Download

1 / 58

570 likes | 580 Views

Compound Interest & Rule of 72 Biggest Wealth Killer High Cost of Waiting Unnecessary Transfers Opportunity Costs Be The Bank Eleven Ways to “Find” the Money The REAL Retirement Miracle

E N D

Financial Concepts 1. Compound Interest & Rule of 72 2. Biggest Wealth Killer 3. High Cost of Waiting 4. Unnecessary Transfers 5. Opportunity Costs 6. Be The Bank 7. Eleven Ways to “Find” the Money 8. The REAL Retirement Miracle

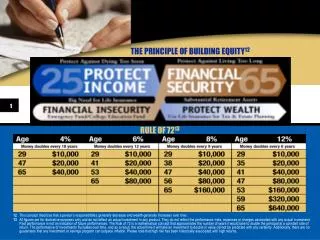

Compound Interest “The most powerful force in the universe is compound interest.” 1- Albert Einstein "The person that understands compound interest will earn it. The person that does not will pay it!“ 2– Albert Einstein 1richnow.wordpress.com Secrets of the rich revealed, Don’t ignore The power of Compound Interest, Dec.6, 2006 2Ibeatmybank.com/see_how_it_s_done.html

72/ 6% =12 yrs 72/12% = 6 yrs 72/3%=24 yrs What’s the MOST exciting double?

Save $1 million by age 67 You'd better get started soon. The longer you wait, the more you'll have to put away each month to reach your retirement goals

Don’t Pay the High Cost of Waiting • 27 years old? $214 a month. • Age 37, …$541 mo. • Age 47,…. $1,491 mo. • Age 57, hefty $5,168 mo. • Wait until the last minute (age 62) and you'd have to stash $13,258 mo. to reach $1 million by age 67. Don’t give up hope- we have an answer

Number 1 Wealth KILLER Taxation • Double a dollar 20 times • It grows to….. ……….$1,048,576 • If you tax 30% on each double • It grows to….. …..$40,642 The Million Dollar Mistake!!!

Anybody see a trend here? You Earn it They Tax it You Spend It They Tax it You Save It They Tax it You Die They Tax it

Unnecessary transfers • By recapturing unnecessary transfers the dollars you were losing and to put these dollars towards your accumulated money and/or lifestyle money with no additional out of pocket cost.

Opportunity Cost • The interest you could have earned, had you been able to avoid losing it or transferring it away. • A dollar paid in taxes unnecessarily not only costs you that dollar but it also costs you what the dollar could have earned had you not given it away.

You Finance Everything! You either finance by: a. Paying interest to someone else – a bank, lender, finance Co, credit card etc. b. Or giving up interest you could have earned otherwise. When you pay cash the interest the money could have earned is forfeited This is Opportunity Cost

Typical Family •Two cars, both cars are financed or leased they often swim in credit card debt, and perhaps home equity debt. •They have a mortgage. •Typical family spends about 34% of its income on paying interest to creditors.

Typical Family •At the same time they are contributing less than 5% of their income to their savings plan and they have put much, if not all, of that at risk. •In other words, they are spending a lot more on interest than they are saving.

Financing Cars We all know that you lose money on buying cars • Did you realize how much? • Did you know there is a much better way? • Over a lifetime the interest paid on financing cars plus the opportunity cost lost on financing accounts for a significant wealth transfer. • (Lease or pay cash still have opportunity cost)

Financing Cars So what’s the answer? The answer lies not in what you buy but how you buy it.

Financing Cars An example: • 40 year old couple purchases (one) new vehicle every 4 years at a cost of $30,000. • They expect to keep driving until age 80. So, over 40 years they will buy 10 new cars. Assumptions: We are not factoring any money down or inflation but we know prices will go up. We will assume they can earn 8% on their investments and an 8% opportunity cost. We will use an 8% loan finance rate

Financing Cars • If they continue to finance one $30,000 car every 4 years over the next 40 years they could transfer almost $300,000 in opportunity cost. The more cars you add to the equation, the greater the loss. • Over 40 years, the total cost is: Principal Interest Opportunity Cost $300,000 $ 51,546 $297,121 $648,667 TOTAL COST Imagine of you could have every dime back plus interest

Become The Bank Our Solution • Start building an account that will allow you to withdraw the money necessary to • Pay cash for your next car and then pay yourself back, paying yourself the principal & interest . • You can “self-finance” everything. • That $648,667 or more could be in your account instead

Sad But True… • People saving in qualified plans at work ( 401k, IRA etc.) Do not have Liquidity, Use & Control of their money and are forced to finance their car Many Americans who finance their cars lose more money in interest financing their automobiles so they can get to work, than they will accumulate in their lifelong savings accounts at work.

First Bank of YOU • Great College Plan • College expenses taken out Tax Free • Not included in college aid grant formulas • Cash Value is owned by parents • Plan completion • Business Owners • Equipment • No need to “qualify” for a loan • Anything Financed

Twelve reasons why You should build your personal ‘bank’ 1. You can get to the money in your ‘bank’ whenever you want it or need it . . . no penalties, no waiting, no taxes and no application. 2. The government, your employer, or any other outsiders have nothing to say about how you operate your ‘bank.’ 3. Your ‘bank’ is protected from creditors and lawsuits (protections are not the same for every state so check with your state .) 4. You can borrow from your ‘bank’ for any reason and you don’t have to qualify in any way.

Twelve reasons why You should build your personal ‘bank’ 5. When you borrow from your ‘bank’, the money in your ‘bank’ keeps growing as if you hadn’t borrowed a cent. . . your money does double duty. 6. Your ‘bank’ allows you to recover the money you pay to purchase cars, household furnishings, vacations, and other big ticket items or to fund education, business start-ups or any other costly expense, and deposit both interest and principal you recover back into your ‘bank.’ 7. Your ‘bank’ allows you to put all of the interest you would normally pay to credit card companies, banks and other credit grantors into your ‘bank’ where it compounds for your benefit.

Twelve reasons why You should build your personal ‘bank’ 11. Your ‘bank’ lets you grow your wealth tax-free every year . . . no sliding backward . . . no worries about stock market crashes or real estate bubbles . . . just peace of mind about your money. 12. Your ‘bank’ serves you without compromise while you are alive and allows you to pay forward –tax-free to anyone you choose – your legacy of wealth and wisdom.

Twelve reasons why You should build your personal ‘bank’ 8. Your ‘bank’ allows you to prepay the cost of future health and long term care so the money you need as you age is in your ‘bank’ when you need it most. 9. Your bank funds an inflation-protected income that you do not have to work for and you can’t outlive. 10. You can use the money in your ‘bank’ when an unforeseen life event throws you off the track. Plus Living Benefits

Does This Work? • This method is used by many Banks. • To capitalize a portion of their banking system, Banks purchase billions in insurance. • This pool of capital is a MAJOR source of working capital the bank draws on to fuel it’s banking system.

Cash Value Life Insurance: A Cornerstone Asset Of a Bank November 24, 2008 By Barry Dyke • Cash value life insurance is one of the most important assets of a bank, particularly America’s large banks. • Banks purchase so much cash value life insurance that life insurance of this type has its own name • BOLI (bank-owned-life-insurance).

Cash Value Life Insurance: A Cornerstone Asset Of a Bank November 24, 2008 By Barry Dyke • Banks own so much BOLI that the banks could be considered life insurance companies unto themselves. According to the Federal Deposit Insurance Corporation (FDIC) and the General Accounting Office (GAO), BOLI is a cornerstone of a bank and one most important assets in the nation’s banking and financial systems.

Cash Value Life Insurance: A Cornerstone Asset Of a Bank November 24, 2008 By Barry Dyke In fact, according to the FDIC figures in June 30, 2008, Bank of America owned $18.99 billion dollars of Cash Value life insurance

From Wikipedia Tier 1 capital is the core measure of a bank's financial strength from a regulator's point of view. It is composed of core capital,[1]which consists primarily of common stock and disclosed reserves (or retained earnings), [2]but may also include non-redeemable non-cumulative preferred stock.

Your Money Bucket If you were filling a bucket What would you do if your bucket had holes?

“FIND” money to Fund YOUR Bank

Eleven ways to “find” money to fund your plan: 1. Restructure debt Cleverly reducing debt will allow you to use the dollars freed up for your policy. There are a half dozen ways to do this.

Eleven ways to “find” money to fund your plan: 2.Reduce funding of your 401(k) or other retirement plans This brings them the guarantees, tax advantages, life, living benefits and flexibility provides that their traditional, government-sponsored 401(k), IRA or pension plan does not.

Eleven ways to “find” money to fund your plan: 3. Rescue your IRA or 401(k) Use IRS rule, 72(t), to transfer your money out of a qualified plan, to fund your policy. Avoid the premature distribution penalty anyone younger than 59½.

Eleven ways to “find” money to fund your plan: 4. Tap your savings Consider opening a policy and moving some of your current savings into it. Your policy can be used as an emergency fund

Eleven ways to “find” money to fund your plan: 5. Rethink that tax refund Some people love getting a big tax refund check in the mail every year. But that’s your own money you’re getting back. You’re giving the government an interest-free loan, while getting a zero rate of return on your money. Fast and easy to adjust your withholding, immediately increase your monthly cash flow (in some cases by hundreds of dollars a month), and use those dollars to fund your policy

Eleven ways to “find” money to fund your plan: 6. Get home based business tax deductions Write off “business” expenses Auto % Cell, Internet Phone, Electric etc Home Office Travel Entertainment Meals More

Eleven ways to “find” money to fund your plan: 7. Quote your home owners and Auto Ins Consider raising the deductibles Self insure inside your policy

Eleven ways to “find” money to fund your plan: 8. Make lifestyle changes • Like holding onto your car a few years longer than you normally would and holding off on buying a new one. • It’s also easy to cut monthly costs through simple changes like eating out less, and bundling your Internet, cable TV, and phone services

Eleven ways to “find” money to fund your plan: 9. Convert existing life insurance policies • Cash value from existing policies may be an option. In some situations, taking a withdrawal from the old policy and using that to fund a policy may be an option. • Careful analysis here: Giving up an old insurance policy is not always in your best interest.

Eleven ways to “find” money to fund your plan: 10. Manage your home equity wisely • Many people like the feeling of security that comes with building up equity in their home, or owning it free and clear. • Some people make extra mortgage payments, or refinance to a 15-year mortgage, even if it makes them feel financially pinched.

Eleven ways to “find” money to fund your plan: 10. Manage your home equity wisely • There are hidden dangers • Payments of principal you make into your home do not make money for you • The equity in your home is not liquid • The equity in your home is not guaranteed (a fact which came as a shock to many when the real estate market crashed) • There is no tax benefit to having equity in your home

Eleven ways to “find” money to fund your plan: 11. Make More Money • Become a paid referral agent • Just 2-3 referrals a year could fund a $3,000 year plan • The Real Retirement Secret Wait until the last minute (age 62) and you'd have to stash $13,258 a month to reach $1 million by age 67. A Team of 10 sales and you do one or two a month