient repatriation of the profits of the captive insurance company. • Estate Planning: • Captive insurance company by their nature as investment vehicles are a great estate planning tool through which wealth can be distributed over multiple generations without or minimal taxes.

Example Planning Structures Venezuela For Illustration Purposes Only Owner (Venezuela) Beneficiaries (Venezuela) Settlor Trust (Offshore) EU Holding Cy (EU) Re-insurance Premiums Insurance Premiums Operating Cy (Colombia) Operating Cy (Venezuela) Captive Insurance Cy (Bermuda)