Download

1 / 28

280 likes | 399 Views

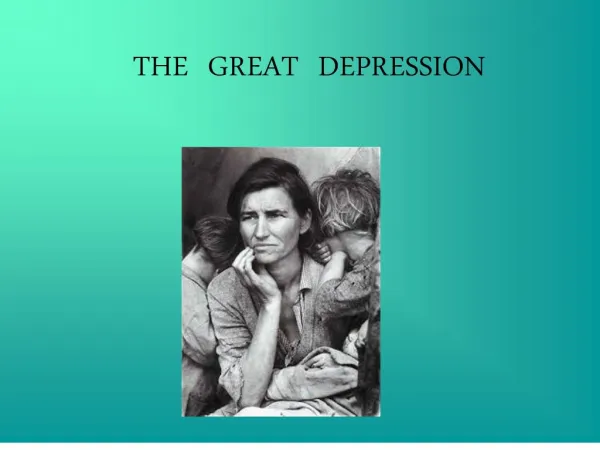

The Great Depression Ahead. presented by Harry S. Dent, Jr. The Spending Wave Births Lagged for Peak in Family Spending. Dow Adjusted for Inflation. Immigration-adjusted Births Lagged for Peak Spending. Australia Spending Wave 1950-2090. Source: United Nations. Australian Immigration.

E N D

The Great Depression Ahead presented by Harry S. Dent, Jr.

The Spending WaveBirths Lagged for Peak in Family Spending Dow Adjusted for Inflation Immigration-adjusted Births Lagged for Peak Spending

Australia Spending Wave1950-2090 Source: United Nations

Australian Immigration Source: Financial Demographics (www.findem.com.au)

Australia All Ordinaries Index vs. US Dow Industrials Source: Bloomberg

China Spending Wave Source: United Nations

India Spending Wave Source: United Nations

Long Term House Prices vs. Inflation Source: Robert J. Shiller, Irrational Exuberance, 2nd Edition, Princeton University Press, 2005.

Home Price AppreciationBritain, Australia, and US1998-2009 Source: OFHEO, ABS, Nationwide

Australian House Price Index Series by Financial Demographics Pty Ltd

Overpriced Housing Markets Source: 2008 Demographia International Housing Affordability Survey

50 Least Affordable Housing Markets Source: 2008 Demographia International Housing Affordability Survey

50 Least Affordable Housing Markets Source: 2008 Demographia International Housing Affordability Survey

Overpricing in Australia and New Zealand Source: 2008 Demographia International Housing Affordability Survey

Affordable Markets by Country Source: 2008 Demographia International Housing Affordability Survey

Mortgage & Household BudgetsPayment as a % of Household Income Source: 2008 Demographia International Housing Affordability Survey

29-30 Year Commodity Price CycleCRB Index (PPI before 1947) 2039-40 2009-10 1980 1920 1951

Exports as a Percentage of GDPSelected Countries Source: CIA World Factbook

Australian Trailing P/E Source: Peter Quinton 2008 Share Market Update

Australia All Ordinaries Index 5 1 B 3 A 1 4 2 C 2 Source: Bloomberg

Refocus: Identify the Parts/Lines/Stores of Your Business that Are Most Profitable and that You Want to Keep; Sell or Divest the Rest to Increase Cash/Cash Flow Sell Unnecessary Real Estate in 2009 to Create Cash and Lease/Rent until 2012 Cut Unnecessary Costs Now before Being Forced to Later Outsource Non-Strategic Functions for Greater Focus and Flexibility Defer Capital Expenditures Until Downturn Bottoms and Costs Fall, Focus Now on Investments that Increase Cash Flow Near Term Pay Off High Interest Loans by Late 2009/Early 2010 and Refinance at Lower Rates Later . . . if You Will Be Credit Worthy Structure Fixed Rate Loans/Mortgages that Switch to Variable Rates from Late 2010 Forward Structure Leases/Loans to Mature between Mid-2011 and mid-2013 for Best Leverage to Renegotiate or Refinance Protect Your Personal Assets from Lawsuits – Trusts, Variable Annuities “Cash/Cash Flow Is King” . . . Steps for Surviving the Shake-out

Sell Stocks/Business Investments on Likely Bounce into April or July Sell Commodities into Likely Bounce into late 2009/early 2010 Sell Investment, Noncore Real Estate by Fall of 2009 Pay Down High Interest Debt Refinance Mortgages Now and/or Mid-2011 – Late 2012 . . . Fixed Rates Until Late 2010/early 2011/early 2012 Lock in Long Term Government Bonds around Mid-2010 Lock in Long Term Corporate Bonds around Late 2010 Lock in Municipal Bonds around Late 2010/Mid 2011 Reinvest in Asian Stocks around Late 2010 Reinvest in Health Care/Australian Growth Stocks around Mid-2012 Reinvest in Select Real Estate around Late 2012/early 2013 Sell Stocks Again around Early to Mid-2017 Reinvest Long Term between Early 2020 and late 2022 Avoid East Asia after 2019 (China, South Korea, Japan) Cash Is King . . . Investor Strategies for Surviving Deflation

For more information, visit www.hsdent.com • Free Sample of HS Dent EconomicMonthlyForecast • Free Downloads