Download

1 / 5

50 likes | 270 Views

Basis adjustment required for a substantial loss. Substantial built-in loss means more than $250,000On transfer of partnership interest, a Section 743 adjustment is requiredException for

E N D

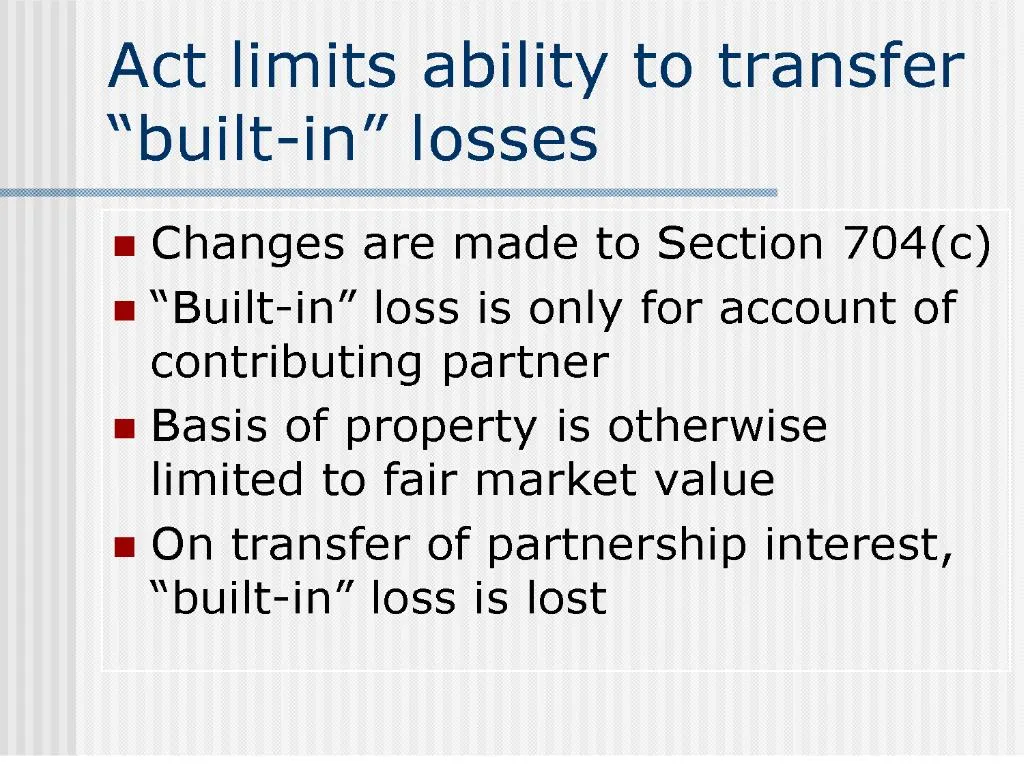

1. Act limits ability to transfer �built-in� losses Changes are made to Section 704(c)

�Built-in� loss is only for account of contributing partner

Basis of property is otherwise limited to fair market value

On transfer of partnership interest, �built-in� loss is lost

3. New definition � �Electing Investment Partnership� Investment company � no trade or business

All assets held for investment

95% of contributions in money

24 month raise

15 year term

Also see � Securitization Partnership

4. Basis of stock of a partner which is a corporation Rev. Rul. 99-57 dealt with gain aspect of stock of corporate partner

On liquidating distribution, Section 755 will not permit loss to be allocated to corporate stock

Allocate to other property

When out of property, partnership recognizes gain

5. Effective Dates Generally effective for contributions after date of enactment

For E.I.P. in effect on 6/4/04, no restriction on redemptions and 20 year term instead of 15 years

Corporate stock rule effective for distributions after date of enactment