Download

1 / 23

230 likes | 441 Views

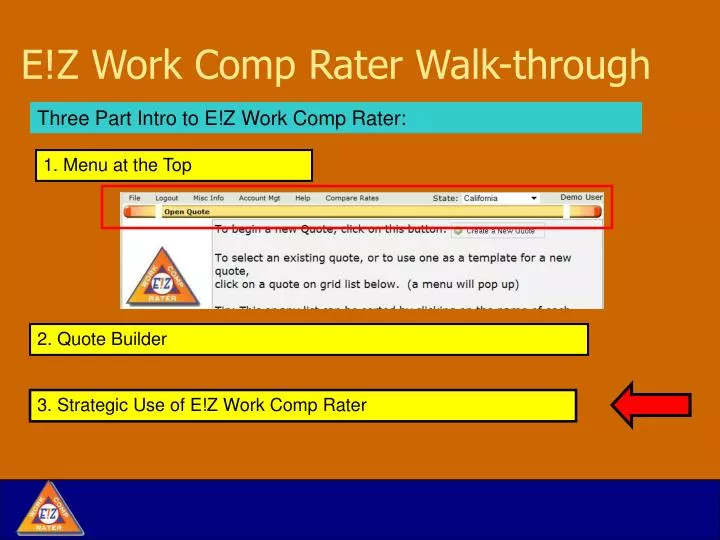

E!Z Work Comp Rater Walk-through. Three Part Intro to E!Z Work Comp Rater:. 1. Menu at the Top. 2. Quote Builder. 3. Strategic Use of E!Z Work Comp Rater. Part III: Using E!Z Work Comp Rater Strategically *. * Competing armed with Market Information.

E N D

E!Z Work Comp Rater Walk-through Three Part Intro to E!Z Work Comp Rater: 1. Menu at the Top 2. Quote Builder 3. Strategic Use of E!Z Work Comp Rater

Part III: Using E!Z Work Comp RaterStrategically * * Competing armed with Market Information

Using E!Z Work Comp Rater Strategically – Three Examples Identifying who is likely to compete for an account you already have. You keep running up against another carrier that comes in with a lower premium. How do they do it? You keep running up against a particular carrier for the same accounts. What do you have that they don’t? What do they have that you don’t?

Using E!Z Work Comp Rater Strategically Example 1: ID your likely competition. *This is your account and you want to protect it: A Gear manufacturer, governing class code 3635 Payroll = $600,000 Experience Mod = 1 Insured with Accident Fund Ins. Co. of America (Base tier rates) * This example is set in MI.

Step 1: Do Manual Rate Comparison • What You Learn • Carriers with closest • manual rates: • Travelers Indemnity • of CT • Hartford Insurance of • the Midwest • Middlesex (Sentry)

Step 2: Sort Carrier List by Group and scroll to Hartford Group. • What You Learn: • Hartford carrier with closest manual rate is Tier 2 with manual rates deviated downward 20%. • Moving Cursor would show Twin City Fire is base tier carrier. Tier 2: (-20%)

Repeat Step 2 with Travelers. • What You Learn • Travelers carrier with closest manual rate is Tier 3 with manual rates deviated downward 20%. • Moving Cursor would show Travelers Indemnity of America is base carrier. Tier 3: (-20%)

Repeat Step 2 with Sentry. • What You Learn • Sentry carrier with closest manual rate is Tier 3 with manual rates deviated downward 5%. • Moving Cursor would show Sentry Insurance A Mutual Company is base carrier. Tier 3: (-5%)

Based on what you learned • Logical to select carriers with the closest manual rates for governing class code And • Reasonable to assume base tier carriers that Hartford, Sentry, and Travelers tier assignment rules are like the Accident Fund, so those could be competing carriers.

Step 3: Select carrier competitors.

Step 4: Check on manual rates for the carriers you’ve selected. • What You Learn: • Biggest surprise – • Sentry Ins. A Mutual Co, • the base rate carrier, • has lower manual rate • than lower tier carrier • (Middlesex). • Sentry appears to • have interest in this • type of account.

Step 5: Look at All Carriers Report by Premium. • What You Learn: • Both Sentry Carriers • have lower premium. • Neither Hartford • nor Travelers base • tier carriers are • competitive. • 5% Schedule Credit • Would bring Accident • Fund to lowest cost.

Using E!Z Work Comp Rater Strategically Example 2: Your competition comes in lower... How Do They Do It? You write for ACE and this account is placed with ACE Indemnity: Auto Dealership, governing class code 8391 Payroll = $3,591,502 Experience Mod = 1 Risk wants $1 mil/$1 mil/$1 mil Increased Limits Competing against Zurich American * This example is set in CA.

Step 1:You have entered payroll and now check manual rates using the Rates By Carrier Report. What You Learn: Ace Indemnity & Zurich American have identical manual rates for the codes in this policy.

Step 2:You run the All Carriers by Premium report to look at final premium. What You Learn: Manual Premium is the same for both carriers, as you would expect. BUT, there is a $12,741 (9.3%) difference in final Annual Premium. How did this happen and what can you do?

Step 3:Use the Detailed Reports to see how this happened. What You Learn: Increased Limits: Difference of $3962 Premium Discount: 3.85% v. 8.5% Terrorism Risk Ins. Act: 9% v. 3%

Step 3:What Can You Do to Compete? Any Credit Programs? Possible for better tier placement? What Else You Might Do: You go to the Carriers by Group report and see that comparison is between 2 “base rate” carriers in their groups. Depending on the Underwriting Criteria, the account might be moved to a lower tiered carrier in the group. What You Learn: The Go To Menu tells you Schedule Rating is only Credit Program for either Carrier. You will need a minimum Of a 9.3% schedule credit To compete with the Zurich price.

Using E!Z Work Comp Rater Strategically Example 3: Know what your competition has to offer. As you know, fully researching the account you want is basic to getting an account. You need to know about workplace policies & practices. E!Z Work Comp Rater helps you translate what you know into premium $$. * This example is set in CA.

Step 1:What credits & surcharges are in the market? A quick way to get a market-wide overview is to create a “dummy” quote. Select all the carriers in the database (highlight top one, hold down Shift key, and use down arrow). Then select a class code all carriers have, such as 8810 (or 953 in PA). Enter Payroll. The dropdown box in Go To to see all adjustments offered by all carriers. * This example is set in CA.

Step 2:Who Do You Regularly Compete Against? EXAMPLE: • You write for Delos. • You regularly compete for the same accounts against: • Employers Compensation Insurance Co. • Everest National • Praetorian Ins. Co. * This example is set in CA.

Step 3: Set up a quote where you face your competition* and look at the Go To dropdown box. . What You Learn: This list shows you the Credits offered by the collection of carriers you have Selected. * Quote: $600,000 payroll in code 8018.

Step 4: Now deselect all your competition but one, go to the Go To drop down box to see what each competitor offers. Example here: Employers Compensation Ins. . If there are credits, use Go To to see what discounts go with those credits. Example of What You Learn: Employers Comp can apply a 10% Discount if the risk has signed up with an approved health care provider. Repeat with each carrier you compete against.

Step 5: Armed with information about what credits your competitors offer, things you would do... • You will be certain to research the account sufficiently that you can make an educated guess whether the account will be eligible for the credit. • If you compete against particular carriers repeatedly, you may want to get copies of the rate filing so you know the underwriting rules and can know with more certainty whether the risk can get the credit.* • You now have an even tighter estimate of how large a schedule credit you would need to get this account. * M & R may be able to provide the filing, depending on the carrier and how much you need.