Download

1 / 26

260 likes | 569 Views

Accounting for Transactions. Accounts receivable Beginning Cash receipts (TOT) balance (py) Sales returns Sales on and allowances account (TOT) Bad debt Ending charge-off

E N D

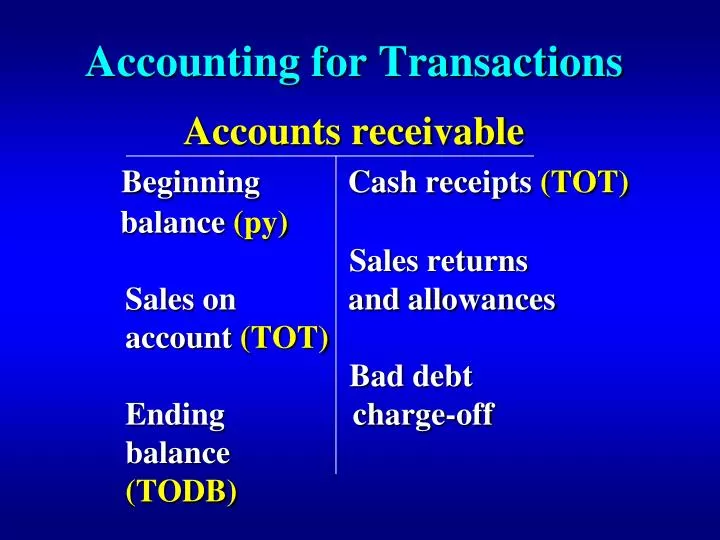

Accounting for Transactions • Accounts receivable • Beginning Cash receipts (TOT) • balance (py) • Sales returns • Sales on and allowances • account (TOT) • Bad debt • Ending charge-off • balance • (TODB)

Accounting for Transactions • Accounts receivable • Beginning Cash receipts • balance • Sales returns • Sales on and allowances • account • Bad debt • Ending charge-off • balance • SR & A and bad debts are non-cash credits (TOT and TODB)

Sales and Cash Receipts • Sales Cycle • Customer Order • Sales Order • Shipping document (bill of lading) • Sales invoice • Sales journal • AR subledger • Credit memo

Cash Receipts Cycle • Cash receipt prelist • Remittance advice • Cash receipts journal • Accounts receivable subledger • Bad debt charge-off

Approach to Designing Tests • 1. Identify controls for each objective • 2. Design TOC for key controls • 3. Design STOT for objective • 4. Assess whether tests are adequate for each objective • Ex. - Occurrence • TOC - Sales invoices supported by bill of lading • STOT - Trace sales entry to invoice, shipper, order

Authorizations • Credit • Shipment • Pricing • Authorization can be general or specific, depending on circumstances

Authorizations • TOT Related • Authorization Obj. TODB obj. • Credit Occurrence NRV • Shipment Occur./Acc Same • Pricing Accuracy Same

Monthly Statements • Monthly statements can lead to timely detection of errors resulting in overstatement of customer accounts, including: • Sales posted to incorrect account • Cash receipt posted to incorrect account • Misappropriation of customer deposits

Direction of Tests • From a journal to source document(concerned with recorded amounts) = Occurrence • From a source document to journal(concerned with unrecorded amounts) = Completeness

Direction of Tests for Sales • Customer • Order • Shipping Completeness • DocumentStart • Duplicate • Sales Invoice • OccurrenceSales • Start Journal • General LedgerA/R Master File Posting & Summ.

14-27(a) • To minimize failures to post invoices to the AR subledger, the auditor would select a sample from: • 1. Customer order file • 2. Bill of lading file • 3. Customer AR master file • 4. Sales invoice file

Direction of Tests for Sales • Customer • Order • Shipping Completeness • DocumentStart • Duplicate • Sales Invoice • OccurrenceSales • StartJournal • General LedgerA/R Master File Posting & Summ.

14-23(a) • An auditor is performing STOT for sales. Tracing debit entries in the AR master file back to sales invoices establishes? • 1. Sales invoices represent existing sales. • 2. All sales have been recorded. • 3. Sales invoices have been properly posted to customer accounts. • 4. Debit entries in the AR master file are supported by sales invoices.

Direction of Tests for Sales • Customer • Order • Shipping Completeness • DocumentStart • Duplicate • Sales Invoice • OccurrenceSales • StartJournal • General LedgerA/R Master File Posting & Summ.

STOT for Sales • Occurrence Traces sales to shipper • Completeness Trace shippers to sales • AccuracyReperform (p x q) • Classification Not usually a concern • Timeliness Compare ship date to invoice & journal date • Post & Summ. Foot journal; test • postings

14-23(b) • To verify that all sales transactions have been recorded, STOT should be performed on a sample drawn from? • 1. Entries in the sales journal • 2. Billing clerk’s file of sales orders • 3. Duplicate sales invoices for which the sequence has been accounted. • 4. Shipping clerk’s file of bills of lading

14-22(c) • Sales invoice for $5200 was correctly computed but key entered as $2500 in journal and AR master file. Customer remitted $2500, the amount on the monthly statement. Error would be detected by: • Prelistings and control totals are used to control postings. • Invoice extensions are independently checked. • Customer statements are verified and mailed by someone other than the bookkeeper. • Unauthorized deductions are investigated.

Sales Returns • Theory - Allowance recorded at time of sale (matching). • Practice: • - Returns recorded as they occur. • - Allowance adjusted at year-end for expected returns. • Why might there be excessive returns after year-end?

Why might there be excessive returns after year-end? • Shipment of unwanted goods to increase sales(ex. Bausch & Lomb)

Sales Returns • Returnssupported by receiving report • Allowances and write-offsauthorized • Objectives • Transactions-Focus is on occurrence of returns • Balances- Focus is on completeness of returns

14-22 (a) • A company received a large sales return in the last month of year, but the credit memo wasn’t prepared until after the auditors completed field work. The returned goods were included in inventory. Error would be detected by: • Aged AR trial balance prepared • Credit memos prepared and accounted for. • Reconciliation of AR trial balance and general ledger is performed. • Receiving reports are prepared and accounted for.

Cash Receipts • Prelisting - mail should be opened and prelisted by non-accounting personnel • restrictively endorsed • compared with actual deposit • Critical to preventing theft of cash (completeness assertion)

Cash Receipts • Lockbox - checks can be sent directly to bank box, greatly reducing risk of theft • Regular monthly statements • A/R Subledger independently reconciled • Review for large non-cash credits

Monthly Statements • Monthly statement will reveal if customer account is too high • Sale or cash receipt credited to wrong account • Cash receipt not credited to account

Bank Reconciliation • Bank reconciliation will reveal whenever cash activity does not equal activity in journals • Cash receipt credited to customer, but not deposited in bank

A/R • Sale CR • Return • Bad debt • *Non-cash credits can hide theft of cash receipts