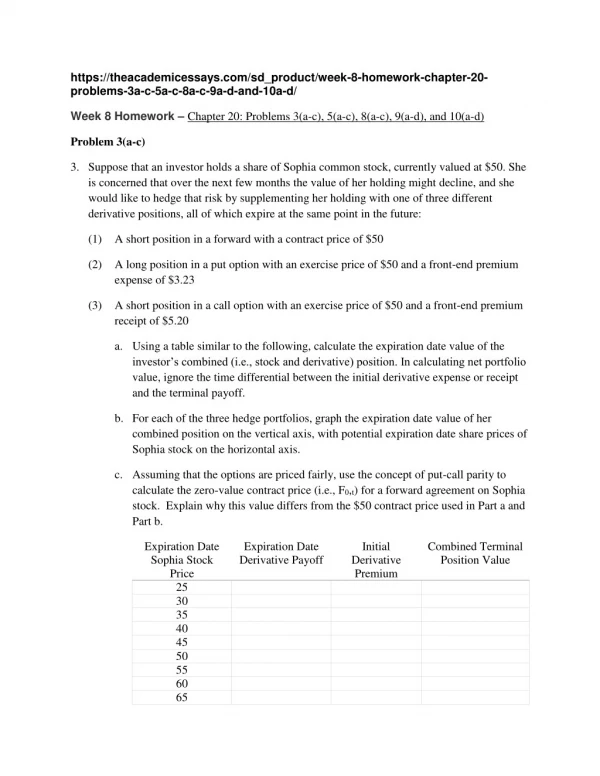

Week 8 Homework – Chapter 20: Problems 3(a-c), 5(a-c), 8(a-c), 9(a-d), and 10(a-d)

https://theacademicessays.com/sd_product/week-8-homework-chapter-20-problems-3a-c-5a-c-8a-c-9a-d-and-10a-d/ Week 8 Homework – Chapter 20: Problems 3(a-c), 5(a-c), 8(a-c), 9(a-d), and 10(a-d) Problem 3(a-c) 3. Suppose that an investor holds a share of Sophia common stock, currently valued at $50. She is concerned that over the next few months the value of her holding might decline, and she would like to hedge that risk by supplementing her holding with one of three different derivative positions, all of which expire at the same point in the future: (1) A short position in a forward with a contract price of $50 (2) A long position in a put option with an exercise price of $50 and a front-end premium expense of $3.23 (3) A short position in a call option with an exercise price of $50 and a front-end premium receipt of $5.20 a. Using a table similar to the following, calculate the expiration date value of the investor’s combined (i.e., stock and derivative) position. In calculating net portfolio value, ignore the time differential between the initial derivative expense or receipt and the terminal payoff. b. For each of the three hedge portfolios, graph the expiration date value of her combined position on the vertical axis, with potential expiration date share prices of Sophia stock on the horizontal axis. c. Assuming that the options are priced fairly, use the concept of put-call parity to calculate the zero-value contract price (i.e., F0,t) for a forward agreement on Sophia stock. Explain why this value differs from the $50 contract price used in Part a and Part b. Expiration Date Sophia Stock Price Expiration Date Derivative Payoff Initial Derivative Premium Combined Terminal Position Value 25 30 35 40 45 50 55 60 65 70 75 Chapter 20: Problem 5(a-c) 5. The common stock of Company XYZ is currently trading at a price of $42. Both a put and a call option are available for XYZ stock, each having an exercise price of $40 and an expiration date in exactly six months. The current market prices for the put and call are $1.45 and $3.90, respectively. The risk-free holding period return for the next six months is 4 percent, which corresponds to an 8 percent annual rate. a. For each possible stock price in the following sequence, calculate the expiration date payoffs (net of the initial purchase price) for the following positions: (1) buy one XYZ call option, and (2) short one XYZ call option: 20, 25, 30, 35, 40, 45, 50, 55, 60 Draw a graph of these payoff relationships, using net profit on the vertical axis and potential expiration date stock price on the horizontal axis. Be sure to specify the prices at which these respective positions will break even (i.e., produce a net profit of zero). b Using the same potential stock prices as in Part a, calculate the expiration date payoffs and profits (net of the initial purchase price) for the following positions: (1) buy one XYZ put option, and (2) short one XYZ put option. Draw a graph of these relationships, labeling the prices at which these investments will break even. c. Determine whether the $2.45 difference in the market prices between the call and put options are consistent with the put-call parity relationship for European-style contracts. Chapter 20: Problem 8(a-c) 8. As an option trader, you are constantly looking for opportunities to make an arbitrage transaction (i.e., a trade in which you do not need to commit your own capital or take any risk but can still make a profit). Suppose you observe the following prices for options on DRKC Co. stock: $3.18 for a call with an exercise price of $60, and $3.38 for a put with an exercise price of $60. Both options expire in exactly six months, and the price of a six-month T-bill is $97.00 (for face value of $100). a. Using the put-call-spot parity condition, demonstrate graphically how you could synthetically recreate the payoff structure of a share of DRKC stock in six months using a combination of puts, calls, and T-bills transacted today. b. Given the current market prices for the two options and the T-bill, calculate the no-arbitrage price of a share of DRKC stock. c. If the actual market price of DRKC stock is $60, demonstrate the arbitrage transaction you could create to take advantage of the discrepancy. Be specific as to the positions you would need to take in each security and the dollar amount of your profit. Chapter 20: Problem 9(a-d) 9. You are currently managing a stock portfolio worth $55 million and you are concerned that over the next four months equity values will be flat and may even fall. Consequently, you are considering two different strategies for hedging against possible stock declines: (1) buying a protective put, and (2) selling a covered call (i.e., selling a call option based on the same underlying stock position you hold). An over-the-counter derivatives dealer has expressed interest in your business and has quoted the following bid and offer prices (in millions) for at-the-money call and put options that expire in four months and match the characteristics of your portfolio: Bid Ask Call $2.553 $2.573 Put 1.297 1.317 a. For each of the following expiration date values for the unhedged equity position, calculate the terminal values (net of initial expense) for a protective put strategy. 35, 40, 45, 50, 55, 60, 65, 70, 75 b. Draw a graph of the protective put net profit structure in Part a, and demonstrate how this position could have been constructed by using call options and T-bills, assuming a risk-free rate of 7 percent. c. For each of these same expiration date stock values, calculate the terminal net profit values for a covered call strategy. d. Draw a graph of the covered call net profit structure in Part c, and demonstrate how this position could have been constructed by using put options and T-bills, again assuming a risk-free rate of 7 percent. Chapter 20: Problem 10(a-d) 10. The common stock of Company XLT and its derivative securities currently trade in the market at the following prices and contract terms: Price ($) Excise Price ($) Stock XLT 21.50 – Call Option on Stock XLT 5.50 21.00 Put Option on Stock XLT 4.50 21.00 Both of these options will expire in 91 days from now; and the annualized yield for the 91-day Treasury bill is 3.0 percent. a. Briefly explain how to construct a synthetic Treasury bill position. b. Calculate the annualized yield for the synthetic Treasury bill in Part a using the market price data provided.

73 views • 4 slides