Download

1 / 33

330 likes | 701 Views

TAX RESEARCH (1 of 2). Overview of tax research Steps in the tax research process Importance of facts to the tax consequences Sources of tax law Tax services . TAX RESEARCH (2 of 2). Citators Computers as a research tool Statements on standards for tax services.

E N D

TAX RESEARCH(1 of 2) • Overview of tax research • Steps in the tax research process • Importance of facts to the tax consequences • Sources of tax law • Tax services ©2008 Prentice Hall, Inc.

TAX RESEARCH(2 of 2) • Citators • Computers as a research tool • Statements on standards for tax services ©2008 Prentice Hall, Inc.

Overview of Tax Research(1 of 2) • Close-fact or tax compliance • Facts already occurred • Discovery of tax consequences • Proper disclosure ©2008 Prentice Hall, Inc.

Overview of Tax Research(2 of 2) • Open-fact or tax-planning • Before structuring or concluding a transaction • Minimization of taxes • Careful compliance permits legal avoidance of taxation ©2008 Prentice Hall, Inc.

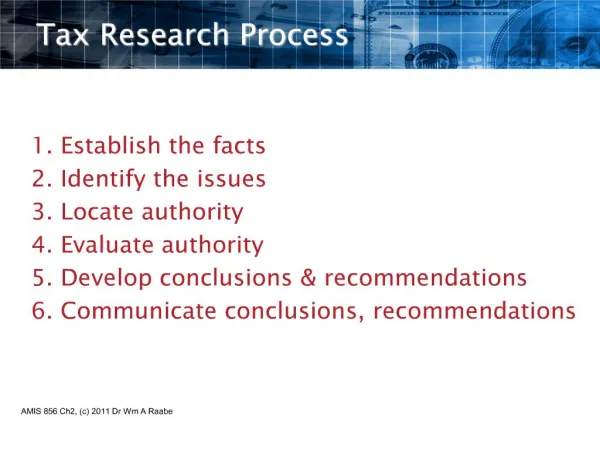

Steps in the Tax Research Process(1 of 2) • Determine the facts • Identify the issues (questions) • Locate applicable authorities • Evaluate authorities • Choose which to follow when authorities conflict ©2008 Prentice Hall, Inc.

Steps in the Tax Research Process(2 of 2) • Analyze facts in terms of applicable authorities • Communicate conclusions and recommendations to client ©2008 Prentice Hall, Inc.

Importance of the Facts to the Tax Consequences • Ambiguous situations (gray areas) • Facts are clear but the law is not • Law is clear but the facts are not • Advance planning permits facts to develop that produce favorable tax consequences ©2008 Prentice Hall, Inc.

Sources of Tax Law(1 of 2) • Legislative process • Internal Revenue Code • Treasury Regulations • Administrative pronouncements • Judicial decisions • Tax treaties • Tax periodicals ©2008 Prentice Hall, Inc.

Legislative Process • House Ways and Means Committee • Voted on by full House • Senate Finance Committee • Voted on by full Senate • Conference Committee • Voted by both full House and Senate • Signed or vetoed by President • Override veto by 2/3 vote by both houses ©2008 Prentice Hall, Inc.

Internal Revenue Code (IRC) • Title 26 of the United States Code enacted by Congress • Organization • Title • Subtitle • Chapter • Subchapter - Part - Subpart - Section ©2008 Prentice Hall, Inc.

Treasury Regulations(1 of 3) • Treasury Dept. delegates authority to IRS to promulgate Treas. Regs. • Types of Treasury Regulations • Proposed: no authoritative weight • Temporary • Provide immediate guidance • Same authority as Final Regs. • Final ©2008 Prentice Hall, Inc.

Treasury Regulations(2 of 3) • Interpretative regulations • Interpret related Code section • Less authority than IRC • Legislative regulations • Almost the same authority as IRC • Legislative reenactment doctrine ©2008 Prentice Hall, Inc.

Treasury Regulations(3 of 3) • 1.165-5 • 1 – Income tax • 165 – IRC citation • 5 – 5th regulation • Subject matter • 1 – Income tax • 20 – Estate tax • 25 – Gift tax • 301 – Admin/procedural matters • 601 – Procedural rules ©2008 Prentice Hall, Inc.

Administrative Pronouncements(1 of 3) • Revenue Rulings • More specific than Regs. • Less authority than Regs. • Revenue Procedures • IRS guidance on procedural matters ©2008 Prentice Hall, Inc.

Administrative Pronouncements(2 of 3) • Citation of Revenue Rulings and Procedures • Rev. Rul. (or Proc.) 97-4, 1997-1 C.B. 5 • 4th Rev. Ruling of 1997 • In Cumulative Bulletin 1997-1 on p. 5 ©2008 Prentice Hall, Inc.

Administrative Pronouncements(3 of 3) • Letter Rulings • Reply to specific taxpayer question • Only authority for specific taxpayer • Other interpretations • Technical Advice Memoranda • Information releases • Announcements and notices ©2008 Prentice Hall, Inc.

Judicial Decisions • Overview of court system • U.S. Tax Court • U.S. District Courts • U.S. Court of Federal Claims • U.S. Supreme court • Precedential value of various decisions ©2008 Prentice Hall, Inc.

Overview of Courts ©2008 Prentice Hall, Inc.

Tax Court(1 of 3) • Taxpayer does not pay deficiency before litigating case • No jury trial available • Regular and Memorandum decisions • Small Cases Procedure • Acquiescence policy ©2008 Prentice Hall, Inc.

Tax Court(2 of 3) • Regular decisions • First time court hears case • Memo decisions • Factual variations of previous cases • Small cases procedure • Cases of <$50,000 eligible • Less formal than regular tax court ©2008 Prentice Hall, Inc.

Tax Court(3 of 3) • Acquiescence policy • IRS announces whether or not it agrees with Tax Court decisions ©2008 Prentice Hall, Inc.

U.S. District Courts • May request a jury trial • Must pay deficiency first • Unreported decisions • Decisions not officially reported • Published by RIA and CCH ©2008 Prentice Hall, Inc.

U.S. Court of Federal Claims • No jury trial • Must pay deficiency first • Decisions appealable to Circuit Court of Appeals for the Federal Circuit ©2008 Prentice Hall, Inc.

Courts of Appeals • Losing party at trial level may appeal decision to appellate court • Circuit Courts of Appeals • Appeals from Tax Court & district courts • Based upon geography • Court of Appeals for the Federal Circuit • Appeals from U.S. Court of Federal Claims ©2008 Prentice Hall, Inc.

Supreme Court • Very few tax cases are heard • Hears cases when • Circuit courts are divided or • Issue of great importance • Same authority as IRC ©2008 Prentice Hall, Inc.

Precedential Value of Decisions ©2008 Prentice Hall, Inc.

Tax Services(1 of 2) • Annotated services • Organized by IRC section • United States Tax Reporter by RIA • Standard Federal Tax Reporter by CCH ©2008 Prentice Hall, Inc.

Tax Services(2 of 2) • Topical services organized by topic • Federal Tax Coordinator 2d by RIA • Law of Federal Income Taxation (Mertens) by West Group • Tax Management Portfolios by BNA • CCH Federal Tax Service by CCH ©2008 Prentice Hall, Inc.

Citators • History of the case • List of other authorities that have cited the case in question • Figure C1-5 summarizes how to use a citator as part of the research process • CCH Citator • RIA Citator 2nd Series ©2008 Prentice Hall, Inc.

Computers as a Research Tool • Computerized sources • No findings list • Cross referencing facilitated by hyperlinks • No cumulative supplements • New developments integrated into main text • Primary sources accessible from explanatory paragraphs via hyperlinks • Citator symbols explicitly spelled out ©2008 Prentice Hall, Inc.

Statements on Standards for Tax Services (SSTSs) • Issued by AICPA • Not legally enforceable • May be cited in a negligence lawsuit as “standard of care” for tax practitioners • Professionally enforceable by AICPA • Violations could result in suspension or loss of license • See Appendix E ©2008 Prentice Hall, Inc.