Download

1 / 15

210 likes | 535 Views

Business Transactions and The Basic Accounting Equation. Introduction to Business Chapter 2. Learning Objectives. Describe the relationship between property and property rights. Explain the meaning of “equity” as it is used in accounting.

E N D

Business Transactions and The Basic Accounting Equation Introduction to Business Chapter 2

Learning Objectives • Describe the relationship between property and property rights. • Explain the meaning of “equity” as it is used in accounting. • List the parts of the basic accounting equation and define each part. • Show how various business transactions affect the basic accounting equation.

Learning Objectives • Check the balance of the basic accounting equation after a business transaction has been analyzed and recorded. • Define the accounting terms introduced in this chapter.

Property and Property Rights • The right to own property is basic to our private enterprise system. • Property – anything of value that is owned or controlled. • When you own property, you have a legal right to that item. • When you have control over an item, you have the right only to the use of the item. • Property Rights – the cost or financial claims of property, measured by dollar amounts.

Property and Property Rights • Credit – when you buy property and agree to pay for it later. • Creditor – the business or person selling you the property on credit, who you owe money to. • When you buy property on credit, you do not have the only financial claim to property. You share that claim with the creditor.

Check Your Learning – page 19 Use the following formula to solve problems 1-4. Creditor’s Financial Claim + Owner’s Financial Claim Property

Financial Claims in Accounting • Separate Entity - businesses are considered separate entities from the personal property of their owners. • The owner’s personal financial transactions are not a part of the business’s records.

Financial Claims in Accounting • In Accounting: • Assets – the property or items of value owned by a business. Some examples are cash, office equipment, buildings, and land. • Equity – the total financial claims to the assets or property of a business. • Owner’s Equity – the owner’s claims to the assets of a business. • Liabilities – creditor’s claims to the assets of the a business, or money owed to creditors.

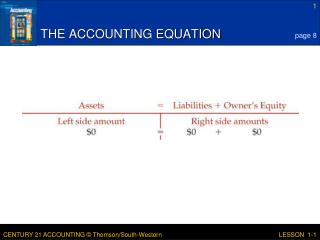

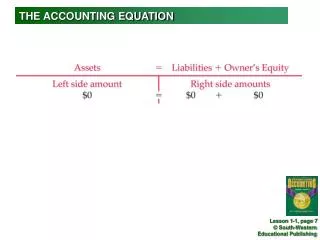

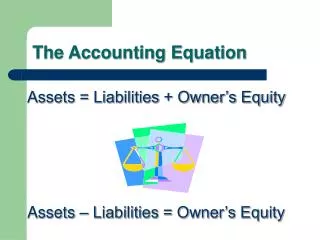

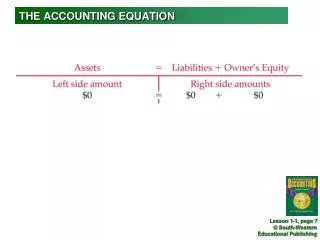

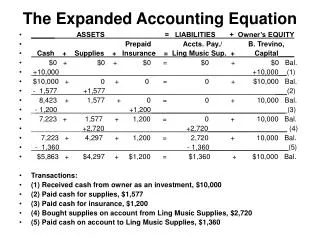

Basic Accounting Equation • The relationship between assets and total equities – liabilities plus owner’s equity – is known as the basic accounting equation. Assets = Liabilities + Owner’s Equity • Read example on page 20 *Check Your Learning page 21

Business Transactions • Business Transaction – an economic event that causes a change in assets, liabilities, or owner’s equity. • They involve buying, selling, or exchanging goods and services. • The financial position of the business changes when transaction occur. • Account – a record of the increases or decreases in and the balance for a specific item such as cash or equipment.

Business Transactions • Accounts represent things in the real world such as money invested, office furniture, money owed. • Each business sets up its accounts according to its needs. • Accounts Receivable – the total amount of money to be received in the future for goods and services sold on credit. • Accounts Payable – the amount of money owed, or payable, to a businesses creditors. • Capital – refers to the dollar amount of the owner’s investment in the business.

Effects of Business Transactions on the Basic Accounting Equation • When a business transaction occurs: • Identify the accounts affected. • Classify the accounts affected (asset, liability, or owner’s equity) • Determine the amount of increase or decrease for each account affected. • Make sure the basic accounting equation remains in balance.

Transactions that occur most often: • Investments by the owner • Cash transactions • Credit transactions • Revenue and expense transactions • Withdrawals by the owner *Remember, each transaction affects at least two accounts. • * Check Your Learning - page 27

Revenue and Expense Transactions • Revenue – income earned from the sale of goods and services. Revenue increases owner’s equity because it increases the business’s assets. • Expense – any price paid for goods and services used to operate a business. Expenses decrease owner’s equity because they decrease the business’s assets.

Withdrawals By The Owner • If a business earns revenue, the owner will take cash or other assets from the business for personal use. • This transaction is called a withdrawal. • A withdrawal decreases both assets and owner’s equity. Check Your Learning – page 30