Download

1 / 24

240 likes | 478 Views

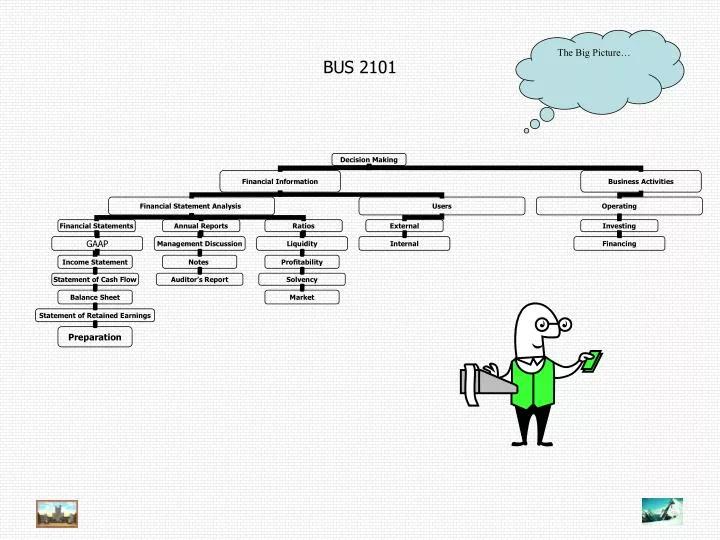

BUS 2101. The Big Picture…. Reporting and Analyzing Inventory. Classifying Inventory Periodic Inventory System Ownership of inventory Inventory costing. Classifying Inventory. Merchandisers (BUS 2101) Merchandise Inventory Buy and sell Manufacturers (BUS 2102) Raw Materials

E N D

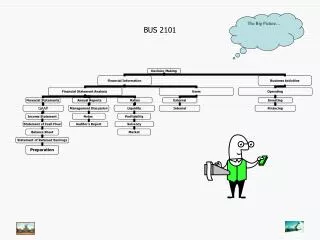

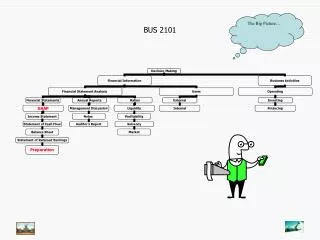

BUS 2101 The Big Picture…

Reporting and Analyzing Inventory • Classifying Inventory • Periodic Inventory System • Ownership of inventory • Inventory costing

Classifying Inventory • Merchandisers (BUS 2101) • Merchandise Inventory • Buy and sell • Manufacturers (BUS 2102) • Raw Materials • Work in Process • Finished Goods

Purchase of merchandise Use Merchandise Inventory account for only inventory, not supplies, equipment, etc.

Freight on merchandise purchased Freight for merchandise purchased is part of the cost of an asset, inventory.

Freight on merchandise sold Freight for merchandise sold is an expense.

Returns of merchandise sold Negative revenue

Sales discounts Sales Discounts is a negative revenue account.

Cost of Goods Sold What would happen to COGS if ending inventory was actually $22,000 instead of $20,000? What would happen to net income???

Ownership of Inventory • Goods in transit • FOB destination • Seller owns goods during delivery and pays for delivery • FOB shipping point • Seller owns goods during delivery and pays for delivery • Consignment • Retailer tries to sell goods for fee but doesn’t take ownership of goods • Antique stores

Inventory Costing • Specific identification • FIFO • LIFO • Average cost

Specific Identification • Used for high cost items • Combines, cars, jewelry • Retailer knows the exact cost of each item it sells

FIFO • First in, first out • Ending inventory is most recent purchases • In times of rising prices • Higher inventory value • Lower COGS and higher net income (EPS) • But also higher income taxes • If prices fall, lower net income and inventory

LIFO • Last in, first out • Ending inventory is most oldest purchases • In times of rising prices • Lower inventory value • Higher COGS and lower net income (EPS) • Lower income taxes

LIFO • If prices fall, • Higher net income and more income taxes • Oldest inventory never sold • Caterpillar • LIFO inventory $2,842; FIFO inventory $4,820 • Large difference due to use of LIFO for over 50 years

LIFO • If use LIFO on tax return, must use LIFO in financial statements • But can disclose LIFO reserve in footnotes to financial statements which tells how much inventory would be using FIFO • LIFO inventory $2,842 • LIFO reserve $1,978 • FIFO inventory $4,820 • Annual increase in LIFO reserve is the amount Net Income decreased that year due to use of LIFO • If reduce quantity of inventory • Possible large net income as selling inventory with very “old” costs

Average Cost • Weighted average, not average cost • Average = Total cost / total units

Inventory errors • Understating ending inventory • Increases COGS • Understates net income • Understating beginning inventory • Decreases COGS • Overstates net income • Over two years, would offset if second year ending inventory correct

BUS 2101 The Big Picture…